Real Estate: Sovereign Wealth Funds To The Rescue?

When news broke that the Norges Bank was considering the joint purchase of Asia Square Tower 1 with Capitaland, it was seen as a big winner for Singapore real estate at its record breaking S$3.5 billion valuation against an asking price of S$ 4 billion which would surpass the previous record of US$ 2.5 billion set in 2011 when Keppel Land sold its controlling stake in Ocean Financial Centre to K-Reit. Not only would it have made a record transaction in price terms, but it would have been the first investment Norges has made in real estate outside of Europe and the US, elevating Singapore’s prime status to the ranks of Manhattan and London.

Alas, negotiations fell through earlier this month, with no comment from parties involved.

Norges Bank has been in Singapore since 2010 when they set up an investment management arm in the city state and they have been keeping busy buying regional equity and bonds, deploying their US$ 825 billion around the world – US$ 2.9 bio invested in 126 local Singaporean listed stocks.

Sovereign wealth funds are growing as their investment returns amplify and they are more than a force to reckon with in markets if we are not careful enough to spot their wall of cash coming, we could be missing out on something big. Just look at how they have grown in 2 years.

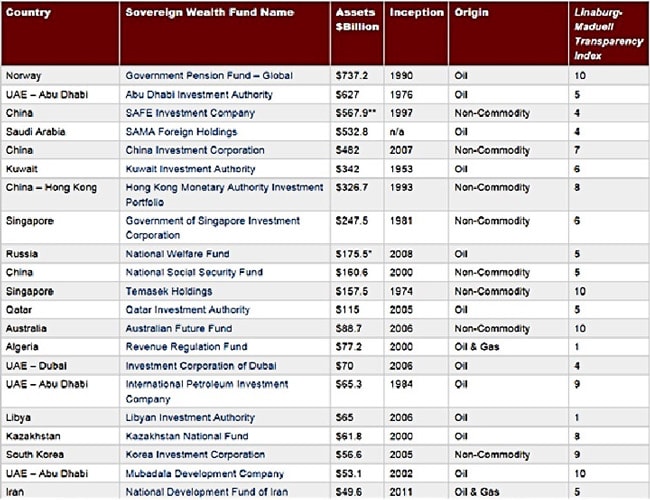

Back in 2013.

And now the latest numbers as of end 2014.

The wall of cash is growing and the deployment gets trickier as the world runs out of safe assets to buy and bond market liquidity becomes a hindrance for the US$ 8-9 trillion held by sovereign wealth funds around the world.

It would be easy if Norges could just buy up Apple Inc for US$ 600 billion with their US$ 825 billion and use the rest of it to buy either Disney, Alibaba or Walmart and we can have Temasek buying up Nestle, etc.

But SWFs have come to realise that some trades are hard to exit when there is no one of their size and calibre to sell out to and Norges has recently decided that bonds are not best place to be in, without pressing any panic buttons, by a politically correct announcement in August that “The fund is gradually increasing real estate investments to as much as 5 percent of its assets through a corresponding decrease in its bond holdings. The move spreads the fund’s risk across more markets and can also protect against inflation as rents are often linked to price indices.”

With real estate only taking up 2.2% of their entire portfolio as at end 2014, there is a lot of room to grow and they have been on a buying spree this year with their most recent purchase last week, paying US$ 1.56 billion for a 44% stake in Manhattan office buildings, in a joint venture with Trinity Wall Street, the Episcopal church owner of the properties.

Norges is now considering if adding real estate will improve the risk-return profile of their mixed asset portfolio and Asia has much reason to cheer, without any representation in the Norges pot, as yet, as all purchases have been restricted to 6 main cities around the world namely, New York, Washington DC, Boston, San Francisco, London and Paris, along with a sprinkling of minor investments in smaller European centres.

Singapore and Tokyo are the first obvious targets in Asia for the sovereign wealth fund that stresses on responsible investment “thorough due diligence of the parties involved in the transaction and the property itself, spanning financial, legal, tax, structural, operational, technical and insurance matters. Environmental factors are also part of this review, and measures to improve energy and water efficiency and waste management“.

And thus the strategy of investing with partners that have good knowledge of specific markets, not taking entire stakes but joint shareholding which made the Asia Square deal a prime choice given that the building is one of the “greenest”, environmentally sustainable building in Asia, complete with largest photovoltaic cell (solar panel) installation on the roof in Singapore and the first bio-diesel generation plant in a commercial development in the CBD (source: Wikipedia).

More of The Same?

Real estate investment by sovereign wealth funds is not a new development and Singapore’s GIC claims 30 years of real estate experience with their “350 real estate investments in more than 40 countries. Its prominent buys include an undisclosed stake in New York’s Time Warner Centre and 50 per cent of the Broadgate Circle in London’s financial district… As at March 31, GIC had 7 per cent of its assets parked in real estate and 9 per cent in private equity.”

With Norges Bank joining the fray, to invest about US$ 5.8 billion annually into property in 10-15 cities globally, we can expect more of the same from the rest of the field who have already started their hunt as we saw the Abu Dhabi Investment Authority pay US$ 1.2 billion for a stake in 3 Hong Kong hotels earlier this year as funds, sovereign wealth funds and their peers sweep in on London docklands and downtown Manhattan.

Bad for Bonds

The immediate casualty from the investment angle would be the bond market.

Property rentals are substitute for fixed income returns whilst adjusted/hedged for inflation as rentals rise with inflation, assuming a long run supply-demand equilibrium. That said, this paradigm should be reserved for the ultra long term investor, the Temasek’s of the world, with their 30 year investment horizon.

Without the extra demand from SWFs to feed the growing bond markets, we are left with only pension funds and central banks to plug the gap for the US$ 2 trillion corporate bonds per annum we have been seeing since 2012. And we have retail participation, of course, even as liquidity dries up.

Glimmer of Hope or a 2 Tiered Marketplace?

Promising as the SWF Walls-of-Cash may be for real estate, the ugly truth is that the beneficiaries are few and far between as few of us can rush out tomorrow to buy or build another Asia Square to entice Abu Dhabi or Norway to look at.

The investment trend suggests that partnerships are preferred for strategic and iconic assets with environmental, social and political considerations, thus we can forget about selling our spare condos tomorrow at this rate.

Size does matter, as well, along with asset portfolios and thus Blackstone may find a more willing buyer for their US$ 861 million Devonshire Square than someone with a S$ 1 million commercial unit in Paya Lebar.

For the sad facts have been summed up by Bloomberg as these.

- For every job created in the U.S. this decade, companies spent $296,000 buying back their stocks, according to the New York-based bank.

- An investment of $100 in a portfolio of stocks and bonds since the Federal Reserve began quantitative easing would now be worth $205. Over the same time, a wage of $100 has risen to just $114.

- For every $100 U.S. venture capital and private equity funds raised at the start of 2010, they are now raising $275, but for every $100 of U.S. mortgage credit extended five years ago, just $61 was extended and accepted this June, BofA said.

- Prime commercial real estates gained 168 percent, compared to a 16 percent increase of all U.S. residential property. In the U.K., London accounted for 26 percent of the value of all housing sales last year even though it accounts for just 1 percent of the land.

Ownership levels is lowest in the US since 1967 so we can be sure building complexes are even more out of reach than ever as credit availability is increasingly.

The hope lies in the partners that will be picked for partnership, such as Capitaland, the likes of Hilton and property managers with the experience to impress the Walls-of-Cash.

This should drive strategic Reits into play. Proper Reits with strategic assets bearing value and not those motley assemblages of little warehouses and rural buildings.

And the biggest hope of all – Time, the 30 year time frame and the SWF pockets that only allocate 5-10% into real estate.

Meanwhile, for all those property owners looking for tenants to fill their vacant units or bond holders wondering where all the bids have gone? Maybe its time to pool together and buy a smart building instead?