1H16 Market Thoughts: Did Somebody Die?

With worries mounting daily, the latest being BREXIT fears, markets are mighty lucky mass hysteria has not broken out for the lack of a potential hard landing for the global economy. Putting a perspective on the year, we are not living in more fear of a recession than we were for the uncertainties back in 2008 -2011 and we had financial markets peace between 2012-2015 when the Fed announced that they would maintain the Fed Funds Rate near zero “at least through 2015”.

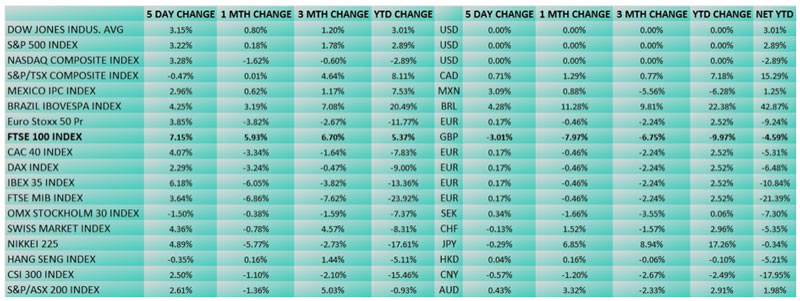

The final week of 1H16 has been one of guarded optimism as equity markets reversed their courses, in an unhealthy expectation of stimulus to be expected from the Bank of England, which cannot possibly match Japan’s on scale, for sure, and yet a nice-to-know fact that turned the Footsie Index into the best DM (developed market) performer for the week, the month, second quarter and the year – up 5.37% since January compared to the Dow Jones +3%.

Fortune favours the brave? And we have the investors like George Soros short Deutsche Bank stock (-6% for the week) and someone else long Gold (+2% for the week) to manage their Brexit pains when the unassuming winner from this has been errr, scandal-plagued Brazil which managed to ekk nearly 9% returns as a stock and currency investment in just a week and winning hands down for the year at 42.87%, stocks and currency combined, making Gold’s 29% gain for 2016 look slightly paltry.

In essence, we have half the world behaving like somebody has died and the other half, hard at work, behind the scenes, putting their money to work which teaches us a fine lesson on reading too many bank reports and news stories telling us that the end is nigh and we should be on alert.

For all it is worth and so much for the gloom and more gloom that appears to be affecting the bankers and central bankers we meet and hear, the year has been pretty fabulous for every single asset class except equity markets and Deutsche Bank shareholders (-44% year to date).

6 months ago, it was a different story with bankers calling for a Crude Oil collapse to $10 (the most dismal forecast I came across), the world was expecting a spate of oil related corporate bankruptcies,

China to capitulate, investors were advised to hoard the USD and dump their gold while expecting 2.5 Fed rate hikes for 2016.

I called for a “selfie moment” then, when 2016 was looking like the hardest year to make money in 79 years, after its first fortnight right after 2015 was officially declared the hardest year to make money in 78 years.

When I wrote “Analysts are now trying to outdo each other in predicting how badly Keppel and Sembcorp Marine’s order books will take to the rout in Brazilian O&G companies, calling for 30-70% of orders being cancelled, none too worried about their cash positions, sitting on their billions in cash with little due in terms of loans and bonds (Keppel none in 2016 and Sembcorp, S$ 224 mio).”, I had not expected Brazil to outperform oil by that much although I did say that Keppel Corp has seen its price lows.

Nearly 6 months later, with Crude Oil up 32% for the year, we would think our troubles are over except that we have newer and bigger problems at hand. For you see, it was not too hard to see the fault lines like the ones I wrote about in December 2015 in the spirit of the Ghost of Christmas Yet To Come.

No. We cannot say it has been easy for 1H16 has been a hard fought battle compared to the relative lull we had for the past 4 years just going by the number of times the VIX (volatility) Index broke above its 10 year average of about 20.5 and the official bear equity markets scare we got earlier in Jan-Feb.

Weekly candlestick chart of the VIX Index

Weekly candlestick chart of the VIX Index

The volatility of 2016 can only be attributed to an underlying theme of discordance or discord in the marketplace, where opposing views clash as much as political views are doing right now in the US, UK and much of the world.

It can only be described as unhealthy by the observer, if bonds are delivering healthy returns with many displaying double digit returns mainly from capital gains in their yield collapse or price gains. When inflation is near absent, or diminishing quickly, even as commodity prices rise, signals confusion. When the Bitcoin becomes the best performing asset (+56.75% year to date), doubling the return on safe haven Gold (+26.41% year to date). Most of all, when basket-case Brazil, still mired in its worst recession amidst political instability, the Zika virus and corporate scandals, becomes the best performing market, currency gains included or excluded, in the investment world for her bonds, equity market and currency.

When I asked my good friend, a trader, what she thought of the mini Brexit crisis, for she has seen too many of such before, the response was “Has somebody died? If no, then it will be business as usual.” None of that “this time is different” views that we read about from those who gunning for fame or even the tempting “buy into the crisis” trade that some have been chasing after.

Yet I can sheepishly, but coolly, confess that I believe the second half of 2016 will probably be different from the first because the realisation that “nobody has died” will set in and while the Bankruptcy Index is at its highest since the Lehman crisis, large scale defaults will be hard to produce with such accommodative monetary policies.

While central banks will be in the spotlight in the coming weeks, they would be more than aware that further quantitative easing is likely to be doomed purely on market rejection which leaves the $20 trillion worth of negative yielding bonds out there at risk except for the fact that they are mostly held by now introspective central banks such as Japan which is closely studying the effects of negative rates, possibly ending our hopes for double digit returns in bond markets in the next half year.

I would hazard a guess that currency wars will be avoided if central banks stay put and we will be in for a long grind, skirting with recession as economies re-inflate amidst rising social tensions which is a good time to stay in solvent assets as our faiths in the US dollar, bonds and equites get tested into the US Presidential elections in November that promises to be a discordant affair, much more than the previous elections.

Nobody has died and we are still mired in a period of secular stagnation with little cause for optimism or greater cause for panic.

Happy Independence Day to Americans!

Revisiting Some of the Themes Identified in the Past 6 Months.

1. An Obituary For QE = QF (Quantitative Fail)

“The International Monetary Fund is increasingly alarmed by signs that market liquidity is drying up and may trigger an even more violent global sell-off if investors rush for the exits at the same time…

He warned that investors and wealth funds have clustered together in crowded positions. Asset markets have become dangerously correlated, amplifying the effects of any shift in mood.

“The key issue is that liquidity could drop dramatically, and that scares everyone,” he told a panel at the World Economic Forum in Davos. “If everybody is moving together we don’t have any liquidity at all. We have to be ready to act very fast,” he said.”

2. It’s Just Too Hard To Think About Central Banks

“We have reached a new era of unknown repercussions from policy actions and ineffectual central banks….. It is likely that markets would take more kindly to news of Kuroda resignation than further policy action at this rate because a regime change would inject an element of hope rather than throwing in even more good money after bad.”

3. The Little Gold Sovereign

“There is little compelling reason not to be bullish Gold with US$ 1,330 in sight and a little head start over the rest of the market that has yet to understand the repercussions of this year’s policy actions.”

4. Sugar Highs To Beat The Inflation Blues

“As for the low cost third world commodity producers, the set back from lower prices will mount as wage costs will increase. The eventual rise of wages will have to be made up in in the form of higher prices which is an inevitability for low cost labour.”

5. No Business Like Bond Business As The Curtains Fall

“And as my friend and I laugh at the “gangsta” bond markets and all the horror stories we hear from investors and insiders; companies that should not be allowed to issue bonds end up selling out their issuance, only for prices to collapse nearly immediately and; the random, baseless prices quoted by the traders left out there, mark-ups that will shock characters in Liars Poker, it does seem like the colourful bond business can compare to show business as major bank withdrawal continues and the curtains come down.”

6. Retail Bond Renaissance – Everyone A Winner

“Bond math is not that hard but it becomes difficult when people are buying bonds based on their dirty prices, unaware of ex-coupon dates, and with the unreasonable expectation that bond prices do not change. The worst case of misrepresentations that I heard about recently are clients who assume their investment yield is the bond coupon and the sales people who knowingly sell discounted bonds to their clients at 100 because it is easier to explain than better stuff that is trading above the 100 mark.

Yet, that still makes everyone a winner, if you ask me, because the retail markets get what they want, my greedy friends will have a field day and the Singapore bond market will get her renaissance.”

7. To Know Your Ironies

“The key irony is that “Secured creditors recover only less than 33 cents on the dollar from insolvencies in East and South Asia, compared with more than 80 cents in the U.S., according to World Bank studies.”

Secured creditors are ranked above senior bond holders.

Does this suggest that Asian companies are more risky investments with 33% recovery value compared to 80% for the US? A more ineffective judicial system? Or, just more dishonest companies around issuing bonds?”

8. The Monkey Business of Real Estate

“While I am sorely tempted to encourage folks to do the same as we did last April to get “the most mileage on the investment via leverage and the currency of leverage.”, the message today is to break down the risk for people who toying with the idea just to get ahead with those tempting negative interest rates. A carry trade is all about making that foreign exchange call. “

9. Living And Banking In Fear

“The Fear of Negative Rates (and Recession) breeds in the strangulated banks, who are turning away deposits (and loans) in the developed world, including Singapore. Banks are closing down their bread and butter trading and lending businesses too because of regulations which negates the effect of negative rates!

10. The End of An Empire and The Risky Banks

“In other words, shareholders can safely assume that too big to fail means too safe to fail and the days of wild profits are over and these institutions, particularly the heavily governed ones, can be viewed as government regulated agencies and socially inclined enterprises instead, quite unable in engaging risky behaviour. Would that not mean that GSIB banks are potential safe havens with implied government aid as a last resort? Even as politicians still seek to vilify them for their personal agendas for the sake of populism?”