Welcome, 1% SIBOR: It is for real this time

It is Oxley on our minds this week when you can have the free papers devoting 10 pages to the Oxley saga that I am ashamed to admit I have little idea as to what the case is about except that half of LKY’s family wants to preserve his old home while the other half wants it demolished and half of them happen to be the head of our state which means that the government is now involved.

Do not correct me if I am wrong because it is not my duty as a citizen to worry about a house that happens to be previously occupied by the founding father of Singapore or demand that every stone or tree he has touched to be sacred because there are so many other things left to preserve his memory and his national legacy, of course.

At this rate, we are better off worrying about some of his final words as was published in one of his final books, One Man’s View of the World.

“Will Singapore be around in 100 years? I am not so sure. America, China, Britain, Australia—these countries will be around in 100 years. But Singapore was never a nation until recently.”

Preparing for Life Above 1% SIBOR

There is something else brewing onshore that has got some of us worried even though we have lived through weirder times in the local markets, such as the mind-blowing episode of negative SOR rates in 2011. It left us scratching our heads long after it quickly blew over with all the rapid first aid measures by the authorities, leaving us licking wounds and feeling sore despite the witch hunt that followed to nab the errant bankers and fines on their institutions.

Things are supposed to be better now with stability that we can safely take for granted again as our faithful authorities brushed up their act, overhauling our financial markets that we might forget. Banks took the opportunity then to shift most of the loan portfolios to SIBOR after the close shave that saw some customers pay no interest for those loans with zero base rates, hardly fair to them for they should have been paid to borrow with those negative fixings.

This week ended 7 July 2017, we saw the largest positive 1-week change in 1M SIBOR since Jan 2015, rising some 0.11% to close at 0.93047%, well above its 10 year average of 0.64%. For that matter, 1M SOR saw its largest 1-week increase since 2015 as well, rising some 0.32% to close above 1%.

It means little to those home loans, to be honest. 0.11% is just $1.1k per annum on a $1 mio dollar mortgage. Yet, if that were to be a trend, the consequences would be slightly more dire although we are safely not anywhere near the highs of SIBOR, last seen early last year.

Nonetheless what got us worried is that we have not had a situation where the market would be tested with a 6 year high in unemployment, tepid growth and higher interest rates before.

Graph of 1M SIBOR, 1M SOR and Unemployment Rate

No, we are not here to spread fake news or sound alarm bells but just to spread awareness that bond prices are not doing too well at the moment which is probably nothing to worry about even if global 10Y bond prices are down nearly 3% in the past month, with German bunds prices hovering near their 18 month lows.

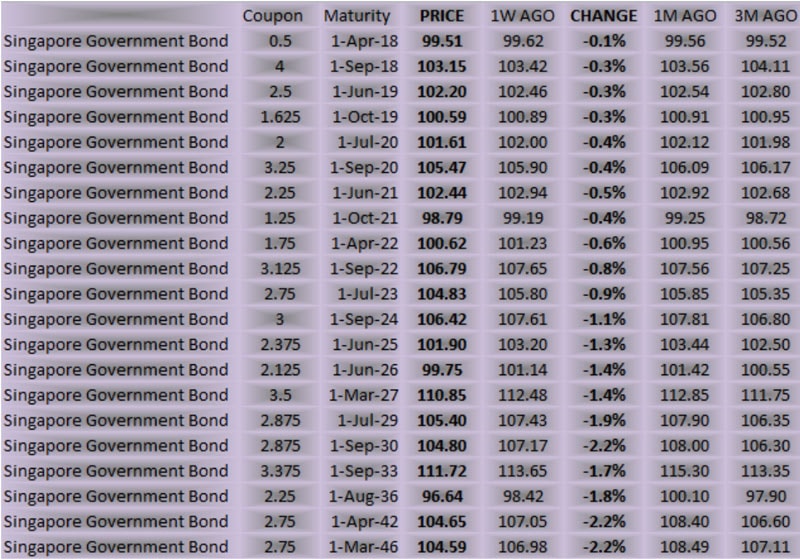

Table of Singapore Government Bond Price Change

Singapore government bond prices are down between 0.1 to 2.2% for this week unbeknownst to many a retail investor as their bankers and the media continue to report on happy times for bonds.

Source: Sunday Times

We Don’t Know Why SIBOR is Higher, But It Is

We cannot be too sure about why SIBOR is rising and if it is on a rising trend simply because Singapore does not have an interest rate policy.

SIBOR is set by banks on a daily basis based on the transactions between themselves although we cannot be too sure how much really goes through between banks beyond the tenor of a month as we have been informed by industry insiders who claim that the new regulations make it hard for outright interbank lending in the longer tenors.

SOR, or the swap offered rate that is derived from the USDSGD forward points, is transacted daily and expressed in our IRS, interest rate derivatives, curve as a means for which the longer dated rates to be derived from.

We cannot say that SIBOR is set on a whim more than demand and supply for money, there was once a correlation between LIBOR and SIBOR and SOR. A correlation that has broken down several years ago led by several factors.

1. USDSGD is a non-international currency and thus, foreigners cannot borrow more than 5 mio SGD at a time. This only allowed inflows i.e. foreigners to lend SGD to the onshore market.

2. This worked well during the times when Singapore’s foreign exchange policy suited them because rising inflation meant the authorities had to keep the SGD dollar on a strengthening trend.

3. As it is, the SGD dollar is the 3rd best-performing currency in the world for the past 10 years even if its appreciation trend ended in mid 2010.

4. When the SGD dollar was on a strengthening trend, it did not matter if the fwd points derived SOR diverged from the SIBOR because the cost was immaterial to the currency gains.

5. Banks were unable to arbitrage the difference between the SOR and SIBOR because local banks were long SGD and did not need the cheap SGD funds which meant foreign banks had no one to lend the money to except to themselves.

6. The demand for USD for assets and speculation grew instead which led to the dramatic collapse in SOR in 2011 led by several factors resulting in several offshore players leaving the market.

The above is written for posterity and unimportant for the issue at hand.

What should be important is that the correlation between SIBOR, SOR and LIBOR has been reestablished for some unknown reason, noting that 1M Libor has been stealthily exceeding 1M SIBOR since late 2016, for the first time in 8 years.

Chart of 1M Libor vs Sibor vs SOR since 2010

It is for real this time, unlike the “scares” and “taper bluffs” we had in the past 2 years that we were unduly worried about when the rest of the world was still in zero rate mode.

The ECB, FED, Riksbank and gang are all in the same boat and acting in unison for a global trend.

Source: CNBC

It is For Real This Time

It is nobody’s fault if the prices of newly issued bonds like FH Reit, issued 2 weeks ago, do not budge in the face of higher interest rates although cracks are starting to appear if anyone has the sense to ask for a bid price for their newly acquired Sembcorp 3.7% perpetual.

In this new world of low volatility, we are right to be none too worried even if the High Yield Corporate Bond ETF has broken below its 100-day moving average.

iShares iBoxx $ High Yield Corporate Bond ETF

It’s Asian counterpart, the USD Asia High Yield Bond ETF, on the other hand, appears to be on a more certain downtrend, trading near its lows for 2017, as Bloomberg reports the first outflow for Emerging Market bonds for the year and since the US presidential elections last year even if it is a mere 2% of AUM, after attracting 30% of AUM inflows in 2017.

iShares Barclays USD Asia High Yield Bond Index ETF is an exchange-traded fund incorporated in Singapore.

Yet these 0.25% rate hikes by the Fed and the SIBOR catching up will undoubtedly eat into those leveraged positions for those investors buying their bonds on margin. Imagine borrowing 60% to buy a bond, returns would be negatively impacted by 0.42% for every 0.25% increase in the borrowing cost, amplified by the leverage.

This applies to all borrowings that are sensitive to higher interest rates unless one had the sense to lock in the cost at a fixed rate which means… we should give every fixed rate bond issuer this year a big pat on the back! Well done for mitigating the risks and passing the buck to the investors.

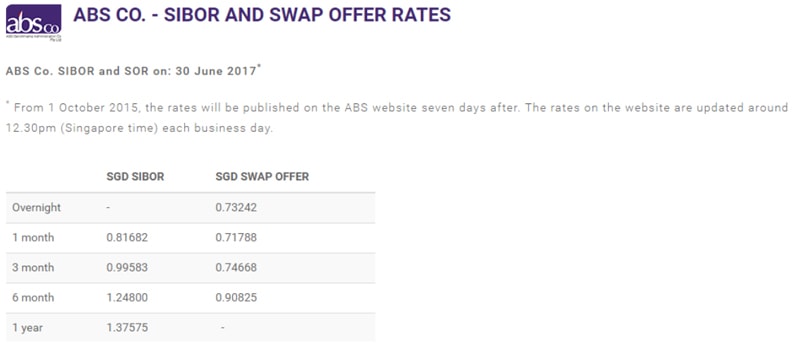

Bond prices cannot be immune to an environment of higher interest rates. However, the retail market sometimes takes a little longer to realise that interest rates have risen which is a shame now that they have to pay for such information as the Association of Banks delays their SIBOR and SOR data to the non-paying public.

Source: ABF website

At the same time, we have to take a pause to consider if all this will work out to be disinflationary for Singapore in the long run which gives the authorities some room to keep their exchange policy easy. So far, we are seeing no signs of that the SGD dollar holds strong at 6-month highs against the USD.

Meanwhile, we know those bond returns are only going to shrink. The same goes for stock and real estate returns. It is just too bad if folks don’t know it’s probably for real, this time.