Missing Out on En Blocs and Singapore’s October Monetary Policy Statement

– Most Singaporeans are missing out on the en bloc mania as a disconnect in property prices emerge between the real market and the en bloc market.

– It still makes property stocks a screaming buy as we said 3 months ago, now with added credence from the presence of Chinese developers and deals going through despite the new levies that hit the market on 1 Sep.

– The MAS monetary policy statement is set to be released on Friday the 13th of October.

– Casting back to SG 50 in 2015, MAS MD painted a less than comfortable picture of economic restructuring between 2011-2025.

– Kudos to MAS for having the foresight of having just 2 monetary policy meetings a year vs the Fed, BoJ and ECB with their 8 meetings.

– Since April 2016, the MAS has moved to a zero currency appreciation stance which has flat-lined the SGD NEER index but not expectations for the days of appreciation to return as evidenced in the SGD forward points.

– In October 2016, MAS added “extended period” into the language of the policy statement suggesting that zero appreciation may be needed for longer and surprised in April by leaving “extended period” intact.

– The market grows impatient for the days of appreciation to return as MAS has been ever-appreciating the SGD dollar in the past decade and more.

– We think MAS is not missing out much if they stay pat and we will not miss out much if we have already missed the en blocs.

A good friend of ours commented about her deepening fear of drivers on the road after experiencing a car accident that was no fault of hers, as she was hit out of the blue, on high impact, when she was just minding her own business on the road. Now she has developed an aversion for other drivers, as we observe negligent and reckless driving on the rise as our streets fill with private hire cars and we train ourselves to automatically give those Vezel’s a wide berth.

Yes, accidents happen, as they say, although we would not believe those statistics out there telling us the probability of getting in a car accident in Singapore is decreasing because we have much less roads (just over 3,000km) here than elsewhere, therefore if we go by accidents per km…

Yes, accidents happen, to innocent concert goers in Las Vegas last weekend and in Manchester 6 months back, its pernicious effects linger for those survivors, as emotionally scarred as refugees or victims of hurricanes that we have forgotten about as we go about with our lives.

The biggest fear this week for most of us living in salubrious Singapore, where the main gripe is either with the MRT or the lack of the extra public holiday due to a non-election, would be the fear of missing out again.

The Fear of Missing Out in those En bloc Sales

As en bloc sales dominate headlines with 2 major ones this week, some folks ruefully lament that their prime Bukit Timah condos remain offered at $1.4k psf when Amber Park on the east side went for more; dishing out windfalls for others, with the latest en bloc of Normanton Park going at double the last transacted price and some owners there are lucky enough to own more than a few units.

Source: The Straits Times

Property counters rose in a euphoria on Friday, after it was decided that the Chinese led consortium purchase of Normanton Park, at the highest land rate for a 99 year leasehold site, was a good sign for all the other 24 deals done this year and companies like UOL packed a 4.3% one day gain to lead the pack.

The logic is foolproof and simple. If the en bloc sales are at post-crisis highs and going through despite the recent hike in punitive development charges on 1 September, the Chinese are coming in and JP Morgan thinks it is sustainable, it stands to reason that property developer stocks are a screaming buy!

Source: The Straits Times

And it is like what we said 3 months back, for the fear of missing out, when we wrote It’s Obscene – Let Them Buy Real Estate, We Buy Real Estate Companies.

Are We Missing Out On The Monetary Policy Statement?

The rest of us, comfortable in our investment portfolios and missing out on the last 3-4% rise in global equities, now fret if the decision to stay underweight was flawed in reason and that stocks will continue to capitulate higher, rewarding those “lazy” passive investors.

Yet, we have come a long way from April and the last Singapore Monetary Policy Statement (MPS), mostly beaten into submission by the markets, feeling overwhelmed by global geopolitical developments (or disintegration), an inordinate number of natural disasters, acts of terrorism and all this new technology invading our lives, privacy and interfering with our personal choices that are now under the threat of viruses, hacks and virtual attacks.

In the midst of onshore en bloc sales fever, the stars are aligned for the semiannual MPS to fall on Friday the 13th.

So far, we have kept our eyes, ears and heads clean of any research, strategy and analysis, because we believe that anyone worth their salt would not be writing about the MPS unless, of course, it is their jobs to do so. Harsh words, but there has been nothing really interesting about Singapore since 2015 and SG50 when MAS MD Ravi Menon painted a picture of slightly uncomfortable economic restructuring between the years 2011-2025 for us.

We feel the same as in April, when we wrote SGD April Monetary Policy Statement: April Is No Fool, that “we cannot help but pity those central banks with policy meetings 8 times a year like the FOMC, BoJ and the ECB, or the RBA at 11 times a year! And congratulate Singapore’s MAS for their foresight in anticipating the need for only 2 policy meetings a year”.

While we were wrong to expect the negative funding of the SGD dollar against the USD to bite into currency speculators, or perhaps lack of, the SGD dollar did “adjust back lower from its overvalued levels against the rest of the basket currencies” as MAS kept the “extended period” language in their April statement.

Source: MAS

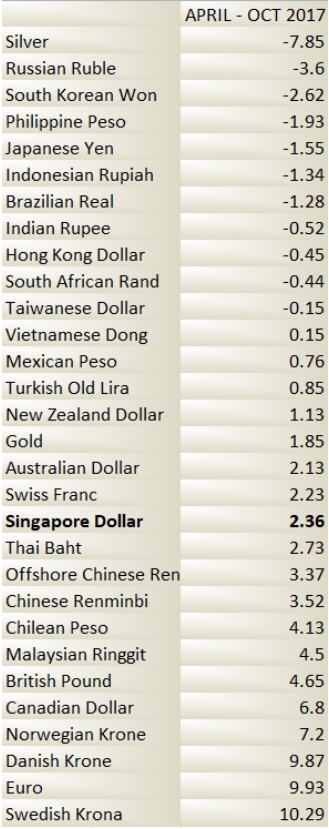

Checking out the relative performance of the currencies against the USD below, the SGD dollar underperformed against the Chinese yuan and Malay ringgit (Singapore’s largest trading partners) in the past 6 months, rising just a modest 2.36% against the US dollar although we would be slightly baffled by the SGD’s larger rise against the US-pegged HK dollar.

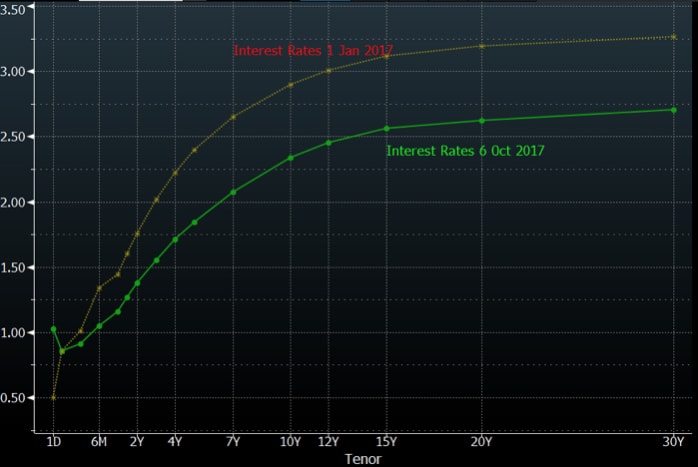

The big tear between SIBOR and LIBOR continued to widen slightly with Singapore taking little cues from rising US rates and local rates remain much lower than where they started the year at, giving us little hope for higher CPF interests too.

Singapore swaps curve change, year to date.

The verdict is that nobody missed out on anything much in the past 6 months and it has not been terribly exciting except for the en blocs (and train breakdowns).

The Quick and Dirty of Friday the 13th’s MPS

The 6-month SGD forwards are pointing to the possibility of MAS tightening ahead, with discount points trading much more negative than April, and most negative in the past 5 years. The collapse started right after the April 2016 MPS and the zero appreciation stance which has seen the SGD NEER index flat-lining for the past 18 months, as we can observe from the graph below.

Graph of the USDSGD vs the SGD NEER vs the 6M SGD fwd points since 2011.

Why?

Because MAS has a track record of ever-appreciation! Again, on foolproof reasoning, the country does not practice monetary policy and the only way to manage inflation is via the foreign exchange policy and in the past decade, there was only 1 occasion of depreciation in April 2009, in the midst of an 18 month stretch that saw neutral (zero appreciation)policy stances before the SGD went back to its strengthening path.

If MAS does nothing this time, i.e. keep the zero appreciation stance, it would be the longest stretch of non-appreciation we had since the period between Jul 2001-Oct 2003, and we can certainly see that happening in 2017, with years of economic restructuring lying ahead of us.

The quick and dirty points on Friday the 13th’s MPS, written for posterity.

- More central banks in the world have cut rates in 2017 than raise

- The unwinding of central bank balance sheets would tantamount to a rate hike and liquidity withdrawal but that would take time to play out

- Time is not of the essence in rate hikes because inflation is not running away

- Signaling intention to return to the path of appreciation would bring back the “unwholesome” speculators and we really do not need these types of investors hanging around. In fact, it would be a boon to the Chinese who will come in for the en blocs to see their profits soar just on currency appreciation

- The credibility of MAS’s “extended period” language would be challenged, to be redefined as 18 months?

- In the face of uncertainty, Singapore would do well to just play along with her largest trade partner—China and her role model—Switzerland.

Verdict—there is not a lot to look forward to in terms of surprises, if you ask us.

Missing Out is a Bad Feeling

Yes. Property is all the rage again and some lucky owners of en bloc properties are reaping the rewards even if some had endured years of abysmal rental returns.

Yes. There will be massive repricing coming up for those Bukit Timah condos going at $1.4k psf as they find themselves buyers who have cashed out of Tampines and Normanton Park, bringing a nice car in tow perhaps to celebrate their windfalls.

Yes. The monetary policy statement is a misnomer of sorts because it is actually about the currency’s value and relative strength.

It is the 1 year anniversary since MAS injected the “Extended period” for zero appreciation and folks are getting edgy and yet it is too hard to envisage the MAS going back to the path of appreciation just to heat asset prices up further that will not go towards creating meaningful jobs and investments.

We will not be missing out, too, if we have already missed the en blocs.