What Are Central Banks Not Telling Us?

After 18 years in the markets and a few crises along the way, one comes to realise some hard truths about markets and central banks, and that they are held hostages by their respective agendas. Markets are simple, just mechanisms that operate solely on human greed and central banks or regulators are bound to keep market order.

Such is the commitment of the central banks that since 2009, the Fed started to use forward guidance as a policy tool, to forewarn markets of their intentions months before acting, giving the markets ample time to “price-in” the moves.

This is because central banks all have one thing in common, they are compelled to naturally assume the role of the ultimate economic cheerleader and cannot be seen to disrupt order or risk an Armageddon of sorts in a loss of confidence for them to admit that their policies are inefficient which, besides puts their careers and personal credibility in jeopardy, would end in political repercussions that carry consequences quite unimaginable.

The FOMC decision not to hike the lowest interest rates in history after 75 months of economic growth, after the worst recession since World War II, has been hailed by the media as the right decision even though expectations were running high for a rate hike after their last meeting in July, the expectations fizzled into September when the S&P 500 saw their worst monthly return since May 2012 and the worst August return since 1998, I believe.

Admitting this time that it was due to China and other global pressures, however, when things are looking quite rosy in the US is akin to ceding their economic supremacy to global forces i.e. China. They tried to pass off housing and other concerns but as we can see from economic data, the main negatives are coming from the business cycle.

To me, they are not telling us something.

Major central banks around the world keep harping on how things need to get better but global GDP has not stopped growing since 2009.

World Bank Global GDP Notional USD Billions

Inflation is off 2009 lows albeit that it is slowing and global unemployment has not been lower since 2008.

Bloomberg World Unemployment Rate %

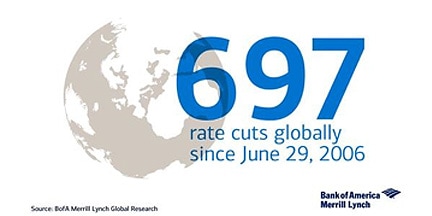

There has been nearly 697 global rate cuts since the last Fed hike back in 2006, according to BofA and stock markets have performed admirably in the past 6 years.

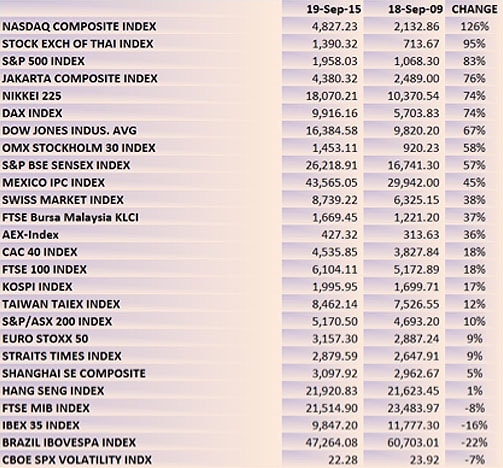

6 Year Change in Stock Indices

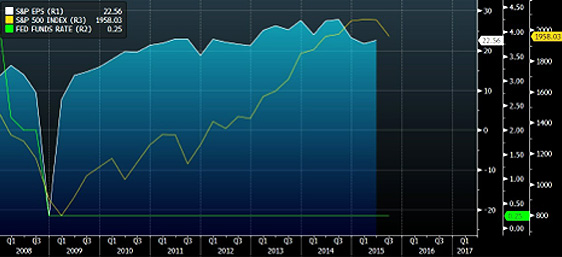

Nearly 14 trillion in QE assets held by major central banks that have pumped nearly US$ 10 trillion in QE monies while keeping a ZIRP (zero interest rate policy) and corporate income has stopped growing for the S&P 500.

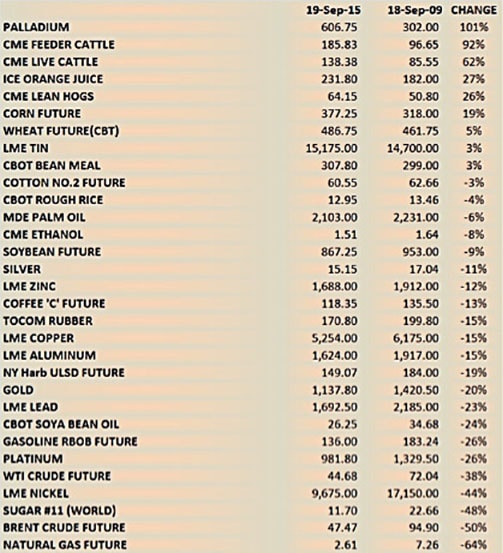

Commodity prices, particularly industrial commodities such as oil and basic metals, which used to buffer and make up for the inefficiencies of the former global growth engines, the emerging market economies, have deflated leaving these budding economies with little prospects, riddled as they were over the years from the effects of corruption and exploitative governments.

The only short term weapon central bankers have left in their pockets which is currency war where weakening the currency is an almost immediate boost to GDP (in local dollars), all things status quo unless other central banks do the same. That happened earlier this year when the Swiss National Bank, certainly almost because they were fed up of the ECB, decided to unpeg their currency from the EUR before the ECB started their Q€ program.

Yet a currency war is the last thing a central banker would want to be remembered for, because devaluation undermines the currency’s sovereignty that leads to the inevitable capital flight that many a central bank can ill afford unless they happen to be the Big 4 or 5 (USD, EUR, JPY, GBP, CNY). Incidentally, that is why no respectable central banker will be seen as a gold supporter.

What Is Happening?

For one thing, I have been writing about this secular stagnation story for the past 2 years and the fact is that we are not going to escape this one without any bloodletting as Moody’s expects default rates to rise which has not happened yet.

For another, it is clear that we are living in unprecedented times and no economic textbook has the answer to what will happen when interest rates are raised from zero which is potential for a minsky moment that we have spoken about.

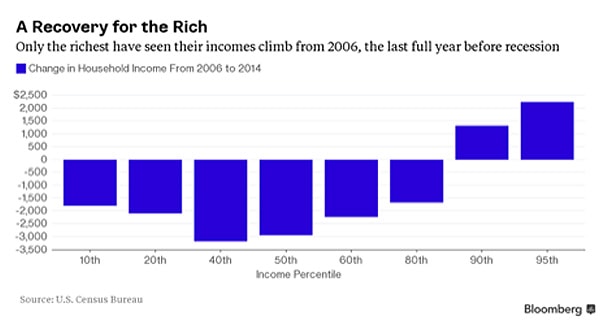

Commonsense tells us that interest rates are a blunt tool, at best. For, does anyone really think that interest rates can directly affect employment ? Yet that is all the US has relied upon in the past 6 years to reduce unemployment. And if that is the case, surely there will be some ill effects? The Fed has admitted that QE is the cause of the widening income gap.

Source: Bloomberg

Markets while functioning on the basic precept of greed know Rule no. 1 that central banks or regulators are bound to keep market order which makes it easy to corner those central bankers in their “forward guidance” game unlike China’s PBOC and Switzerland’s SNB which made no such commitment to the markets and is free do as they please.

Free Markets? No More?

I never thought I would say this but the Chinese model is starting to work because total control looks like the best way to keep Markets/Greed in check which is something that does not happen for free markets elsewhere.

Anyone who thought we had free markets after the Great Recession would be deluded to think so with the plethora of rules and regulations to ensure market order.

But rules and regulations are just new obstacles for Markets/Greed to find a way to skirt.

What Are They Not Telling Us?

Perhaps the only honest person is Bernanke who has since left the Fed’s service and is open enough to admit that there is no escaping this low rate regime for his lifetime.

Central banks have run out of ammunition ! At near zero rates, there are no more fats to cut and another QE would be as effective as a mosquito against the elephant in the room. There is no more room for failure!

In the absence of any new growth engine to take the place of China which has grandly assumed the role for the past 2 decades, while looking to India and Indonesia as pale comparisons, the world has run out of steam as technological advances continue to keep inflation in-check in manufacturing, services and agriculture space.

The Bloodletting Conclusion

Economic booms must be accompanied by economic busts. That is the key characteristic of the capitalist model.

What central banks cannot tell us is to expect an economic bust/downturn which is expected by some economic models to be end 2017. Imagine the social and market panic ?

Some long term economic cycle models such as the K-wave points to the dawning of a new 20-year age for a post IT cycle that has lasted from the mid 80’s to now. New themes as resource efficiency and robotics/artificial intelligence have been suggested which does not bode well for employment, in my opinion.

As a friend neatly summarised last week:

- Who believes the official unemployment numbers?

- Who believes the official inflation rate?

- Who believes that a group of very intelligent individuals uses the above to determine short term interest rates?

What they are not telling us (and cannot tell us) is just perhaps that they just do not know what they are doing and there is no more margin for error.