Nobody is Going to Actually Notice if Sibor is Higher

Happy Versus Unhappy People

World happiness levels are at a 10 year low, according to a Gallup survey, as US stock markets powered to a record high on this Autumn Equinox.

Yes, we feel it as fatigue drained us this week in the markets which have been obedient and true to US President Trump’s agenda which is the simple mantra, stock market = economic health, notwithstanding the US dollar or rising bond yields, nor trade wars, Brexit, emerging market woes, nor disturbing economic forecasts that mention the R-for-recession word too many times for our comfort in this week.

After Trump’s tweet grumbling about high oil prices, accompanied with threats, we would expect him to have something to say when US bond yields broke new highs but we guess that would have to wait especially after he finds out this weekend that Saudi Arabia is following in China’s stead in purchasing Russian weaponry and India will be buying sanctioned-Iran’s oil with rupees.

The only happy guy we would claim to know would be the fellow who is a friend of a friend’s church mate, who had sold off his nice house and possessions, and bought himself a little flat (that is probably not a store of value) and sleep with his bank passbook under his pillow. He supposedly takes out that little passbook once in the morning and again before he sleeps each night, presumably fitfully, feeling happy knowing that the number will not be going away tomorrow.

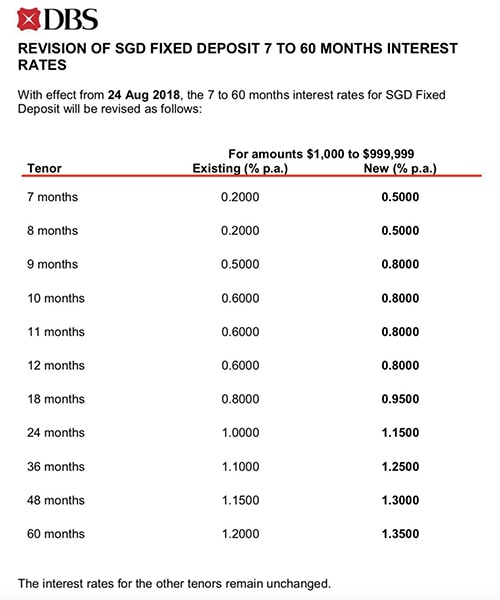

He would be even happier to know DBS has hiked their fixed deposit rates again last month with the 18 month fixed deposit now at 0.95% from 0.6% when we started the year.

Source: Mortgagewise.sg

Source: Mortgagewise.sg

Nobody is Going to Actually Notice…

This brings us to our point today, after we were asked by a good friend how would we feel if 2% SGD funding (as in 1 month Sibor) became reality?

It never crossed our minds, really, as we laugh and joke about Argentina (at 60%), Turkey (at 24%) and Russia who was forced to act last week. Singapore’s Asian neighbours have been at work in August, with India, Indonesia and Philippines raising interest rates but we did not think it would matter much or significantly affect us.

After all, as US Commerce Secretary, Wilbur Ross, said about tariffs, “nobody is going to actually notice it at the end of the day”.

He could have been talking about us this year.

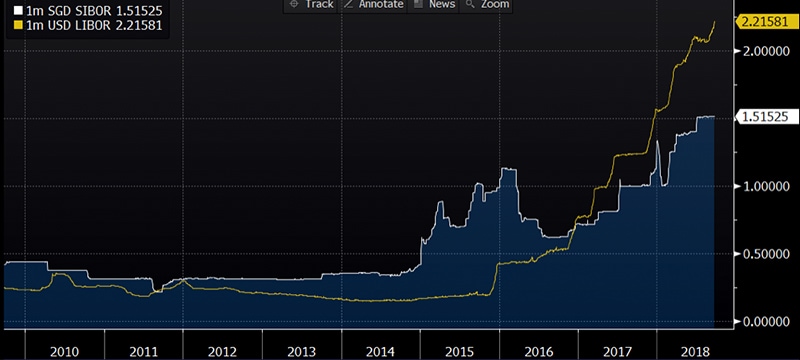

We had 1% Sibor last July when we wrote, Welcome, 1% SIBOR: It is for real this time, and 14 months later, it is just at 1.51525%.

Better still, the gap between 1M Sibor and 1M Libor made a new 9 year high on Friday.

Chart of 1M Sibor vs 1M Libor 2009-2018

Chart of 1M Sibor vs 1M Libor 2009-2018

For all the noise out there, we did not feel a thing here or even the fact that Sibor’s (1 month to 12 months) across the curve are at their 9 to 10-year highs.

It is rather simple arithmetic, 1.51525–1%=0.51525% which is just S$5,152.5 per annum (on a million dollar loan), hardly a dent (4.75%) in the median household income of S$ 108k a year.

Give us 2% and maybe some folks will start making some noise but meanwhile, show-flats are still packed and the property sector remains robust because we have nothing but optimism in every single report we read from The Edge and Property Guru to the Straits Times and no self-respecting licensed media outlet would have anything bad to say because mortgage rates and property prices are just not correlated.

Moving over to Hong Kong, the Hongkies have it tougher, as we read about home sellers cutting their property prices as interest rate increase looms some selling for as much as 18% below bank valuations.

Source: SCMP

Source: SCMP

We would say that it is their own doing because 1M Hibor has risen sharply by 1.35% in the past 12 months, from 0.54% to 1.89%, in contrast to Singapore’s milder ascent. Surely it cannot “loom” higher from here?

1.35% would be $13,500 on a million dollar loan and that would be much more unpalatable as a 12.5% of additional expense on Singapore’s median household income although experts have informed that it would never happen in Singapore because they are sure that rates will hold steady because we are about to head into October’s MAS meeting which will decide on the direction of the Singapore dollar (for we have no interest rate policy) and strengthening the Singapore dollar would give our interest rates room to head lower.

Some quick math on a hypothetical 1 million dollar loan on a 3% rental yield 1.5 million dollar investment property would mean that rentals would have to rise well over 60% to cover the interest rise from 0.54% to 1.89% in order to maintain the 3% yield. How inflationary would that be?

Some quick math on a hypothetical 1 million dollar loan on a 3% rental yield 1.5 million dollar investment property would mean that rentals would have to rise well over 60% to cover the interest rise from 0.54% to 1.89% in order to maintain the 3% yield.

In Singapore’s case, rentals will have to rise by just 20% to make up the same yield for the higher Sibor.

It is definitely not as inflationary.

Are we missing a point here or perhaps the math is slightly flawed?

Nobody is Going to Actually Notice… The Boiling Frog

For our part, we do not have anything pessimistic to say about Singapore but we are not sure if Singapore can withstand the global headwinds of higher interest rates. Yet we think no one is going to make the connection to Goldman Sach’s analogy of the boiling frog, in their report this week, which has nothing to do with our real estate rental returns.

Source: Bloomberg

Source: Bloomberg

The link or connection is in the boiling frog—a fable that a frog in tepid water would not notice itself being cooked to death if the water comes to boil slowly.

Source: Wikipedia

Source: Wikipedia

Us and our nonchalance over Sibor at its 9-10 year highs, unperturbed as Hong Kong investors are feeling the heat, much the same attitude we have on our passive investments which is the correct attitude because it does not pay to panic and we all want to be like Warren Buffet who famously said that no one likes to get rich slow.

Bring on the 2% Sibor and we may start to see some folks jump bail and opportunities arise across the asset classes although Sibor is not for any central bank in the entire world to control, rising when the rate-setting banks increase the rate without direct guidance from any authority.

The Federal Reserve will meet next week to hike interest rates for the 3rd time this year, as markets have more than 100% priced in. The expectation is a 60-70% chance of a hike in December to make that 1% increase in 2018.

Until then, we can widely expect higher Sibor rates in the days ahead, that is, if anybody actually notices.