Imagine an Asset Light Model into the US Presidentials

Modern leap years all have the following in common—The US Presidential elections, the summer and winter Olympic Games and the European football championships. This year we got more than our hands full with Brexit, shortly after the longest-reigning British monarch, Queen Elizabeth II, celebrated her 90th birthday.

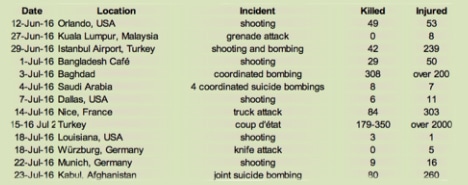

Nonetheless, this must be the most doleful Olympic games in my memory, plagued by the shadow of the Zika virus leading to the absence of a long list of top athletes; missing the entire Russian contingent; and against the backdrop of rising incidences of terrorism and not a week has gone by in the past month without some attack or other globally, acknowledged or unacknowledged acts of terror, some lone acts, some disputed and some closer to home.

With the 2 US Presidential candidates now officially selected, the ordinary American must surely be more worried than ever, having 2 candidates whose reputations precede them by a mile quite unlike the naïve populist choices found in Obama, Modi, Jokowi and Trudeau. Yes, the average Joe must be feeling most helpless and betrayed by their constitutional election process, mocked into having to choose between, as some observers put it, a “mad man” and a “liar”, whose ideals and agenda are likely to tear asunder the social fabric of the 300 odd million Americans.

For the record high in the S&P 500 that we are living through, we are challenged by downward revisions in global GDP by the World Bank and more difficult than ever to see the glimmer of hope in the near future with global politics in discord, it does look like we shall we in the same quandary as American politics which will be stuck in a rut for the next 4 years until their next Presidential campaign as Jeff Hirsch of the famed Stock Trader’s Almanac said in January this year, ‘The market is not really enamoured by any of the prospects for the next resident of the White House.”, not especially when tweets from Hillary Clinton managed to tank biotech and pharmaceutical stocks in September 2015.

Taking a page from anecdotal evidence, according to the Stock Traders Almanac, election years used to be the second-best year of the four-year presidential cycle yet, “Since 1920, however, the eighth years of presidential terms have represented the worst of election years. While the Dow Jones Industrial Average has posted an average gain of 4.8% in election years since then, the last year of a two-term presidency has been down an average of almost 14% on the Dow and about 11% for the S&P 500 according to the Almanac, with losses in five of the last six times a two-term president was finishing up.”

11% would put the S&P down some 350 points from here, a nice number of 1,818 into November.

Does it give cause for concern for the statistically inclined investor? Especially when the post-election year has always delivered the weakest returns since 1900?

Geopolitical uncertainty has already crushed some companies and their earnings, with Rolls-Royce coming out this weekend to take a $2.6 bio write-down on the sterling pound’s weakness since Brexit. Lufthansa and other European airlines are warning that growing terrorism will affect earnings as airports become high risk zones (Brussels airport attack in March and Istanbul airport just a month ago) and tourist spots are shunned after Tunisia (last year) and Ivory Coast (March) were sieged.

I am not sure what is going through most investor minds right now but I am increasingly advocating an asset-light model for myself.

Asset-light is the new catchphrase for me in the same spirit of Singapore’s own MRT as recently announced. By that I am inclined to avoid being tied-down by fixed investments such as real estate and overly beholden to leverage. Asset-light to enjoy freedom of flight as Americans explore emigration to Canada and British hunt for Irish passports even as Singapore has always been inundated by peace-loving and financially independent immigrants looking for a new home.

Some Radical Hedges

And the potential hedges for the past weeks of violence and the up-coming weeks of potential violence when Trump and Hillary start their ugly campaigning in earnest?

I can think of 2 overlooked sectors—defence and private security companies.

While defence companies have their share of popular ETFs out there, led by ITA US, PPA US and XAR US, private security companies are few and far between, mostly privately owned due to the nature of their business which is “private” and thus could not stand to public scrutiny as we find only a handful of listed firms

The best example would be G4S, the largest private “army” in the world with 618,000 employees on their payroll, a global operator in 125 countries. Rocked by scandals, with the most recent bad press coming from the Orlando shootings where it has unfolded that the gunman was a former employee.

G4S Plc operates as a global integrated security company. The Company offers a range of services, including the supply of security personnel, monitoring equipment, response units and secure prisoner transportation. G4S also works with governments overseas to deliver security.

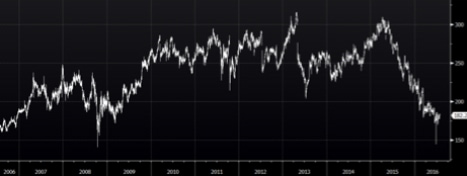

Listed on the London Stock Exchange as GFS LN, its stock price has tumbled in past years to its lowest since the financial crisis.

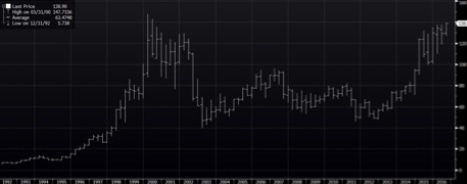

Not so unlucky would be the other publicly listed security firms, that do not engage so much in direct confrontation such as Securitas AB, listed in Stockholm as SECUB SS whose stock is trading at its highest since 2000.

Securitas AB’s services include guards and patrols, investigations, home alarm systems, loss prevention, security consulting and guard dog supply. To facilitate its cash in transit service, Securitas AB operates specialist vehicles with metal safes as well as a fleet of bulletproof jeeps. It also specialises in securing sporting, business and recreational events operating in Europe, North and South America, the Middle East, and Asia.

Spanish company Prosegur, PSG SM, operating largely in Europe, the popular destination of ME refugees, is seeing a historic high for its stock price.

We can naturally expect any companies associated with the US National Security Agency to prosper, the surveillance companies, cybersecurity companies, big data companies and more.

The top 3 Aerospace and Defence ETFS—iShares US Aerospace & Defence ETF (ITA US US$128.28, +8.5% ytd), Powershares Aerospace & Defence Portfolio ETF (PPA US US$ 38.35, +7.6%) and SPDR S&P Aerospace & Defence ETF (XAR US US$ 57.57, +8.85%), have outperformed the S&P 500 year to date and look set to be portfolio staples going ahead.

It is much harder to throw it in with the defence companies of Asia much as punters like AviChina (2357 HK) whenever some ship sails too close to disputed islands. Singapore has her own ST Engineering (STE SP) and some newly listed Secura Group.

A Final Word

Global geopolitical tensions are unlikely to ease with little middle ground in sight and the world shall suffer a loss of global leadership into the coming US Presidential elections with potentially more uncertainty after. In the extreme case where the US loses its “street cred” and global influence, imagine how many more souls would be swayed to radical thoughts when hope is lost? Imagine the fall out if Trump declares Saudi Arabia a public enemy? Imagine the global fund flows when that happens?

Such are times to imagine an SMRT asset-light model for ourselves.