SG50 Special: Singapore Takes On ETFs, For Better Or Worse?

Sometime in March, the MAS announced three broad initiatives for individual investors.

The new rule is that SGX ETFs that make limited use of derivatives can be traded by the public.

Where were ETFs before this?

Out of reach since 2012, except for 8 then, because retail investors had to take an SGX financial literacy test before being allowed to trade most of the 96 listed ETFs in the Singapore Stock Exchange, that is unless they are accredited or expert investors, or if they possess the right education or work or investment experience.

Under the new scheme, ETFs that pass the mark will be reclassified as EIPs (Excluded Investment Products) which means the public will grow to love ETFs as the world has come to. And as we continue to get positive press reports like this one below, the number of ETFs permitted for public trading has risen to about 19 as the SGX comes out to waive ETF clearing fees for both institutional and retail investors between June 1 and Dec 31, 2015 and fees on block trades till end 2017.

A Bit About ETFs, ETNs and Index Funds

There are mutual funds and indexed mutual funds which have to be bought over the counter from the fund company. Over the years, indexed funds have been found to outperform the actively managed mutual fund. Yet this has also proven to be a hassle because price discovery is difficult and for most of the time, one will not know the transacted price until after the deal is done.

In comes the convenience of the ETF, an offspring of the indexed fund, which is traded over the stock exchange and that is the fastest growing segment of the stock markets today with US$368 bio of new funds flowing into ETFs versus global new IPOs of US$286 bio in the past 12 months.

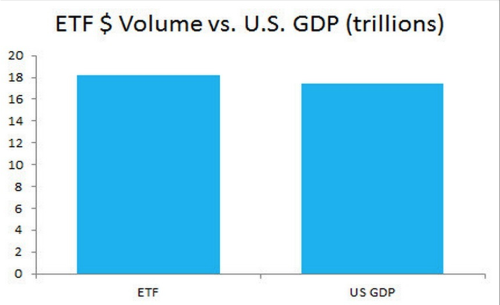

ETFs have over taken hedge funds in terms of total assets and ETF trading volumes in the US alone for the past year have over shadowed the size of the US economy.

What about the ETNs?

That is another similarly indexed linked product that is in the form of a note i.e. a security issued by a bank and also listed on the stock exchange for trading.

The main difference is for the ETF, you are investing into a fund but for the ETN, you are placing your money with a bank and thus taking the bank’s risk.

Yet there are upsides to it, because the ETN is supposed to less tracking errors, which we will come to find may not be theoretically true, and there are tax advantages to them for investors in certain jurisdictions.

There are currently nearly 5,000 ETNs in the world now and about 50% more for ETFs and we note that statistics do not group them together which means this entire idea of Exchange Traded Products has reach a new high globally with many good years left in store.

Why ETF or Why Not?

From the Bloomberg article from above, we note that one-third of the trading volume comes from the SPY US ETF (S&P 500), with US$ 6 trillion in turnover per annum even when their total AUM is only US$ 177 bio and the top 4 ETFs combined account for 45% of total turnover.

I would suppose that a high turnover is good because it means that the market is efficient and thus the SPY’s tracking error is just 0.321 or 0.05% off the actual S&P 500 which is less than their expense ratio of 0.095%.

It is not always the case, as a reader pointed out to me, that his VXX US (Barclays iPath S&P 500 VIX Short Term Futures ETN) never saw the short terms profits of the VIX Index made and resulted in a loss for him just last month when the underlying VIX Index outperformed the ETN with a weak 50% correlation. It is no wonder that the market cap of this particular ETN has dwindled to US$ 940 mio from a high of US$ 6 bio some years back.

This tracking error is exacerbated when the underlying comprises of illiquid instruments or when the ETF, itself, is illiquid like the GLD SP ETF (SPDR Gold Shares SGD) which consistently underperforms its USD denominated counterpart, the GLD US ETF (SPDR Gold Shares US). The USD GLD ETF actually outperformed the gold fixing by 1.3% year to date while the SGD version of the same instrument underperformed by 1.27%.

Other reasons for ETF tracking errors – leverage, rebalancing costs, dividend reinvestments, index changes.

So far, few have dared to bring up the dreaded topic of liquidity which is brings me to my main point today.

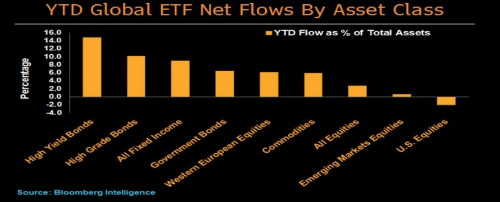

For instance, we know that liquidity in the bond markets have never been worse and for that reason, there has been unprecedented demand for bond ETFs.

Is it really more liquid when you buy an ETF?

Carl Icahn echoed this last month at the high yield debt market, taking a swipe at Blackrock, the largest ETF manager in the world with over US$ 800 bio of AUM.

“They sell liquidity. There is no liquidity. That’s what’s going to blow this up.”

And it is not just the bond market because there will be secondary effects when ETF managers are unable to unwind, they end up hitting other products which has a domino effect as I noted last year that the Russell 2000 mid cap index was sold off to hedge the HYG, the iShares iBoxx USD High Yield Corporate Bond ETF.

US Congressman Hensarling has accused the Volcker Rule to have “caused a massive drop in corporate bond inventories” as bond traders are vanishing from the marketplace which is the reason for the illiquidity.

And when there is no liquidity, the obvious consequence is that funds can plunge “way below the value of their underlying assets, with the biggest discounts since the U.S. financial crisis” with “traders are taking a 15 percent discount to sell shares of the $1.3 billion BlackRock Corporate High Yield Fund relative to its assets’ value, and an almost 11 percent haircut on John Hancock Preferred Income Fund II shares” which is what is happening now in the closed-end debt funds in the US. This is a cause for concern if it spreads to the larger world of ETFs.

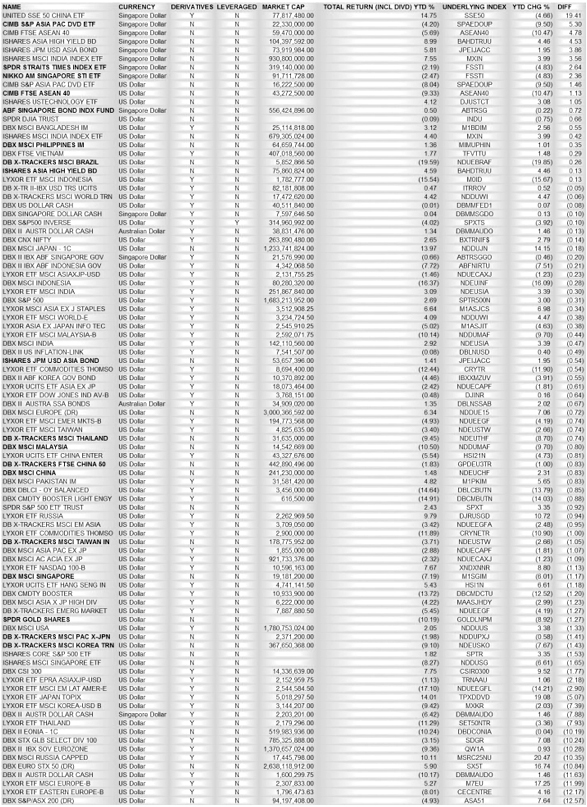

At least the ETF world has a name for it – tracking error and let us examine how it looks for the 92 ETFs available on the SGX.

Ranked in order of outperforming their underlying indices and highlighting in Bold those which qualify as EIPs (information unverified from hardwarezone forum because SGX does not have a list on their website).

MAS is right – most of the derivative ones do worse and should, thus, be kept away from the retail investor. The smaller market caps ones, especially! Yet how is it possible to block trade when 40% of these ETFs have market caps of less than 10 mio?

The positive is that errors can also work in your favour, if you know how to capitalise on it.

And looking at the big winner, the derivative based (futures driven) United SSE A50 China ETF (+19.4% vs index ytd), shows how Singapore could give the HSI a run for their money with their underperforming US$ 5.93 bio 2823 HK ETF (-3.8% vs index ytd and -25% vs index in 12 mths) and US$ 7.25 bio 2828 HK ETF ( -0.5% vs index ytd and -0.48% vs index in 12 mths)!

Happy SG50!