Bond Market Thoughts: The Royals, The Bad and The Ugly

You cannot help but read with great amusement that Singapore’s GIC gave a single B rated junk bond a blue-blooded kiss of life, leading to a fairytale rally for the notes that gained 28% after the announcement of GIC’s investment in the company.

“Since the Aug. 14 announcement, Greenko’s $550 million of notes due August 2019 have surged 11.9 cents to trade at 105.91 cents on the dollar on Friday, driving the yield to a record-low 6.21 percent, according to Bloomberg-compiled prices… The notes had plunged in November 2014 after India’s central bank said it disapproved of Greenko using an offshore unit to buy debt. They fell below 82 cents in the dollar in January before recovering throughout this year.”

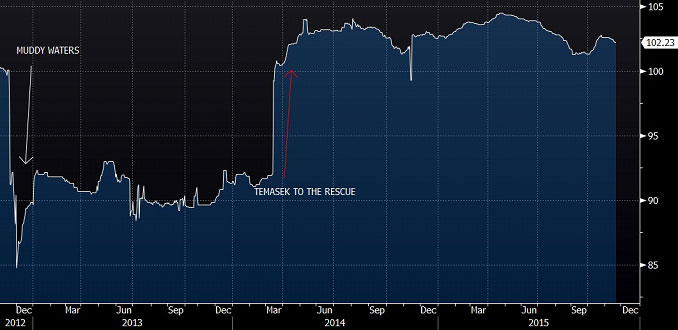

It brings back fond memories of Temasek’s direct invention into Olam’s fate back in early 2014, bringing relief to bond and share holders alike after months of suspense filled wait as we witness rival Noble Group’s troubles this year.

Noble Group would be a basket case if not for China Investment Corp holding just 9.5% of the company but that is apparently not enough, like in the case of Olam, to dissuade the short sellers until they put more money where they mouths are.

Others achieve royal treatment in the third degree. O&G companies like Ezion which managed to issue DBS’s committed funding backed notes a few months back, managed to save the day and redeem their perpetual bonds, paying 3.65% for 5 year money that is backed by a Temasek (30% owned) backed entity.

The bond markets in Asia are slightly different and have become even more so these days when retail participation is on the rise. What may seem as unorthodox selling points to qualified portfolio managers are basically all a company needs to get their notes fully subscribed as I will not be quoted for noticing that in the recent SGD Pacific International Lines bond issue, the fact that owner was also the head of the Singapore Business Federation was a key selling point for some of the RMs that I spoke with. Needless to say, 94% of the bonds were sold to private banks and their clients with 6% going to institutional buyers who were probably more sticky in their investment strategies and buying bonds of private companies.

Yet I cannot fault investors for their decision, having no view on the company or the bond issue after Goldman’s prediction in May that dry bulk shipping rates will only bottom in 2020 (and indeed, the Baltic Dry Freight Index just made a historic low last Friday).

It comes from the common sense school of investing that Warren Buffet has made famous, giving us self respecting folks hope of becoming great investors just armed with our wits and logic. And the results are showing up with credit spreads tightening across the board this year lead by the mad grab for state protection or royal blood and blue chips.

No complaints yet as the anomalies pop up daily – parent company Singtel (Aa3/A+) USD 10Y bonds trading at Libor+1.2% versus lower rated Optus (A1/A) SGD 3.24% 7 year bond trading at a credit spread of 0.5% and Capitaland (unrated) 4.076% USD 7 year trading at Libor+1.85% against City Developments’ 3% 5Y SGD paper that is yielding only 0.6% higher than SOR.

Blue blood and blue chips all rule, with demand driving SIA 5 year notes to the tiniest of premiums at just 0.3% for 5 years and it is a shame that NOL bonds had to sell off after the takeover news mainly because the new owners are unlikely to be as creditworthy as Temasek, whose bonds in USD are, ironically, trading at wider levels than most of her subsidiaries such as SIA.

Even the only Singapore government guaranteed bond in the world (that is not Singapore government issued and fully owned), Clifford Capital (AAA) 1.625% USD 2018 gives a nice pick up of 0.7% for 3 years.

I suppose royal treatment can only go so far and is worth about that much offshore and in the eyes of the international investors or punters, there is little discernible difference between Olam and SIA, perhaps ? And Greenko bonds could outperform NOL soon?

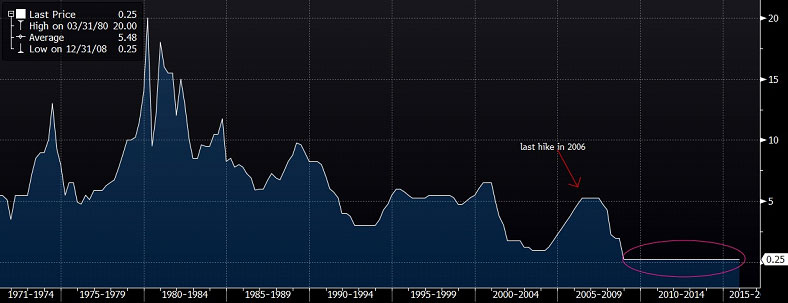

Enough with the little ironies of the little Singapore bond world, because there are greater anomalies afoot in the real world. Anomalies stemming from the strange times that we live in and that portend more strange times ahead as we head into the “dovish” rate hike, the first Fed hike since 2006, waking the markets up from the longest period of Fed rate inactivity in history.

As we observed in September, we have sat through a 30 year bull run in bond yields, a “0.25% move in rates will be quite devastating on bond prices indeed… Yet, all that has been priced in with most bond holders seeing a loss on their holdings for the year to date as I pointed out a fortnight ago that we can now find over 5,000 hard currency benchmark bonds yielding over 6% when there were only 1,000 just a few months back…” It is just as bad if not worse now with US swap spreads continuing into a negative descent for 2 months (since late Sept) with US government bonds yielding most over swap rates in history.

At the same time that China and Japan are lightening on their claims on the US, and as Norges Bank decides to bank on real estate while dumping bonds, for the US, there are enough foreign buyers for US treasuries to keep the status quo which does not explain the negative swap spreads and the best possible guess is that banks cannot hold too much of them due to balance sheet constraints.

Elsewhere, investors are unloading bonds, according to the latest numbers where investors pulled $1.12 bio from US fixed income ETFs in November leaving us wondering that if US treasuries are yielding above swaps because banks cannot hold too much of them, where will the rest of the corporate bonds go when investors decide to sell? Although there is plenty of hope that it would not be happening soon after the “dovish” rate hike.

We are starting to hear stories of banks stuck with piles of debt they had underwritten as the NYTimes reports: “A large portion of the paper losses is from debt issued by Veritas, a software entity that the private equity firm Carlyle Group is buying in a $5.5 billion leveraged buyout. Morgan Stanley and Bank of America led this transaction. A lack of demand for the debt has effectively left it on the books of the banks.”

Yes, with such ominous signs, maybe a bit of common sense to discern between the good, the bad and the ugly and realise maybe that is why the “royal bonds” are getting more expensive.