2015 by The Ghost of Christmas Present

30,000 feet up in the air and reminiscing on the year, humming along to the song that we had dedicated to 2015 just 12 months ago, Bittersweet Symphomy by the Verve. A classic piece that is mired in controversy with the Rolling Stones claiming plagiarism, thus living up well and truly to the not quite dark chocolate version of bittersweet which is rather apt on retrospect.

2015 was mayhem from start to finish as we said earlier this year.

Resonating Chaos

2015 will be a chaotic year, with nothing for certain, 7 years after the global financial crisis.

It is the end of the easy monetary policy era that was funded by the US Fed as the QE taper of October 2014 continues to impact fragile developing economies.

The currency wars will continue as Europe and Japan seek to weaken their currencies which gives another excuse for the USD trade besides the rate hike story.

Lower oil prices will be beneficial in due course but we should expect to see, 1. slippages i.e. benefits not accruing directly to the consumers and, 2. credit defaults and/or credit widening that will hurt the borrowing economies (mostly EM) and corporates…

I was mid way in my writing when the news of the Paris attacks broke*. Yes, 2015 shall see a lot more of these little outbreaks of violence which has been brewing since last year – Sydney, Canada, NY shootings, Ferguson and now, Paris, although I am not sure if HK counts.

Social fabric has been asunder-ed by the stress of housing 7 billion people on Earth, each wanting to have a piece of it along with the enviable lifestyles of the rich and famous that is paraded each day in social media.

For my grievances against tech, I still hold bullish on my long term calls on robotics and fuel cells as I have written about last year. The jobs of tomorrow are gradually being lost to robot waiters and drone delivery men. It will not happen all in 2015 but I am certain it shall start. Giving up on bonds is easy enough as stuff worth buying deliver worthless yields to the retail investor who needs the absolute returns. Pitch this against the funds and central banks who do not need those returns and we have a polarised and disgruntled marketplace.

And so the theme of equities and high grade bonds is an easy sell for most reports we have gotten in our in-boxes because corporate cash levels are at all time highs, profits are returning to health and inflation is expected to be kept in check.

*Paris terror attacks on the offices of Charlie Hedbo

2015 has been 2014 in parts.

2015 In Review

There are so few positives in markets for 2015 and hardly a bright spark to close the year on as we await the first Fed rate hike in a decade.

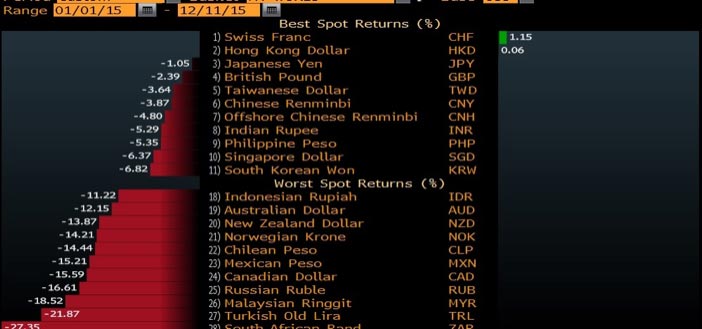

Forex – The most over exposed trade of the year to end on a high note as the USD reigns supreme which started with the SNB giving up on its EUR peg that cost many a hedge fund trader their jobs and we are ending on a low note as “Parker Global Currency Manager Index of top funds has lost 0.7 percent this month to extend its slide in 2015 to 2.7 percent. That puts it on course for its worst annual decline since 2011.“

Adding up the returns over 5 years and Asia looks on better ground, especially Singapore and South Korea.

Equities – Pay little heed to those China naysayers because the Shenzhen Composite is the best performer in the world this year, returning 55% year to date, beating Iceland (+36 %), Ireland (26%), Denmark (29%), Hungary (39%), Slovakia (32%), Latvia (+42%) and Argentina (48%), among others unless we have to include Venezuela, mired in hyperinflation for toilet paper and an 800% inflation which makes the 288% rise in equity markets, a little farcical.

China’s equity market scare, subsequent interventions and continuing dragnet that spares none ends the year on heightened unease. This includes last week’s disappearance of one of their richest men, Guo GuongChang, owner of Fosun International (656 HK), said to be detained by antitrust authorities which is becoming commonplace in China with only members of the current Politburo safe, given that they are coordinating these “detentions”.

Equity markets have been in defense mode for the past months with a sagging growth story, along with currency markets. Stock buybacks have been artificially boosting the earnings per share but even that is expected to wane with financing costs on the rise. A cynical comment from Doug Kass on the mega merger of Dow and Dupont to create a US$130 billion chemicals behemoth, which can be taken to refer to all mergers we are witnessing.

Bonds – It is a tale of 2 yield curves.

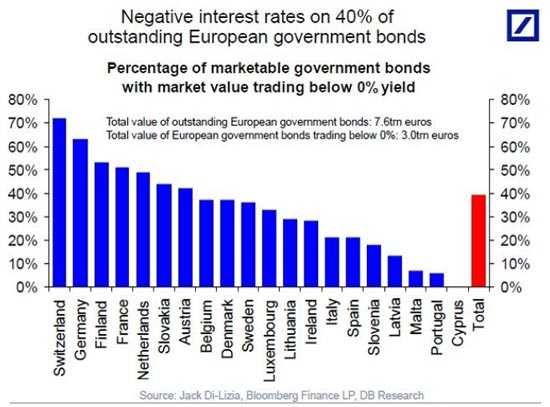

In Europe, we have 40% of European government bonds trading under 0%, which is hardly healthy as we read astounding reports that some Danes are discovering that their banks are paying them every month to borrow, instead of charging interest on their home loans.

It will get worse next year as new rules and more new rules bite in Europe giving regulators the right “to write down the value of senior bonds or convert them into equity to help bring a failed lender back to life” along with more capital requirements.

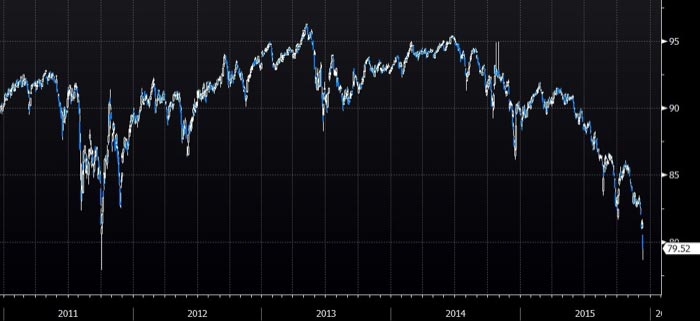

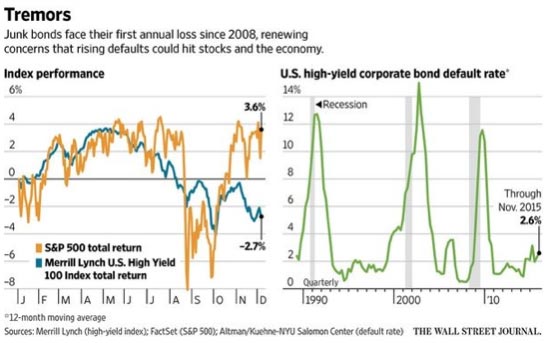

And the meltdown in junk bonds continue on poor liquidity exacerbated by worsening credit metrics. The HYG ETF of USD high yield corporate bonds has closed the week on a new 4 year low and are set for their first annual loss since the crisis in 2008.

“In most high-default periods we’ve seen in the past, the rise in default rates precedes a recession.” According to WSJ and with “the stock of dollar-denominated debt has roughly doubled since early 2009 to over $3 trillion,” there can only be more pain to come.

Commodities – it’s a bloodbath. “Aluminum is having its second worst year in history and gold is having its sixth worst year in history…”

With oil prices closing on a 7 year low this week, we read predictions for US$ 20 a barrel for the months ahead even if the forward prices are holding above US$ 40 for Jun 2016.

Real Estate – finally popping in London and Australia, both places registering declines, at last. “The Home Value Index for November showed that home prices fell by 1.5 per cent across Australia’s capital cities over the month.” and a property baron predicting that “Next year…. London property prices will crash.”

Till 2016…

The motto for 2015 was.

Carpe diem quam minimum credula postero: “Seize the day, put very little trust in tomorrow.”

And the Ghost of Christmas Present is omnipresent in our midst, in probably the most anticipated month of the year as academics and historians wait excitedly to document the market effects of the ending of the zero rate policy in the US.

The 2016 theme would be “Come, my friends, T is not too late to seek a newer world,” for it shall be a quite an odyssey ahead.

To be continued.