Imaginations Running Wild Part 2: SIBOR, SOR or A New Benchmark?

– Singapore’s en bloc fever rages even as China’s President Xi says Housing Should be for Living in, Not for Speculation. Perhaps Singapore could represent currency stability or gains?

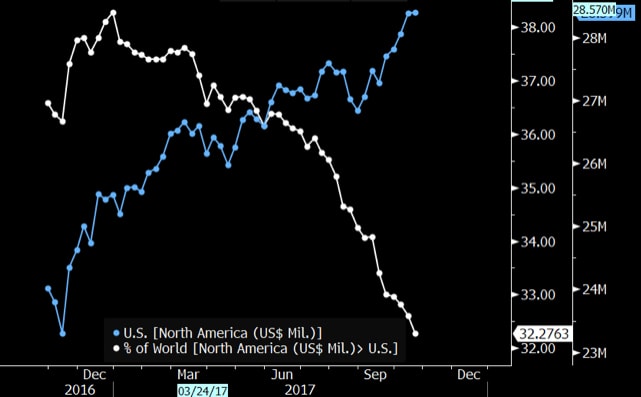

– The US share of total global market cap has plunged even as it added $5 trillion to its markets

– Meanwhile, the US has the 6th largest budget deficit on record for 2017, at $666 bio as we wonder if Nasdaq will get to 6666 before Bitcoin does

– With overnight money rates rising to a 9 year high in Singapore this week, it is a good time to talk about the future of Sibor as Libor will be phased out by 2021

– Libor has lost its credibility with too few transactions to be meaningful thus the urgent need for a replacement given that hundreds of trillions’ worth of loans and derivatives are tied to it

– The General Collateral Financing Repo rate has been picked to replace Libor which makes sense, given that both rates are based off the Fed Funds Rate

– It is complicated in Singapore because Sibor is not covered by Singapore’s version of monetary-without-interest-rate policy

– Currently, the Singapore government t-bills are paying a higher rate than Sibor which is an anomaly

– The SOR trades even lower than Sibor which makes it cheap for offshore folks with access to USD to swap their USD into SGD to lock in profits on those bills, making more money than locals who borrow in Sibor

– Yet Sibor does not trade much and is probably based on “expert opinions” much like Libor these days

– While there is a flaw in that, there is less at stake because unlike Libor, the derivative markets does not use Sibor as a benchmark with Sibor’s use largely restricted to the home loan market

– DBS and other local banks have started to peg home loan rates to their fixed deposit rates which are solely in their control

– Singapore has 2 choices: 1. Do nothing and leave Sibor alone or 2. Do something with only 2 viable interest rate products to choose from that transacts in the marketplace—the SOR or 1-6M govt tbill

Flying Through a Whole New Dimension

Our imaginations are taken further to a whole new dimension this week, leaving us barely time to catch our breaths as we watch markets bulldoze through new record highs at a blistering pace that should make anyone who is fully invested start to worry.

The en bloc fever rages on, bordering on delirium with yet another landmark sale in Hougang of Florence Regency to B1 rated Chinese developer, Logan Property (3380 HK), whose stock price has sunk over 20% since the Chinese government curbs last month.

Source: Today

With 336 lucky en bloc recipients netting over S$1.8 mio each (vs last transactions of $900k- $1.24 mio), who says Housing Should Be for Living In, Not for Speculation?

President Xi, on Wednesday, was obviously not referring to Singapore, where it can be a case of currency speculation after the MAS policy statement and the expectations for a return to a modest and gradually appreciating SGD dollar soon.

Source: Bloomberg

In the 19th National Congress of the Communist Party of China on an “odd” numbered, therefore, important year, what we have read so far has firmly cemented the idea of China as a global leader of the “free” and “unfree” world, perhaps rising to de facto leader sooner than later. That could be due to Donald Trump, the unofficial de facto incumbent leader of the “free world”, appears to be more interested in imposing “totalitarian rule” and fixated in extending his domestic market capitalization, using the stock market as a benchmark of his policy, or lack of, success.

Chart depicting US Market Cap rising US$5 trillion in the past 12 months vs falling 5% in global market share

Ignoring the US’s falling share of the global market cap pie, Donald Trump has finally made some progress in passing a budget resolution for 2018 that will allow the budget deficit to increase by US$1.5 trillion over the next decade, paving the way for soon to come tax reforms that will be good for stock markets as companies are expected to spend their extra dimes on stock repurchases.

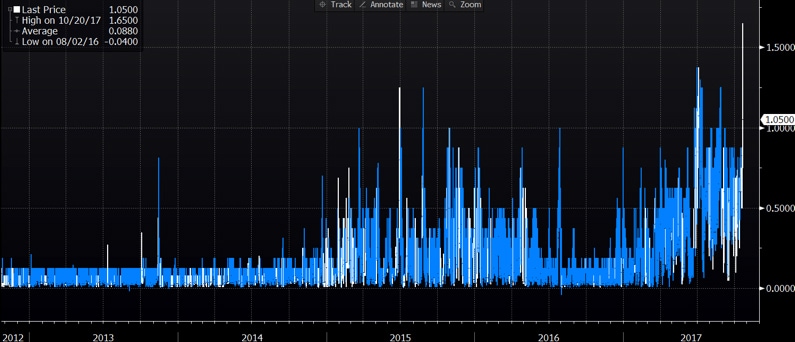

2017’s final deficit was released on Friday at $666 bio, the 6th largest on record and it is easy to start over imagining things as Bitcoin looks set to hit a $6,666 peak in no time, at the rate it is raced past $6,000, up 6.4% for the week, closing just under. But we will take our chances with the Nasdaq at 6666 first after a new high of 6640 on Friday.

Graph of Nasdaq and Bitcoin in race to 6666

Did we say, sleep easy, folks? Don’t imagine too much.

No Better Time To Talk About SIBOR

There is no better time to write about Sibor than this week when the Overnight rates hit a record level not seen since the financial crisis erupted 9 years ago.

Yes. The cost of 1-day money rose above 1.5% to an intraday high of 1.65% on Friday, inverting the curve and making 3-year interest rate look cheap at 1.6%.

Graph of SGD Overnight Money Markets Interest Rate

3 months ago, we warned about Preparing for Life Above 1% SIBOR and we did say it is for real although the retail market sometimes takes a little longer to realise for the lack of publicly available information.

And how wrong were we to expect leveraged returns to shrink or bonds, real estate and stocks to be impacted by higher interest rates with the hefty capital gains we have seen so far.

The Credibility of LIBOR and SIBOR

For years we have been questioning the existence of Sibor which has been around circa July 1987. What is Sibor if it does not trade, as we questioned in July? Why are the majority of Singapore residential home loans pegged to Sibor? What is Sibor if there is no Sibid? Why are we getting next to zero for those kiddy savings accounts?

We have written stuff over the years suggesting that Sibor is all but obsolete but we are not brave enough to give you the answers today because 1. We value our privacies against unnecessary attention in our highly censored lives and, 2. We do not get paid and so we learnt to shut up especially when nobody cares to read about such stuff unless it will help make them rich.

Nonetheless, we still strive to make the world a better place. Thus there was no point in gloating back in Jul when regulators announced that LIBOR would be phased out as a benchmark by 2021.

What will be useful to readers is that we may be able to value add, being former market practitioners, in explaining the various interest rate alternatives because everybody likes to read about how to make money or save money.

Now, does anyone know that Sibor is not covered by our monetary policy? That the central bank has no part in it in terms of guidance?

If the answer is No, please change to Yes before continuing.

Why is LIBOR Getting Scrapped?

CNBC summarised as follows.

1. Libor lost credibility as a benchmark after banks including Barclays, Deutsche Bank and UBS were, since 2012, fined by U.S. and British authorities for manipulating Libor submissions, in many cases to boost profits on their derivatives positions.

2. Libor is still viewed as fragile, however, as regulatory reforms since the 2007-2009 financial crisis have resulted in banks making fewer short-term loans to each other.

3. Money fund reform has also reduced demand for short-term bank debt. That means the rates are often estimated and not transaction based.

4. Data by ICE shows that only around 30 percent of U.S. dollar based three-month Libor submissions are based on actual transactions.

5. Regulators have pushed internationally to find alternatives to Libor and its equivalents. A British committee has selected SONIA, an unsecured overnight lending rate, as an alternative to sterling-based Libor and Japan last year selected TONAR as an alternative to yen Libor, also an unsecured rate. A group in Switzerland in May selected SARON, a collateralized rate based on the Swiss repo market, as a Libor alternative. The European Central Bank said in May it is ready to work on its own index of bank-to-bank lending after an industry-led revamp of Euribor failed.

There is just “not enough transactions underpinning the rates”, according to the CEO of the UK Financial Conduct Authority, Andrew Bailey, giving the example that for one LIBOR variant, only 15 trades were executed in 2016.

Barclay’s Bank estimated 70% of Libor submissions are now made upon “expert judgement” instead of genuine transactions and the risk involved “in generating such an important and highly utilized interest rate based upon expert judgement is enormous, especially in the wake of the Libor fixing scandals”.

That is a mighty big problem because Libor “underpins more than $3 trillion in syndicated loans, around $1.5 trillion in commercial mortgages and $1.44 trillion in residential mortgages, and another $2.5 trillion in mortgage-backed securities and other asset-backed securities, according to a report by the Financial Stability Board’s Market Participants Group in 2013. The largest exposures, however, are in derivatives. Libor is used as a reference rate in around $111 trillion privately traded derivatives and an additional $30 trillion in exchange-traded derivatives.”

The Libor Verdict

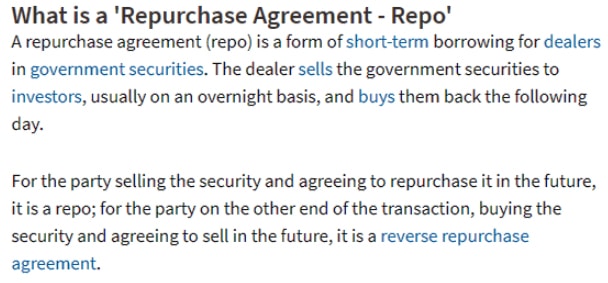

The GCF (general collateral finance) repo rate was selected over the Overnight Bank Funding Rate (OBFR), an unsecured bank lending rate based on transactions in the federal funds and Eurodollar markets.

Definition of Repo or Repurchase Agreement: Source Investopedia

The repo rate is an easy choice as a clear substitute to Libor given that US$ 600 bio transactions made overnight compared to half for the OBFR.

There is also some consistency between the repo rate and the “expert determined” Libor over the years because it all stems from the Fed Fund Rate (upper bound) which gives the markets some guide.

It Gets Complicated for Singapore

Now, it gets slightly complicated for Singapore because 1. There is no interest rate guidance in Singapore (monetary-without-interest-rate policy), 2. The domestic repo market is virtually non-existent and many banks are not involved in that area of business, 3. There is SOR (Swap Offered Rate), the other benchmark and 4. Sometimes there is an arbitrage to get around Sibor to access SOR which has been consistently lower in the past year.

We will endeavour to enlighten with a glaring example of the anomaly in the market today.

We have the 1M Sibor at 1%, unchanged for the past 3 months.

1M SOR was last at 0.86%.

1M t-bills issued by the Singapore government is 1.15-1.25%, on average.

- Now just imagine the Singapore government borrowing above Sibor—the rate banks use to borrow or lend to each other? One of those things that make you go Mmmmm …

Graph of 1M Sibor vs SOR vs SGD Govt bills

Now, imagine where the 1M repo rate should be?

Folks tell me that it is somewhere between 1-1.2% which gives SOR a huge upper hand!

What is SOR? Who gets SOR?

We will not overly burden and embark on the history lesson of why SOR came about, the concept of banks’ cost of funds, the old liability base computations, just suffice to say, SOR is derived from forward points supposedly to represent the interest rate differentials between Libor and SGD rates expressed in exchange rate terms, throwing in several other factors such as demand and supply and the big Section 757.

The trick of Section 757 is that not everyone can access SGD borrowings in SOR or Sibor because it is the privilege of only onshore tax residents/entities, to be able to borrow more than S$ 5 million unless it is explicitly for the purpose of buying SGD assets.

That means that anyone with access to USD at Libor will be able to buy 1M Singapore government bills at 1.25% and pay just 0.86% for it, earning 0.39% in a month instead of borrowing at 1% (Sibor) and make less.

Why is SOR So Much Lower than Sibor?

- Not everyone has USD to swap into SGD to take advantage of the lower SOR

- Banks are flushed with SGD customer deposits that they pay virtually nothing for while lending the money out at Sibor

- Sibor just does not trade a lot and is based on “expert opinions” these days

Starting to Look Unfair on the Home Loans

Home loans are generally going at Sibor+0.5% but, in DBS is offering their new fixed deposit home rate loan at 0.25% (9m Fixed Deposit rate) + 1.15% = 1.3%.

Why 9 month? How does DBS determine the rate? DBS has full control!

[Bizarre as it seems, some credit trader we know still prefers to pay 1.68% for 3 years fixed because that means they are only paying 3Y+0.05%]

Yet banks cannot afford to let customers take those SOR loans anymore given its unstable and volatile history, fixing at negative rates in 2011, against the interest of the banks even if SOR is mostly always lower due to our monetary-without-interest-rate policy.

The Story So Far…

We would disclaim again – that we have no intention of pointing the smoking gun at the system we hold dear.

Yet the story so far is that Sibor does not seem to be anything much and the best part of it is that, unlike Libor, does not have hundreds of trillions dollars’ worth of derivatives tied to it.

The flaw in Sibor is that it is just a benchmark based off, mostly, expert opinions (that we do not doubt) and yet the best “experts” who divine the rates each day are also probably the people with vested interest in the not much-traded product.

These are the options available for Singapore.

- Do nothing. Continue with Sibor for loans and use the new USD benchmark to price SOR.

- Do something in seeking a public consultation for a replacement rate because we are too important a financial centre to left out of the picture. The rates we can think off hand would be SOR or the SGD tbill rate because these are backed by genuine transactions. Develop the repo market to get those repo rates.

We think it is just best to come clean and just do away with Sibor on its 30th anniversary.

Those loans against DBS’s 9-month fixed deposit rate would be just as “expert” as Sibor and last we heard, MAS is still the central bank even if the Singapore government is borrowing 1-month money at a higher rate than Sibor these days.

No doubt you will be hearing more from us on further developments.