Singapore Corporate Bonds: Wishing Us Good Luck Into the New Decade

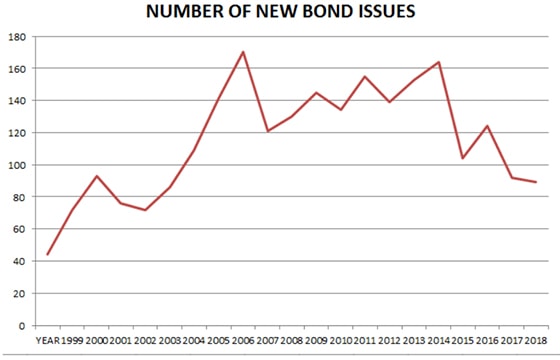

Coming to a very quiet end of another decade in the Singapore corporate bond market and we cannot be faulted for wondering where 2019 went. We are going out on a whimper with the lowest number of bonds issued since 2004 (84 new bond issues) at just 89 for SGD 24 bio, tumbling from peak bond year, 2012’s SGD 31.6 bio, and notching a new low from last year’s 92 issues versus the decade’s average of 134 or 135.

Graph of number of SG dollar bonds issued since 2000. Source: Bloomberg

Graph of number of SG dollar bonds issued since 2000. Source: Bloomberg

The healthy increase in total issuance over 2018’s SGD 22.1 bio is largely attributed to a private placement of SGD 1.5 bio of Sembcorp bonds to Temasek Holdings in June, without which total bond issuance would have flat-lined from 2018 where we saw the last default which is still dragging on—Hyflux.

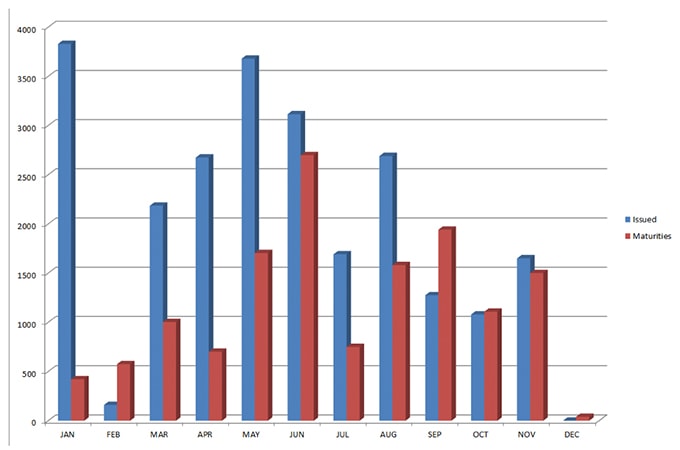

2019 bond issuances versus maturities (unverified)

2019 bond issuances versus maturities (unverified)

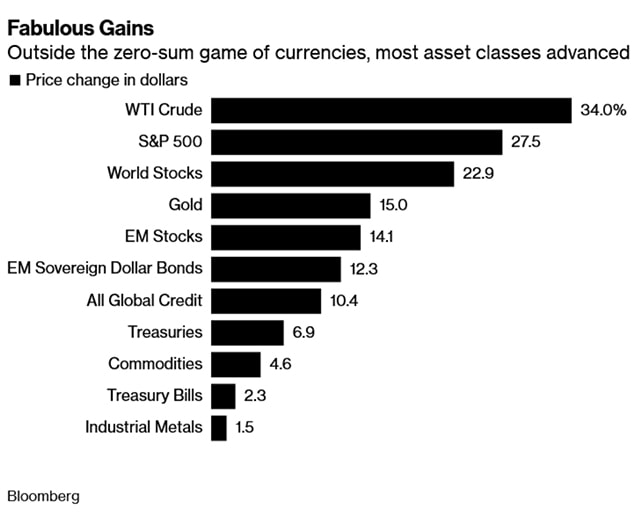

Elsewhere in the world, it has been a stellar year with “the world’s major asset classes collectively on course for the strongest annual performance since 2009” to end a spectacular decade with Singapore bonds on track to largely underperform the double-digit gains in global credit, emerging market dollar bonds and also US Treasuries’ 6.9% returns. The ABF Singapore Bond Index Fund of government bonds has returned 4.4% year to date and Nikko AM SGD Investment Grade Corporate Bond ETF just 0.8% higher at 5.2%, which is still not bad considering 10-year Singapore government bond yields are barely scratching 1.75% having had a lousy year (higher than Japan, Taiwan, Australia, Thailand, HK, New Zealand, South Korea and nearly all of Europe except for Hungary, Poland, Romanic, Russia and Iceland) compared to the rally that engulfed the rest of the world.

TLC (Temasek-Linked Companies) Developments

Interest rates aside, credits also had a tumultuous year in Singapore and especially in Singapore where everything did not fare so well despite the lack of defaults. The Capitaland acquisition of Ascendas-Singbridge Pte Ltd from Temasek in January to create the largest real estate group in Asia with assets of over S$116 billion was not good news for the bonds because spreads blew out and have not recovered since. In fact, Capitaland bonds widened some 20-30 basis points (0.2-0.3%) and have been holding at those levels, spreading the contagion to the rest of the real estate bonds which make up about half the market out there (including the REITS and real estate developers) if we would want to include the likes of Metro and SPH (with their substantial real estate exposure) or not.

Source: Bloomberg

Source: Bloomberg

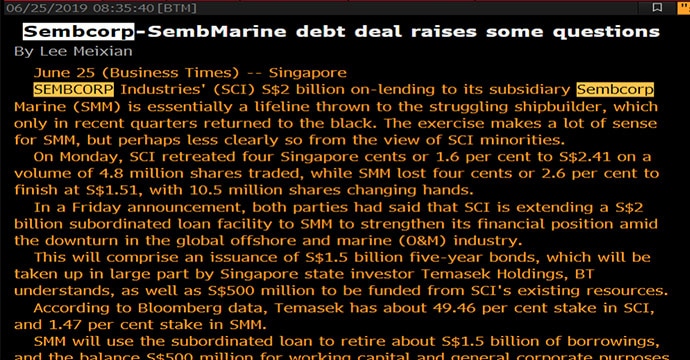

And then we had the somewhat odd Sembcorp Marine “bailout” mid-year that caught everyone off guard and slightly perplexed when Temasek provided Sembcorp Industries a 5-year loan for SGD 1.5 bio for Sembcorp Industries to provide a 5-year subordinated loan of SGD 2 bio to Sembcorp Marine which was credit positive overall for them all.

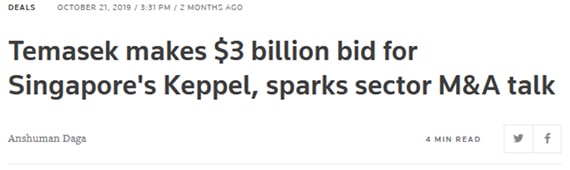

The entire deal raised some questions almost immediately from the minority shareholders’ standpoint especially when it did little to help the stock price, looking much like a state-led bailout which helped the Keppel deal that came next.

The Keppel deal was an outright takeover offer in October for majority control of Keppel Corp for the purpose of a Sembcorp Marine merger. That went down well, for the S$4.1 bio Temasek was willing to splurge for a 51% stake in the company, paying a 26% premium over Keppel’s last closing price.

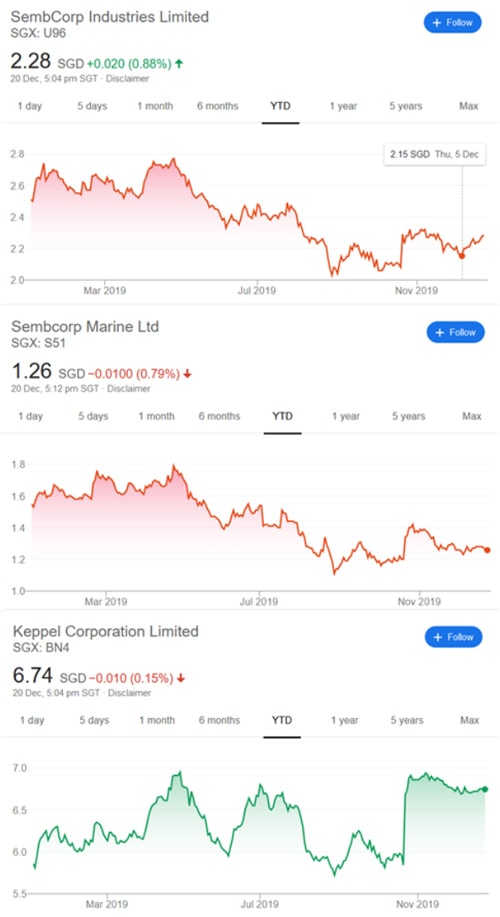

The stock market cheered Keppel, Sembcorp Industries and Sembcorp Marine although Sembcorp is still in the red and has a long way to go by the looks of their share prices in the charts below. Nevertheless, their credit spreads posted huge contractions to catch up to Capitaland’s, for the Temasek boost.

SembCorp Industries, Sembcorp Marine and Keppel Corporation stock prices YTD. Source: Google

SembCorp Industries, Sembcorp Marine and Keppel Corporation stock prices YTD. Source: Google

Looking into 2020, it does look like Temasek is not done with these two or Capitaland or maybe the rest of her stable of companies, which also represent a chunk of the Singapore bond market. It would be fake news to speculate and thus, no point losing sleep over it.

2019 Retrospective

2018 still holds the record for billion-dollar issues but 2019 can claim to have the most mega benchmark issues that are SGD 700 mio (USD 500 mio) and above which more or less explains the lowest number of issues since 2004.

17 Perp Issues—Singapore issued more perps in 2019 than the total of 2014 to 2016, 42% more funds were raised than peak perp year 2017 were we saw 15 perps issued. Just less than 30% of total issuance for the year and roughly 32% of total issuance for the year were subordinated bonds.

New record low coupon for a SGD perp—UOB breaks the previous low coupon set in 2017 by Mapletree Logistics (3.65%) to pull off a 3.58% coupon and congratulations to the buyers because the bond is yielding just 3.13% 5 months later, to make us wonder if we can see a sub 3% coupon for a new perp issue next year?

List of perps issued in 2019, a record year

List of perps issued in 2019, a record year

Table of perp issues over the years

Table of perp issues over the years

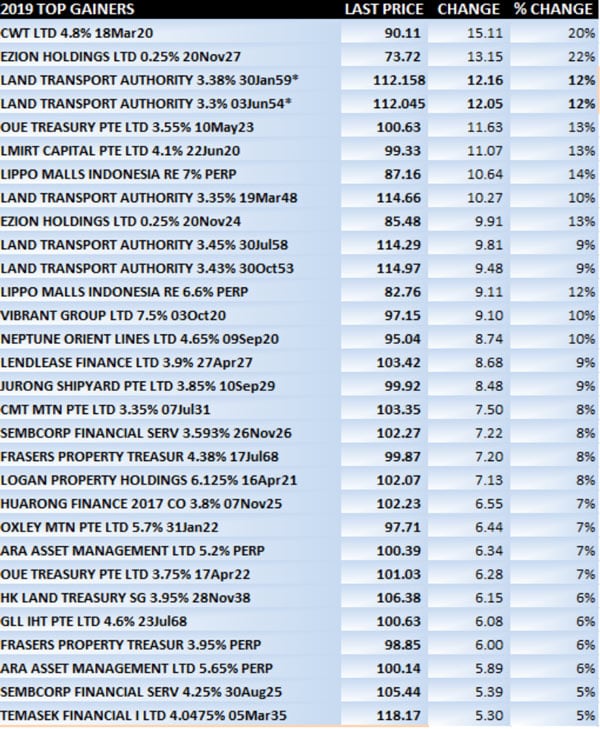

The drop in interest rates and the flattening of the curve did much to rake in capital gains for many a long end bond holder and the almost instant 12% profits in LTA 2054 and 2059. Yet, the rest of top gainers saw massive credit improvements although the prices cannot be verified, it is most certain that Jurong Shipyard (Sembcorp Marine), Sembcorp, the Indonesian property names like Lippo, LMIRT and related OUE as well as CWT and Ezion would have justifiably improved.

Table of top-performing bonds of 2019 (unverified) *Issued in 2019

Table of top-performing bonds of 2019 (unverified) *Issued in 2019

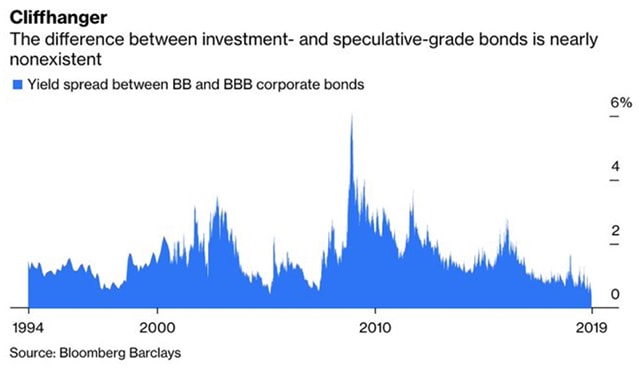

It is unsurprising that many of the down beaten names of 2018 have staged a comeback rally because it is a global phenomenon in 2019. Whilst Capitaland senior has widened since last year, the Logan’s and Fraser’s are catching up because as Bloomberg pointed out, the “difference between double-B and triple-B bond yields is just 38 basis points, the smallest in at least 25 years. Effectively, there’s no ‘ratings cliff’ between investment- and speculative-grade bonds”.

Hyflux senior bond holders are the clear losers for 2019; poorly rewarded for their astute foresight, suffering a lower coupon in return for less protection while perp holders enjoyed that 1.4 to 1.8% incremental coupon return for years that more than make up for the 7 cts vs the 12 cts valuation at the moment. Which is perhaps why 2019 is PEAK PERP YEAR! It just goes to show so much for investor education and the safe bet of seniority—seniority doesn’t work in Singapore defaults?

PIL and Century Sunshine both missed their call dates for their USD and SGD bond respectively and thus the supposed lower prices (unverified).

Table of 2019’s biggest losers (unverified prices)

Table of 2019’s biggest losers (unverified prices)

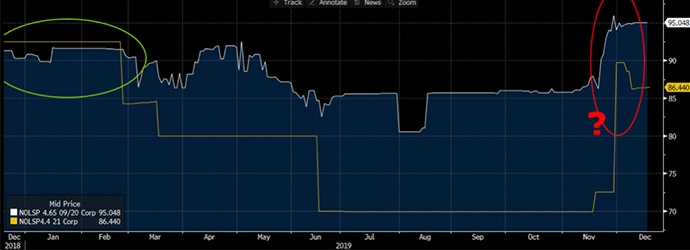

We cannot explain why SingPower bonds have lost out despite their longer duration when all the other long duration bonds have outperformed but we can probably blame the HK riots for Wharf. We also note with irony and interest that NOL appears in both the best and worst performing bond list in some idiosyncratic price action for the year in the graph below.

Graph of NOL 20 and NOL 21 price action in 2019. Source: Bloomberg

Graph of NOL 20 and NOL 21 price action in 2019. Source: Bloomberg

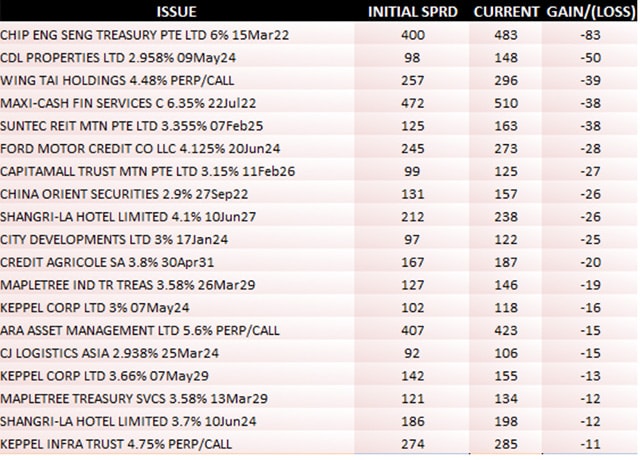

The worst credit performers for the year were quite difficult to get hold of, given the patchy sources of data but we approximated a table of top losers issued in 2019 which looks about right considering the credit deterioration contagion caused by Capitaland, the HK riots on the HK exposed names such as Wing Tai and Shangri-la, the global auto sector woes and such. Yet, we would also blame the lack of trading and market depth that condemns bond prices to stagnate after their issuance for some of the wider spreads.

Table of the bonds issued in 2019 that suffered credit deterioration (unverified)

Table of the bonds issued in 2019 that suffered credit deterioration (unverified)

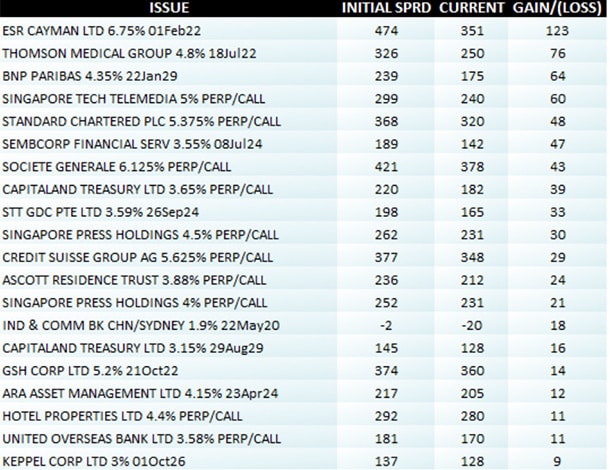

The bonds issued in 2019 that saw their spreads tightened can thank generous banking lending limits for their gains. ESR Cayman and Thomson Medical Group both outperformed and have something in common—the fact that Credit Suisse is a lead manager for the deals. The perpetual bonds dominate the list (Peak Perp Year) of course, as investors sought for yield in the face of higher funding rates.

Table of bonds issued in 2019 that saw credit improvements (unverified source)

Table of bonds issued in 2019 that saw credit improvements (unverified source)

We note that both Capitaland bonds issued in 2019 (at wider levels) have improved, tightening since their issuance but the Capitaland perpetual (5-year call) has closed a meaningful gap with its senior 10-year note to have both bond trading within 0.35% of each other despite the differing levels of seniority. Perhaps the market has learnt from Hyflux, that the seniority is of scarce importance in defaults?

Chart showing yields of Capitaland perpetual bond converging with its senior paper

Chart showing yields of Capitaland perpetual bond converging with its senior paper

Into a New Decade

We can say Singapore markets spent a better part of the last decade in consolidation, starting the decade with a roar and seeing peak bond year in 2012 before the defaults started hitting in 2015, peaking in 2017 with 9 defaults after 5 defaults in 2016 and ending in 2018 with Hyflux, miring some 34,000 retail bond holders in the process—with their fates still in limbo to close the decade on a low note.

Market dynamics have changed in the past decade with retail participation on the rise and sometimes distorting credit valuations although that is proving to be slowly changing as sophistication improves.

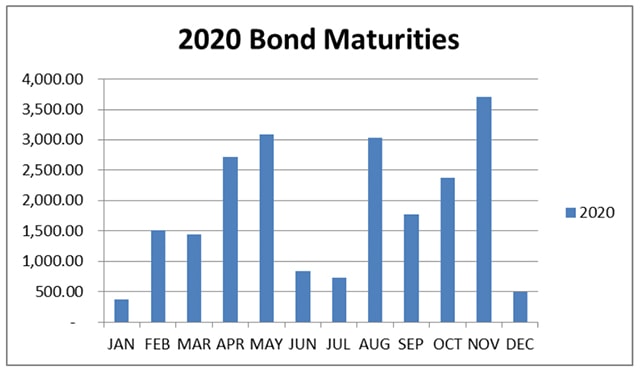

There is a whole lot to worry about in 2020 where we will see peak maturity match the last big maturity year of 2017 where some $22 bio matured. 2020 should see the same amount of bonds maturing or called, excluding the already defaulted papers.

Table of bond maturities in 2020 by month (unverified)

Table of bond maturities in 2020 by month (unverified)

We prepared a table of the largest ones and note the usual suspects.

Table of large bond maturities in 2020

Table of large bond maturities in 2020

There are also a small handful of high-risk maturities which we will not talk about with the new fake news law.

2020 could well turn out to be a watershed year after the stellar performance of 2019 that makes one shudder when one thinks about it. And it is not just us, a rough survey of investors have indicated that many do not want to think about what lies ahead for markets, politics, the economy, the environment and society.

Here is to wishing all of us good luck into the new decade!