Can We Bring Back The 5 Year Singapore Government Bond Futures?

Market Bash: All About Trump

We can feel the levels of frustration build up, anxieties growing that just about anything can be construed as the tipping point for the correction of the stock market that just will not happen! (by correction, Investopedia defines as the negative price action of at least 10% and we are just -2.8% from the historic high on 1st March)

Trump bombs Syria along with a dismal Non Farm Payroll number last Friday, 7 April, and stocks barely budged. And so, the market has taken to enacting their version of a correction by buying up treasuries and gold and selling the USDJPY (down 7.7% ytd), blaming it first on Syria and then Korea, to throw caution to the wind on every single rate hike mentioned by Fed speakers this week.

The best part of the entire parody is that it all about Trump whom we hate so much, given his unpopularity ratings which makes it easier to assume that investors are more likely to hate than like him.

And all it took for the S&P to break out of +/- 0.35% trading range for a record-breaking streak (since 1968) of 10 consecutive days, was for Trump to appear in a WSJ interview to comment the USD was too strong and he liked low rates, which caused the S&P to close 0.38% lower and another 0.68% lower the following day. The power of Trump’s comment could be compared to feats that only QE could achieve.

With warships sailing from Singapore to the Korean peninsula, the US VP dispatched to Korea and Japan (then, Indonesia and Australia), we can safely assume that not a single fund manager would not be long (or at least, neutral) US treasury bonds and the majority of the market would be short USDJPY – because it is just too hard to short the S&P. That is the textbook prescription for a long risk-off weekend into a new week where Trump will call the shots again, and not just the missile shots.

And my textbook answer to this is that sometime in the future, we shall witness a massive decorrelation trade unwind.

End of Bash.

Singapore, Please Bring Back the 5 Year Bond Futures

I have been cajoled into writing this post by a dear friend who put forth the challenge to me to speak up, as a responsible member of society and a loyal Singaporean, as a suggestion to the proper authorities (who might chance upon this post), of whom I am unworthy to critique.

Thus we shall start with a little story of a chance dialogue I happened to have had with an old school friend who invested into the latest FNN 10 year bond on Thursday. From my previous experience of talking to bond investors, for instance, friends who had bought into Rickmers (now in default) after its first crash from 100 to 94 cents, I knew it was a tough un-sell. Yes, we know your RM says (yes, you are important enough to have an RM that calls you) that 3.8% is a steal for an “investment grade” name like FNN (potential mis-selling because there is a proper definition for “investment grade” and FNN does not fall into that definition) and your RM is so smart (though not as smart as me when it comes to bonds, I suspect) so yes, you did the right thing because you have already bought it anyway. And it is ok if you do not know that this is Fraser’s 7th bond issue in SGD for 2017 via FCL, FCT, FCOT and the last FNN.

Perhaps your RM is also eyeing that new Panamera Turisimo or a nice semi-d around the corner? It is not my lot to tell you that, thanks to your purchase, the bond should be worth 103 if it had paid up its initial mooted coupon of 4.15% instead of the 3.85% for the next 10 years that you are happy paying 100 for.

My only reply was “good on you, my friend, congratulations”. And now I say, “MAS and SGX, can we please bring back the 5-year bond futures?”

Can We Please Bring Back The 5 Year Bond Futures?

Times are fluid and Singaporeans are grateful and lucky that our authorities are trying their best to financially educate us with Moneysense, in partnership with SIAS, as “approved trainers” are unleashed onto the public whilst yours truly, here, has not heard back from IBF and SGX for my vain attempts in bringing out my bond seminar to the masses, no sarcasm intended for my lack of qualifications, no doubt.

Yes, please guide and educate us, the public, in local interest rates and market developments.

Instead, we have degenerated, if I can profess as a personal opinion, now that interest rate data has become further more inaccessible to the public than ever, since ABF decided to start charging for daily, “live”, fixings of SIBOR and SOR, which can seem perfectly unimportant, to me for instance, because I have long since come to the conclusion that SIBOR is a myth, as I have been informed by a few industry professionals that interbank (the “I” in the SIBOR) lending and borrowing has grinded to a halt and does not extend longer than a week or a month, let alone 3 months which is what most of us are using for that home loan rate.

Why 5 Year Bond Futures?

1. Investors need a hedge and there is none available for Singapore interest rates except for the handful of institutions that can trade those interest rate swaps via their ISDA agreements at a wholesale amounts (>5 mio).

2. Retail investor participation in the bond markets has grown over in recent years, increasing their exposure to the bond market when there is little information available on long-term interest rate levels (besides knowing short term SIBOR fixings 7 days late). There are no benchmarks readily available for the public to access as a gauge of whether bond price trends unless one monitors the MAS website religiously for the daily bond price closings.

3. Most investor portfolios are clustered in the 3-to-5-year bond tenors, just examining the maturity profile of outstanding bonds and hence the demand for interest rate hedging would be in the 5-year tenor.

4. 2-year government bonds make poor hedging given that the short term papers are usually held as liquid assets in banks’ investment books and thus those prices are heavily influenced by bank demand and supply, sometimes distorting the yield picture.

5. Similarly, the long end government bonds that are 10 years and usually less liquid with less investors and sometimes more speculators participating in that space, which really does not make it a good place to start in the name of hedging.

6. Lastly, the 5-year government bond futures existed a decade ago after its initial launch in 2001 and as far as we know, it is still supposed to exist if we take a page from the MAS website and the Singapore Bond Market Guide last updated in 2012.

Source: MAS

Why Did The 5 Year Bond Futures Disappear?

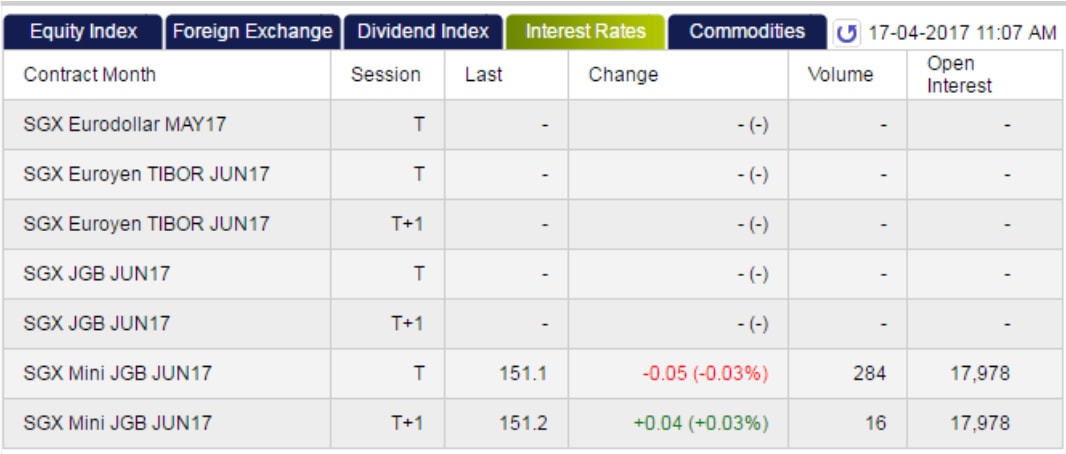

We cannot find any signs of life on the SGX, under the interest rates derivatives section.

Source: SGX

And we cannot be certain really what happened to the 5-year bond futures, but most people regard it as a fiasco and almost no one I spoke to remember anything about the “short-term interest rate futures contract” mentioned in the Singapore Bond Market Guide.

From what we can gather, the 5-year bond futures was introduced a little too early, during market infancy and in the eagerness to make it a success, primary dealers were all roped in to make mandatory prices for the instrument.

The relatively lack of transparency in the old days, along with the absence of a robust bond repo-market, led to the severe market distortion especially when there were lack of market participants and market depth. Arbitrage opportunities could not be bridged as a result which left initial supporters quite disillusioned and the market eventually withered and ground to a halt.

It is pretty much like the 1980’s when the futures market took off in America, on rocky terms at the outset as market players struggled to grasp the, then new, concept, yet managed to blossom and boom as more players came in to bridge the gaps.

Who Said It Will Be Easy?

The main resistance to the 5-year bond futures are, indisputably, the government bond market makers, of course. For some of them, the idea of revisiting the distasteful losses they have incurred in the past when the prices diverged at their expense when the big players of the market place withheld liquidity.

The price tag was painful, as some informed me, that the authorities extracted a commitment to make markets for the exchange.

The concept of cash settled also complicates the picture because foreign players cannot borrow more than SGD 5 mio unless it is for the purpose of buying an onshore asset, according to the MAS’s non internationalization of the SGD dollar notice, which means that the bond futures will have to be a deliverable contract.

For small markets like the SGD government bond market, having a bond futures contract would expose the market to higher levels of foreign speculation which the market may not be prepared for, although we are not sure how the Australian market managed to pull it off with their 3 year and 10 year bond futures amongst the 10 most traded long-term interest rate futures contracts in the world—both cash settled, of course.

The Silent Support

The odds are indeed stacked up high against the idea of reviving the bond futures market and if our authorities did their usual rounds of consulting the market participants, the idea will probably be buried even if we all know inside of us that it will make our little domestic market just a bit more complete and slightly more credible, not to mention, the long term good it will do for investors out there.

We cannot doom ourselves to the certain failure because of what happened in the past and the investing public would, no doubt, voice a majority support for the idea.

Think about what could spawn from this?

We could revive a functioning repo market? Investor comfort levels would rise as an avenue to hedge bond portfolios open up? Increased public awareness to financial developments to boost the financial education cause?

Singapore can look to cement her spot as a Aaa financial market.

I think I have said enough and I think you know what I mean.