The Triple Whammy of AAA Singapore’s Monetary Policy

I wrote about this last week but I feel a need to reiterate the point on Singapore, and with slight urgency on what I feel is a potentially profitable opportunity for investors in the near term future.

For it would appear that Singapore is vying for the title of the worst performing AAA market for 2015 at a quick glance at her markets and that would not sit too well considering that France and Japan both just got downgraded in the past 3 days.

Japan, for a single A country, is showing no worse signs for the wear with her currency gaining on the week and bonds rallying after the FOMC’s decision not to hike interest rates which begs the question, how did Singapore sink so low? To become the only all rounder AAA country where every market, be it the currency, equities, bonds and funding rates, is working against her?

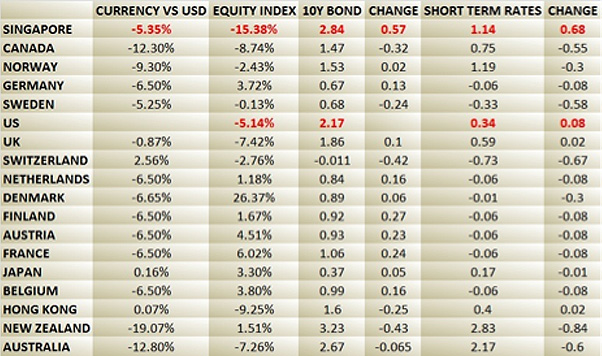

Taking a glance at a table I had prepared earlier last week, before the FOMC, we see that the rest of the developed world with some AAA rating to their credit has not done as badly even for the US which has only suffered minimum damage in funding rates while the rest saw decent equity market gains, or as in the case of New Zealand and Australia where funding rates fell, to offset the other losses.

Everyone has their theory about what is happening. Stock brokers will tell you its because volumes have not picked up since the Blumont scandal from Oct 2013 and IPOs have collapsed, economists will say it is because we have hit a snag in economic growth or that it is because of the funding costs, property agents will say it is because the housing market volumes have corrected substantially since the loan curbs and so on.

It is probably all true.

Yes the SGX has seen a change of leadership in the past months, economic growth is looking suspect with the latest Non Oil Domestic Exports seeing their worst decline in 6 months which is putting GDP at risk, property indices have come off, funding costs are at 6 year highs along with most bond yields, bank loans are not growing and IPOs have dried up.

New Territory

Our quarterly GDP has only been worse 12 occasions since 1975 ie. 12 out of about 160 times with the last brief dip in 2012 and our last technical recession back in 2008 which was saved by the not 1 but 2 casinos.

There is little growth story left on the plate as we have pointed out a few months ago.

The government set the alarm bells off in January with a surprise weakening of the SGD, catching the market off guard and the markets reacted in a bad way presupposing, quite correctly, that the situation was more dire than it looked.

It is easy to say this on hindsight because the other reaction, which would have been natural as it was back in 2008, was that it would be a once off event and the SGD would strengthen back thereafter. Yet, it was not easy to expect the other central banks of the world to panic, largely on the ECB’s and Greece’s accounts, and to start on mini rate cut currency war.

The SGD Dollar Policy

The SGD dollar is a unique creature, being the only currency in the world to follow strictly to a NEER basket which is an informal peg against a basket of currencies which, in Singapore case, comprises of the USD, MYR, CNY, EUR, JPY, AUD, THB, TWD, IDR, GBP, KRW and the PHP, in order of importance.

Thus, an informal peg of sorts. Adding to that, we also have the non-internationalisation of the SGD policy (MAS Notice 757) which prevents the SGD from being borrowed directly for offshore purposes unless the proceeds were first swapped into any other currency. In other words, SGD could be borrowed only for onshore purposes and one has to have the SGD dollar on hand before taking it out although there is no limitation on how much one can borrow to buy SGD assets.

As such, while everything about Singapore is considered first world, the SGD dollar is classed under the EM category as far as many international portfolios were concerned.

The direction of the peg is determined by the MAS which has only adhered to the simple rule that it shall be inflation led.

For the past 15 years since the formalisation of what is called the Exchange Rate-Based Monetary Policy with semi annual monetary policy statements, the stance has always been for a modest and gradual appreciation of the SGD dollar.

The reason for the constant appreciation stance is appropriate given that, for the lack of natural resources, inflation would always be intact.

And for that, all foreign investors would be rewarded with currency gains which has been the case since 2001. The SGD is the world’s 7th best currency pair (against the USD) in the past 15 years ranking only behind Gold, Silver, CHF, CZK, CNY and NZD and giving an 18% return which does not sound like much especially if you compare it to 12 months ago where the SGD gave a 31% between 2001- Sep 2014.

The Interest Rate Conundrum

A unique monetary policy begets unique effects.

Having a strong SGD meant that inflows would exceed outflows for the purpose of currency gains, the result of which meant that buying a SGD dollar in 3 months would cost more. That resulted in negative forward fx swap points.

Now, without a central bank determined interest rate, the only way to derive short term rate fixings for derivative contracts would be to strip the implied rate from the fx points with the aid of USD Libor to give Singapore reference benchmark, the SOR (Swap Offered Rate).

Conversely, if the SGD was on a weakening trajectory, the forward fx swap points would be positive which would result in a higher SOR.

This is where the conundrum lies. If a strong SGD was the result of higher inflation, it actually meant that interest rates would be lower and vice versa for lower inflation.

Economics 101 that is used by the other central banks suggests rate cuts for lower inflation to stall its fall and keep it at a healthy level. With the opposite happening in Singapore, higher interest rates act as a deterrence to the already falling inflation which bodes badly for rents and asset prices even as import prices rise on the weaker currency effect.

The Triple Whammy

Couple the weaker SGD with potential outflows for the lack of currency gains and then couple that again with the lack of a growth story, we end up with a triple whammy on the currency front which is also a triple whammy on the interest rate front which leads to even more problems on the economic front for stock and bond prices.

Now tell me if that is not why Singapore is “the only all rounder AAA country where every market, be it the currency, equities, bonds and funding rates, is working against her?”, all due respect to Blumont and the housing loan curbs.

Is this time to rise up to the occasion to take that investment plunge into that AAA status as Singapore-bashing continues into the next monetary policy statement in about 3 weeks time?