Singapore Bonds: Fact Checking The News

Weekly Market Bash Is No Bash

There is little to say about markets this week except to applaud the keep calm and carry on behaviour, with no major terror incidents in the developed world unless we count the Melbourne hostage incident or the hammer attack at Notre Dame, Paris. The weekly suicide bombing rotated to Tehran this week, which may not be that surprising given Gulf tensions amidst the embargo on formerly AA rated Qatar (now cut to AA- which is closer to Saudi’s A-, recently cut from A in March) who can only count Turkey and Iran as her allies from here.

Perhaps the Qatar annexation has done some good in containment or the would-be-terrorists have been too riveted by the Comey-Trump testimony (for we cannot have a week without Trump in the headlines) or the results of the British elections, it is all hard to say except that the keep calm and carry on strategy has worked for the S&P 500 to hit yet another record high during the day on Friday before coming to a screeching halt as tech stocks hit the brakes. The index somehow closed the week lower giving the Nasdaq its worst day since September 2016, and giving the rest of us out here some hope for sanity in the world at last in the meanwhile.

We Cannot Guarantee The Sanity of The Reporters

Sanity reigned in the bond markets as the market took the Banco Popular collapse in its stride, calmly accepting the wipeout of all outstanding subordinated debt which was priced between 50 and 70 cts the night before Banco Santander, Spain’s largest bank, bought the 5th largest bank in Spain for a token €1 on Wednesday. In the process, senior Popular debt rallied some 10-15% from 90 cts to over a dollar, a slap in the faces of the sub debt investors, all wondering why the ECB permissioned the government led rescue of Monte dei Paschi just a week ago and forced Popular to close?

While we are on track for keeping calm and carrying on, we cannot guarantee that Business Times or Bloomberg is doing the same with headline grabbing articles like Four Singapore companies with bond deadlines to watch published last Wednesday, in what appears to be a random pick of 4 companies, causing market experts to scratch their heads in wonder, amazement and almost incredulity.

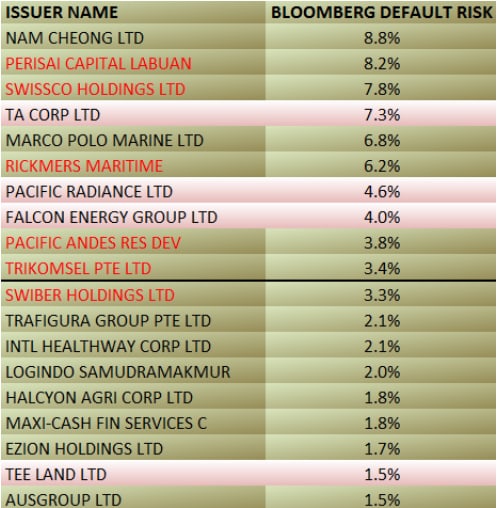

Source: Business Times

The claim that TA Corp (7.27% risk, bond price 95.4 cts), Pacific Radiance (4.21% risk, bond price 20 cts), Falcon Energy Group (2.48% risk, bond price 70 cts) and Teeland (1.44% risk, bond price 99.5 cts) are on watch-list for default because of a “Bloomberg default risk model”, which is universally known among market experts to be highly flawed especially in the realm of Asian credits?

The screaming question in everyone’s minds is, “Where is Nam Cheong?” 10 of out 10 market pundits would unanimously vote Nam Cheong as the next Big-Default risk because Marco Polo Marine is as good as gone, with their bondholder meeting on 15 June. Besides, Nam Cheong has admitted to a “going concern” risk just last month.

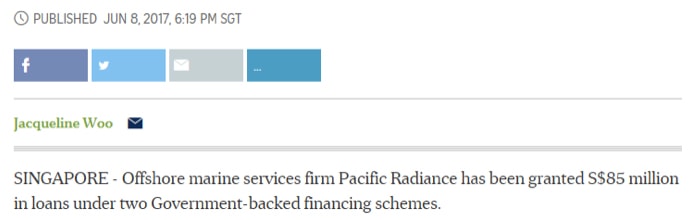

A bond trader we spoke to joked that if that “Bloomberg model” works then Pacific Radiance would be a screaming buy with its default probability at 4.16% and the bond is trading at 20cts which means there is a 95% chance of making 80cts? [Note: Pacific Radiance just received S$85 mio in government-backed financing on Friday so maybe we can tick that name off in the near future?]

Is there any chance investors can sue the banks? TA Corp was issued a year ago when its default risk, according to the article, was a screaming 3.4% high?

Thus, we have been implored to write a keep calm and ignore the ignorant reporter THE IGNORANT REPORTER piece by some friends as my part for social service and for the fools would believe and act on their claims which, as I was informed, did happen, as some panicky investors started selling whatever they could find a bid for.

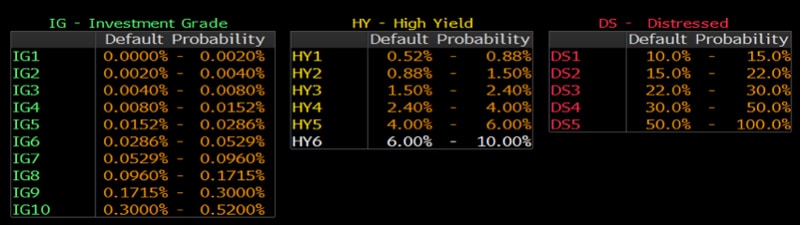

Fact Checking The Bloomberg Default Risk Model

First, we would clarify that Bloomberg has several default risks to choose from and it would appear that the reporters picked the 12-month default risk percentage over the 2, 3, 4 and 5-year default prospects.

- The Top 19 Companies At Risk, according to Bloomberg (we did a random cut off at 1.5%). We highlight the reporters’ picks in pink and have defaulted companies in red.

- Bloomberg Model wins, Reporters Lose! Yes, they missed out BIG-Time on the Nam Cheong case, while pursuing little Tee Land which ranks far below.

- Nam Cheong has a higher default risk than 6 already defaulted names.

- TA Corp has a higher default risk than 4 defaulted companies! (**TA Corp should consider 1.suing or 2.strongly word a response?)

- 4ct TA Corp has 50% more chance of default than 20 ct bond, Pacific Radiance and Marco Polo Marine which is on the verge of default.

- What about that entire list of names between Swiber and Tee Land? There is significantly more at stake in those than Tee Land’s outstanding SGD 30 mio. E.g. Ezion, that nobody dares talk or write about?

- We have no idea what Logindo Samudramakmur is doing up there, being 100% guaranteed by UOB Bank, even if it is a subsidiary of Pacific Radiance.

Interestingly, the possibly-flawed Bloomberg model has failed us in the past because nothing in the SGD bond universe comes up in the Distressed category (Surprise!) which meant we were all caught by surprise, when low-risk companies like Swiber defaulted on us without a single “distressed” rating call.

Taking a look at the scales used and realise how little use it would have been for someone who had bought Swiber or Marco Polo Marine etc., because they are still nowhere near the “distressed” >10% zone. In any case, just about 250 bonds in the entire world are considered default risks by Bloomberg although 60% of the 250 belongs to the same issuer—Banca Monte dei Paschi.

Can we conclude that the model works best for developed companies in developed countries?

Credit Analysis is Not Cheap or Easy

For one, fixed income credit analysts i.e. bond analysts are paid way more than equity analysts and we are talking about, potentially, several-fold. Perhaps analysing future cash flows is a lot harder than putting a number to profits and sales which are future cash flows too but we can suppose that there is much more number crunching in a more complex way. We are jealous all the same.

Rating the 4 names (TA Corp, Pacific Radiance, Falcon Energy) which now increasingly appear quite randomly selected, we only have 1 possible problem on the radar with Falcon Energy calling for a bond holders meeting on the 14th of June which may or may not result in buying some time for the company to dispose of its majority stake in Chuan Hup Offshore, the only, disputably, “debt-free” mainboard-listed O&G company in Singapore.

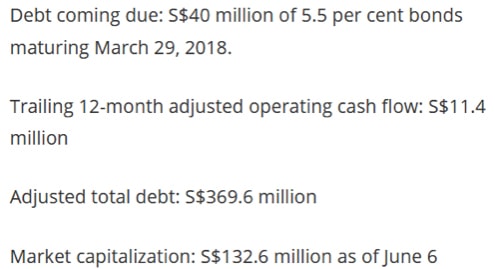

TA Corp? 2nd runner-up in the Most Likely To Default list, according to Bloomberg and their reporters’ analysis is found below.

How about assets of SGD 459 mio? A clean number because they have already entirely written off their China investment and all their assets and receivables there? They also wrote down their Tuas dormitory and still have SGD 90 mio of cash at hand versus bond maturity of SGD 40 mio.

[This is why we do not attempt to publish proper credit analyses or make it our business to make money from them except for discussions with close friends.]

There is nothing much to say about Pacific Radiance who managed to secure SGD 85 mio in government-backed loans just one day after being called out.

Source: The Straits Times

Finally, little Tee Land, somehow dragged into the fray as reporters are unaware that their cash balance has risen to healthy levels after their Australian hotel sale that completed in May and should be quite ready to pay off that SGD 30 mio bond maturity in October with that being their only liability for this year.

How About A Good Story For The Reporters Who Want To Write About Bonds?

How about a Trikomsel’s potential fraud story? Discrepancies were found in their financial statements by auditors but nobody is doing anything about it except the bondholders. Which reporter will have the guts to report about this?

Clipping of Trikomsel auditor statement, unverified for source or accuracy.

How about Pacific International Lines? The private company has SGD 430 mio worth of bonds outstanding, 300 to mature this year and another 130 in 2018. The 2018 tranche is trading well under water, at mid-80 cts which hardly seems justified even if they (as a private company) do not have a Bloomberg default risk score.

We read somewhere that the chances of success or debt recovery in defaults for Asia are about 3 times less than what it is for developed countries, Singapore is probably unexcepted. Why did Ezra choose to file for Chapter 11 than work with Singapore-based judicial managers? The word out there is that it is a slow bleed for fees before the death knell. It’s unverified and probably untrue, but possibly worthy of investigation.

In Signing Off

If we wanted an attention-grabbing headline, we would title this post, Let’s Arbitrage The Reporters And Buy Those Bonds After Misleading News Drive Their Prices Down? [not to be taken as financial advice]

We are not here to bury the Bloomberg Default Risk (DRSK) function or our local reporting, for that matter, because we are a generally peaceful bunch of Singaporeans who did not bother to report on many bond market reporting inconsistencies we have come across in the past. For goodness sake, the SGX would not even consider us qualified to run a bond seminar for them, a conclusion we reached after several emails went unreplied.

Thank goodness, the market still remains imperfect and it perfectly suits those who will do their homework to sieve for information and pay for good information like this new source we discovered in paid service, Reddintelligence, whom we will be crediting in the weeks ahead.

What happens when we live in a world with such abundance of information that patients can tell doctors what is the matter with them or call out a doctor’s wrong diagnosis?

The flipside is that we tend to get overwhelmed and accept information and reports at face value. The choice is really ours to make just as we have chosen to write this, for our part, as national service and not as vigilantes, with no ill will, intent or, least of all, criticism.