April Is the Cruellest Month Because of March

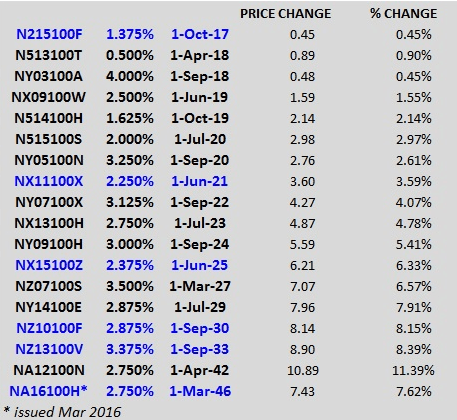

In March, 10Y Singapore government bonds saw their largest rally since Jan 2008, a whopping 0.44% crash in yield which added to the 0.34% decline we saw earlier in January. This makes 1Q16 the best performing quarter since 4Q08, ignoring the 7 month rally between Mar – Sep 2011 which saw yields edge 0.99% lower. In terms of price, this is a 6.5% move, but pales in comparison to the 11.4 % gain in the old 30Y government paper.

Even luckier are those who participated in the 30Y government auction at the end of February with a 7.6% windfall for holding on to a paper for just a month! This makes me wonder if Singaporeans know they can participate in government bond auctions too. And for minimum lot sizes of SGD1,000? Life is not just about the new capital-GAINLESS Singapore Savings Bonds …

Table of SGS price changes and profits for 2016

While we all wish we could say global investors finally see value in AAA rated Singapore and its first world economy, Thailand and Indonesia win hands down as far as the 2016 government bond rally is concerned and the Malaysian ringgit (+10.6% year to date) outshines Silver (+8.74%) and the Russian Ruble (+8.92%) in its biggest 1 month gain since 1998, with only Gold (+15.2%) looking better in the entire universe of recognisable currencies.

Yes, Singapore is merely a follower and beneficiary of the EM bond rally this year as US and developed markets show moderate results as Thailand (BBB+ rated) spirals out of control with the lowest 10y bond yields in their history at 1.57%, making US (AAA), South Korea (AA-) and Singapore (AAA) look slightly foolish with their higher yields. All this, without having to cut rates to negative as well, noting that the Thai central bank has overnight rates at 1.5%.

Market professionals are probably the biggest skeptics out there as they make their livelihoods from market inefficiencies of Singapore, tell me they prefer the market to remain under developed. A friend of mine who is in the bond business calls Singapore a first world economy with a third world bond market.

Emerging Market Singapore

Corporate bonds issued since Nov 2015 have seen only average price gains of 1% as the Singapore markets saw their first default since Lehman Brothers back in 2008 out of Indonesian company Trikomsel in the most blatant of all defaults that tantamount to almost bond holder abuse in the latest startling development where the company backed down on promises with the sudden mysterious emergence of a “new” bond majority holder who “supports” the move, taking the Mickey out of investors and regulators.

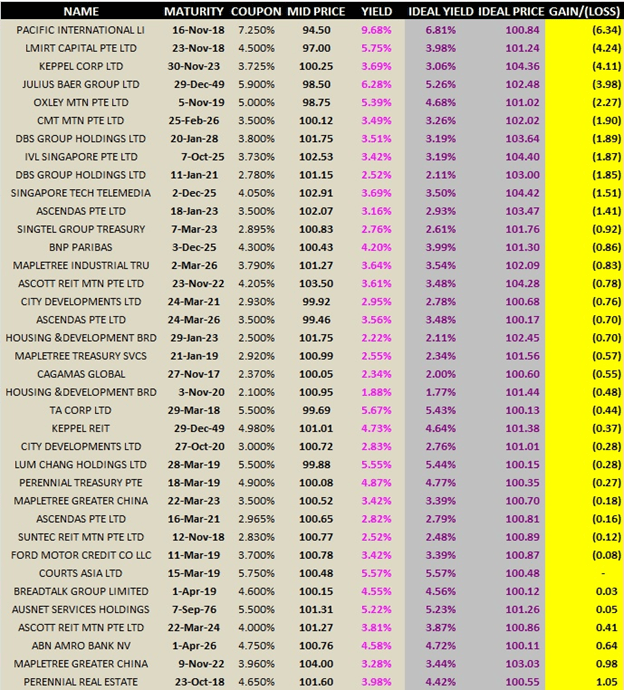

Taking a look at the worst performing bonds in our casually assembled list taken from bonds issued in the past 5 months.

The main takeaway is that investors have lost out! Even Temasek linked companies are not spared, led by Singapore Technologies, DBS Group and Capitamall Trust, given that DBS pulled off a coup when they replaced an old bond issue with a cheap new one, with the smallest of premiums for the new issue, a mere 0.18% higher than swap rates, which subsequently widened out at an opportunity cost to the investors.

Given the general level of ignorance in the public (which may not last given the “skills for life” propaganda), it is quite easy for a banker to advise their client that they stood to make 20% returns holding on say, Fraser Centrepoint perpetual because 5% coupon multiplied by 4 years gives them that amount, and advise the client to sell Cheung Kong perpetual because it had only 6 months left to run and could only earn another 2.6%. The banker did not lie for the record, even if the Fraser perpetual was 98 cts (and the customer paid 100 cts), because they did give the right numbers.

Several price makers in the market have long held to the belief that Singapore bonds should trade on prices instead of credit spreads or on relative valuations to offshore credits. It is for this reason that the Business Times proclaimed Singapore bonds winners last year, holding their own as government bonds fell, ignoring the massive credit deterioration that was affecting the rest of the world that resulted in a crippled marketplace of bid prices that could not be dealt on.

Perhaps a portion of blame could be laid on major investors who adopt the similar mentality of benchmarking their success to an absolute return, investing according to their mandates which meant buying some bonds to scarcity and shunning papers of value just because the bond did not have a specific rating regardless of who its parent company was.

When government bonds sell off because of deflation (opposite of developed markets) and rally on currency strength, when credit spreads improve against global credit deterioration and underperform amidst an improving outlook, Singapore has little choice but to take her place among the volatile emerging market lot.

It is an unavoidable situation and we should not look to the next MAS Monetary Policy statement in the next week (between 7-14 April) for any help with Singapore’s main trading partners mostly from the EM led by China, Malaysia and Indonesia.

On the part of the regulators, they will continue to pray for the marketplace to diversify to attract sophisticated investors into the fray in order to keep checks and balances on the state of the market. The hope is that we do not end up with local media headlines boasting about how Singapore bonds were bucking global trends.

On the other hand, it may be a good thing with the latest headline blaring out of Goldman Sachs to sell Asian currencies after their best rally since 2008.

“The currencies will resume declines as further easing in China and Japan is likely to push the yuan and yen to their weakest levels since at least 2008, says Kamakshya Trivedi, a strategist at the bank who correctly predicted in November that emerging markets would recover in 2016.”

We can then react with warped logic that SGD corporate credits will then outperform when crisis strikes and the rally turns south.

And if, as TS Eliot says, “April is the cruellest month..”, it is because we had March.