The Sharpe Investor Strategy

Looking back on the past fortnight, I realise that I have been writing on the recurrent theme of volatility and it is not often that I think too hard about my psyche (perhaps for fear of what I will discover?).

Humour aside, it dawned on me that I have been reacting to an inner instinct that is not unique because conversations with friends in the past week have unveiled a variety of concerns that all converge on the same uncomfortable feeling of a certain anxiety in our selves that we cannot seem to pinpoint to a specific source.

Maybe we were all, at some point, traders and carry the same cross of risk management ingrained at the backs of our minds, making the same risk-reward decisions daily as a second instinct.

So what is going on in our heads?

The volatility.

As I wrote last week, we are seeing inordinately large daily trading ranges in currencies and the second largest stock market in the world, China, Gold and government bonds, unexpected.

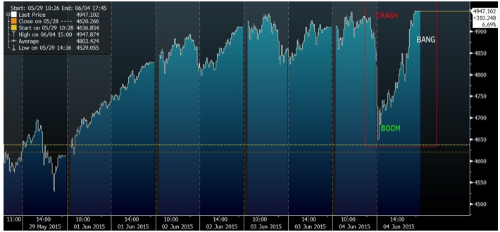

We saw a Crash, Boom and Bang in Shanghai Composite, within the same day, something that has not happened in years.

The market is clearly confused, uncertain and running on the extreme spectrum of fear and greed.

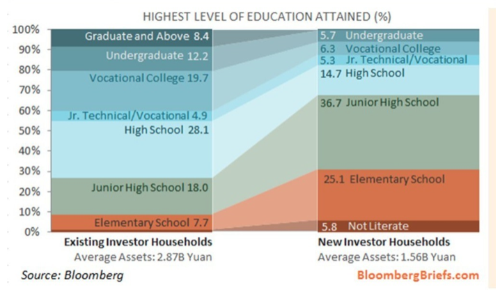

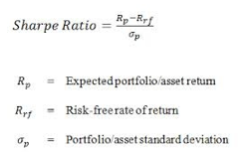

In such times, many of us dust off those old financial texts and pull out the chapter on the Sharpe ratio, that we should not expect half the Chinese investors to know about because, like we mentioned before, the literacy rate of the hordes of new investors is falling.

In simple terms, the Sharpe ratio is “a measure that helps investors figure out how much return they’re getting in exchange for the level of risk they’re taking on”.

How we do that is to take our returns or expected returns and divide by the standard deviation of market gyrations from historical norms. If the number is high, then the investment is worth keeping and a low number indicates that returns do not compensate for the risk.

As individual investors, the precision of calculation is not necessary like in my friends’ cases, rough mental sums are sufficient to cause unease.

What are my friends and I doing?

A portfolio manager with a small fund is switching into cash – 30%. That is a big decision to make because idle money pays no return and if left idle for too long, will underperform against benchmarks which would make his life a bit difficult when he accounts to his clients.

Another friend kindly documented his latest trades for our discussion, taking an interest in our self examination joke which warranted some soul searching, as we like to call it.

- Stock index hedges on the S&P and HSI

- Faded the A-share rally, selling most of his speculative holdings

- Sold calls (collected premiums) on 2823 HK (etf)

- Long USD via shorting the EURUSD

- Sold half of his HY bond portfolio

- Cut leverage on position reduction

- Increasing cash positions for both his bond and stock portfolio

We are both not in the extreme bearishness camp for sure, just like-minded in reducing beta and he is waiting to buy SGX bluechips in the coming weeks, a rather good idea to me because Singapore shares have suffered as investors pulled their funds out to pour into China.

On a Sharpe scale, the alpha returns should outperform the risk trades which is evident in for example, the HY bond rally in the past months.

Another aspect most people have forgotten to consider is the rise of the risk free rate.

The risk free return is the basis of the Sharpe ratio whereby investment returns are net off the risk free rate to arrive at incremental return which is then divided by the risk.

We have, for too long, rightly assumed that the risk free rate is zero and those times are coming to an end especially for countries like Singapore whose short term funding rates have shot up this year.

With global central banks done with their monetary easing or content with the current pace of their stimulus which is all priced into markets, it would be reasonable to expect that the risk free rate of return may not sustain into the future. Higher interest rates undermines asset prices because prices would have to drop to maintain their incremental return against the risk free asset.

Holding cash then becomes the key to bolstering the portfolio against loss. The portion of cash in the portfolio could be raised to 20-30% after reducing the beta or higher risk equity and bond bets. This is against the typical allocation in a regular investment portfolio which is about 5-10% in cash or cash equivalents which are usually in government treasury bills (SGD 6mths currently at 0.9%) or government bonds under 2 years in duration (SGD currently yielding 1.12%).

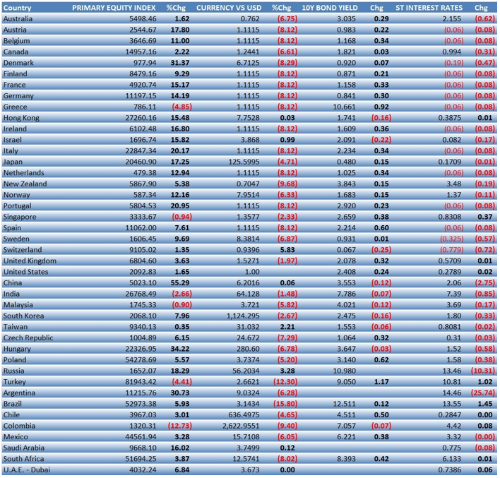

Let’s take a look at the market snapshot for the year so far.

We have come a long way with some massive moves that is becoming quite un-Sharpe-worthy.