Equity Markets: Decluttering for Trades

Sometimes you stare at that ceiling crack for years or watch that damp plaster patch fester into a blackening mould. Days turn into months, then into years before you decide to take any action, as my good friend confessed to me recently what happened to her last weekend when seized by the decluttering bug, which is a little behind the Marie Claire reader curve (sniggers).

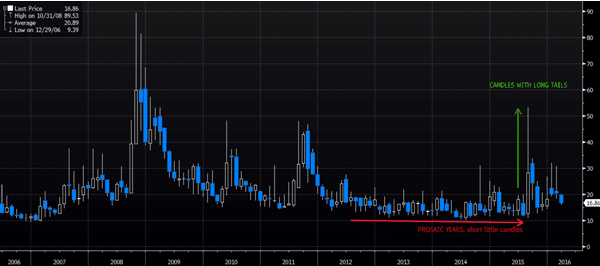

Decluttering is in vogue, after Marie Kondo’s NY Times Bestselling book The Life Changing Magic of Tidying Up has been singled out as a global consumer trend for millennials in 2016 and beyond. This coincides with my personal paradigm shift into 2016, watching some of the most exciting market volatility since 2011, evidenced in the hair-raising candlesticks of the VIX monthly volatility chart for the past six months.

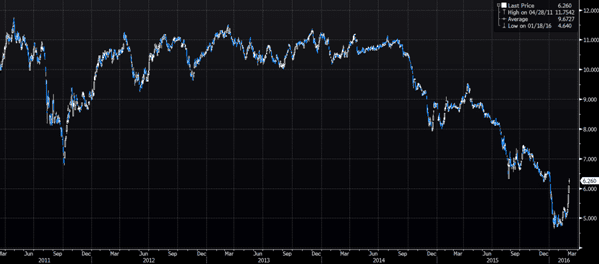

And the decluttering in 2016 has been good for the brain, if we had stopped to take a selfie 6 weeks ago, about the time for the personal investor selfie as we were running scared and running for cover on our equity investment in Keppel Corp, for example, when it was battered down 28% on 18 Jan (to a low of $4.64).

Market re-enlightenment has driven the stock price of Keppel back up nearly 35% from the low, to its current $6.26 level, begging us to question the reason for the Chinese “Monkey Year Madness”, when the uncluttered brain would have sought the rationale for a mean reversion trade.

Keppel Corp 5 year stock price chart

No sooner than as we stop to scratch our heads, Singaporeans shall be able to catch a rare sighting of a near total solar eclipse this week, at 90%, with the last total solar eclipse back in March 1821! The excitement will not end into the Ides of March as we speculate on the Singapore Budget 2016, coming uncharacteristically late on the 24th of March, just a day after founding Prime Minister Lee Kuan Yew’s first death anniversary.

Keppel long term shareholders may be relieved and new shareholders would overjoyed for their foresight in making that leap of confidence, yet it is not the same for the rest of the half comatose field especially when SGX, starting 3rd of March, put 41 mainboard companies on watch list because they do not comply with the minimum trading price requirement of 20 cents per share for mainboard companies or flouted the financial entry criteria of posting losses for past 3 years and having a daily market capitalization of less than US$40 million.

This is a hefty 24% increase from the last count of 33 listed companies out of the 900 we have on the mainboard as junked Noble got booted out of the the STI Index to make room for A3/A- rated Capitaland Commercial Trust.

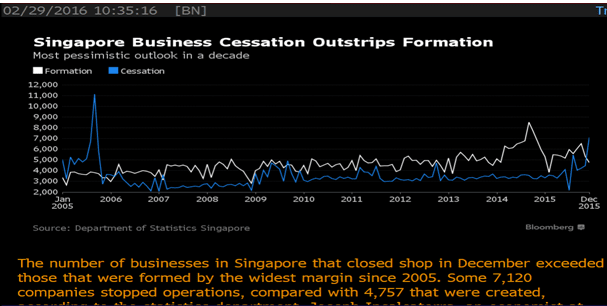

It is a sad reflection of the state of the economy as a Bloomberg news report cited Department of Statistics that “the number of businesses in Singapore that closed shop in December exceeded those that were formed by the widest margin since 2005”. 7,120 companies stopped operations, compared with 4,757 that were created!

Headlines are not as dire because GDP growth surprised on the upside for 4Q15 despite the business closures probably because small businesses hardly make a dent in the economy and the last unemployment rate number reported for 4Q15 was a healthy 1.9%.

The international trend is just as troubling with Moody’s tallied the latest number of distressed companies, which refer to companies 6 notches into junk, i.e. CC- and below, rose to a post-crisis high of 274 (vs April 2009 record of 291).

A rational mind would say that defaults should be making headlines soon and yet the US high yield default rate remains below its long term average of 4.7%, at its lofty lows of 3.1% now.

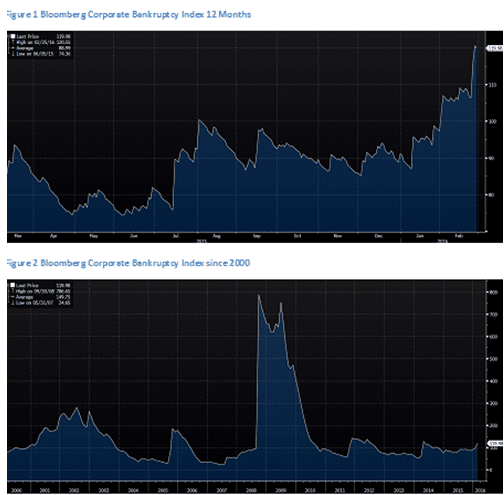

Taking a look the Bloomberg Bankruptcy Index, it would appear that we are seeing resurgence in corporate defaults or, more politely, restructuring which looks miniscule if we look at the big picture.

For the 5 reported major US bankruptcies in Feb 2016, the total liabilities only mattered about US$ 15.6 billion in total.

Decluttering and Simplifying

The equation has indeed become more complex with the odds increasing for a Donald Trump presidential run, oil prices, gold prices, lost thoughts on China, recession calls, central bankers in crisis mode as BoJ’s Kuroda speaks in their parliament daily, terrorism, disease, natural disasters and more.

The simple trend that I discern from the STI mainboard listings and business closures, along with the US bankruptcies and the S&P, is just that the small businesses will be the ones feeling the most heat as the world gets used to the ‘Too Big To Fail’ mindset.

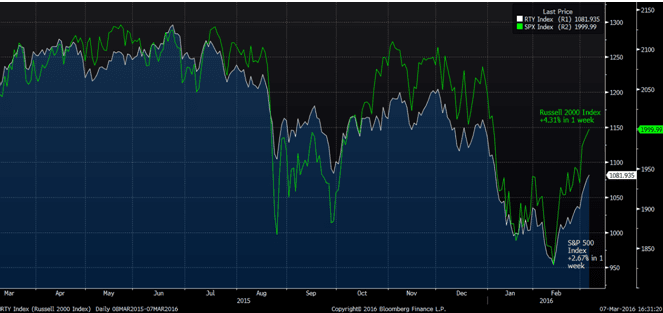

Keppel Corp is unlikely to visit its year lows in price from here but it is too early to trust that junk rally investors are piling into at the fastest pace on record last week, with $5 bio of inflows which should have led to massive out-performance of the small cap Russell 2000 Index, long seen as a proxy for junk bonds, against the S&P 500 over last week.

All timed nicely into the action packed week for opportunities that could be missed in the clutter of our thoughts or an eclipse over the Sun?