An Obituary For QE+QT=QF?

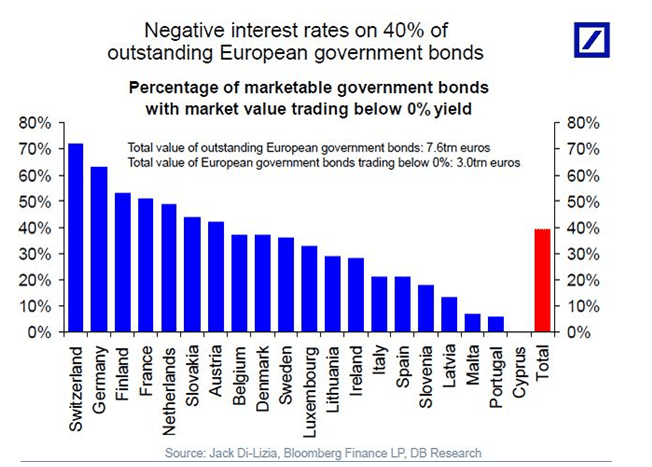

First, they cut and cut until there was nothing left to cut. Then they bought and bought till the yields turned negative and we mean 40% of Europe government bonds are now yielding negative.

Negative rates are unnatural? Yes. Excel has no formula to compute those and it is a challenge on our realities especially when central banks are breaking ranks in an epic Clash of the Titans scenario as the Bank of Japan decides to cut rates to negative, implementing a penalty of -0.1% on certain excess holdings of cash, a month after the Federal Reserve decides to hike interest rates for the first time after nearly a decade.

This whole QE then QT (Quantitative Tightening) business is becoming a QF—Quantitative Fiasco or F for Failure, but Failure is a relatively difficult concept for economists to grasp in their shades of grey spectrums.

The plain truth is that the market has concluded that QE has lost its effectiveness in the broader economic picture and only succeeded in creating a bond market bubble of epic proportions that has led us to the current state the bond markets, dysfunctionally trapped in a liquidity stalemate that has extended to even the most liquid bonds of all, the US Treasuries, where “buyers are gravitating to the newest, easiest-to-sell debt. This year, investors are paying almost twice the average premium to own the most-recently auctioned 10-year notes, known as “on-the-run” securities, instead of “off-the-run” ones issued just a few months earlier”.

In September 2015, we noted that there were 5,000 hard currency bonds globally that yielded over 6%, the market accepted level for high yield back in the hey days of QE. That compares with just over 1,000 bonds we could find earlier in the year. Now we have over 10,000 hard currency bonds yielding over 6%, 8,000 bonds yielding over 7% and 5,000 bonds yielding over 10%.

At the same time, we have over 10,000 bonds in the world yielding negative returns! 5,500 of them in EUR and 1,447 in CHF alone, including another thousand in JPY.

As we said last Christmas, the themes that will haunt us will be that of the Have’s vs the Have Not’s.

1. The wealth gap in society is keeping the billionaires up each night as billionaire hedge funder Paul Tudor Jones thinks it will end in either higher taxes, revolution or war.

2. The good borrowers and the bad borrowers is alienating the bond markets as companies like Apple borrow at near lows in rates while the hard hit oil and gas associated companies are unable to refinance. Home ownership rates are lowest since 1967 in the US because of decreased affordability.

If we had to guess how bad it is, the credit worthiness is best illustrated in this chart of Global HY spreads against, IG spreads and sovereign spreads where the trend is clearly broken, observing that sovereigns are paying near lows to borrow, at 0.15%, as compared to HY funding costs which has risen 50% in the past year and about 30% for the IG names.

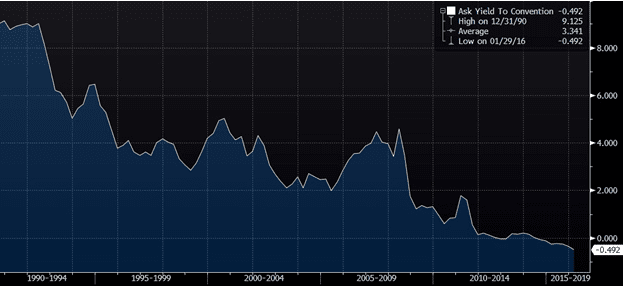

It has been 18 months of negative rates for Europe with the German 2Y bund’s yield at its historic low as we speak at -0.492%. Japan has also seen 3 months of sustained negative yields for its 2Y bond.

Challenges

1. More than hard enough for portfolios to stomach, it is even harder on the individual sense of reality where bank balances are eroded daily as society is taught that saving is a bad thing as if we do not need reminder there is about $ 29 trillion of corporate bonds out there for us to buy with corporate leverage at a 12 year high and 1/3 of global corporates are failing to generate high enough retruns on investments to cover their cost of funding.

2. A good enough reason to buy more of those negative yielding bonds on a flight to quality that is perhaps a misplaced belief even if global inflation rates for most economies are trending under 2%? Unless we move into deflationary territory, there is no logical reason to buy a negative yielding asset unless it is for the express purpose of profit when yields become more negative which essentially assumes there is a buyer willing to risk the loss of holding onto a negative yielding asset.

3. James Rickard: “Gold has zero yield. That means it has a higher yield than bonds from Germany, Japan, Switzerland, Sweden…”

4. “The International Monetary Fund is increasingly alarmed by signs that market liquidity is drying up and may trigger an even more violent global sell-off if investors rush for the exits at the same time… He warned that investors and wealth funds have clustered together in crowded positions. Asset markets have become dangerously correlated, amplifying the effects of any shift in mood. “The key issue is that liquidity could drop dramatically, and that scares everyone,” he told a panel at the World Economic Forum in Davos. “If everybody is moving together we don’t have any liquidity at all. We have to be ready to act very fast,” he said.”

A Quantitative Fail!

It would be easy to say that it is China’s and oil’s faults and Europe can blame those refugees too but deep inside we all know that there is something unnatural about negative rates and the aimless borrowing to fund share buybacks.

And the biggest risk would be one of assuming that negative interest rates are here to stay and there is safety in those instruments of negative or low rates because it is a crowded position and the crowd, including central banks, cannot be wrong. Yes, it would be wrong to go down that rabbit hole because markets are acting out the script for the obituary of QE and its sequel of QF. The corporate bond universe is already paying the price, when will governments start?