A Hard Look at the Maturing SReit Market

There is a new SReit coming to town but do not worry because I am not in the habit of writing sales pitches, and we have enough analysts reports out there to keep dozens of folks gainfully employed even if IPOs in Singapore have been non existent this year such that the recent Singapore O&G IPO has returned 164% in a quick rally for us to remember and then quickly forget.

The Manulife US Reit will be the largest IPO we have seen since the Accordia Golf Trust priced in Jul 2014, comprising non-Singapore real estate which is good because it is then exempt from the stamp duties involved in acquiring Singapore real estate and true to the intention as of the 2015 Budget.

Reits typically exist for mature real estate markets, the Heavens forbid if China decides to “reit” their real estate at their 55% market volatility levels and the continuous State interference that sometimes happen more than twice a day.

We know our reit market is maturing because there are new rules now to change gearing limits and increase the development limits so that managers can enhance their stable of properties to improve on yields. Additional disclosure on fees also prevent Reits from disadvantaging the minority stakeholders especially for those reits that used to be part of personal real estate portfolios.

SReits have not had a good year so far, quite flattish in their price action but still compares favourably against the STI Index which is down for the year and I think it is a remarkable feat indeed given that our interest rates have bucked global trends, going higher.

It is not an easy task to compare SReits with the rest of the world because there are just too many differences in cross borders accounting rules, mainly in asset depreciation and such.

Japan probably has the safest reit market because JReits are required to pay down their principal and interest annually which is an ultra conservative measure that protects the investor/shareholder against asset devaluation in times of crisis.

SReits, in contrast, do not have the debt pay down requirement and are only required to service interest payments which will leave them exposed even if their Loan to Valuation ratio is now limited at 45% much like the Australian Reit market which suffered heavy losses (>40%) during the Lehman crisis due to the collapse of their NAV and most of them were running on negative equity during that period, surviving on rights issues ransoms on stakeholders.

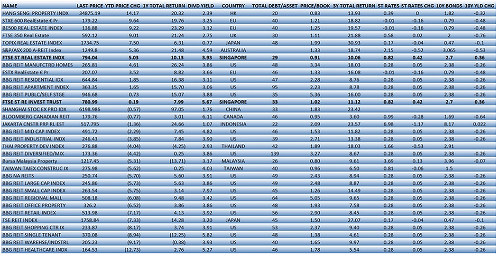

So how do SReits fare against the global US$ 12 trillion reit market, year to date?

Surprisingly well on price returns, with dividends ranked amongst the highest in the world, beating high yield countries like Australia. Note that I threw in some real estate indices for good measure.

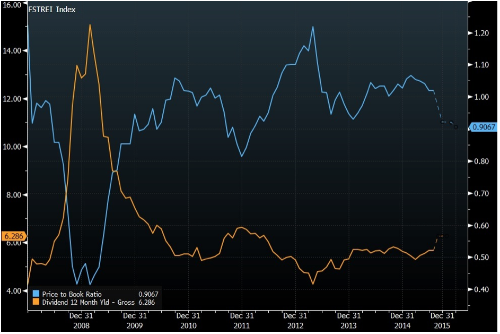

The SReits Index with its market capitalisation of SGD 65 bio has been delivering the typical 5-6% return since the height of the financial crisis with its Price/Book ratio hovering around 1.02, unchanged on the year.

The 2 main factors I would consider before investing in SReits.

- The risk free return of the Singapore 10Y bond versus dividend yields and expected dividend yields.

- The price to book value of the reit and price buffers to allow for asset devaluation due to economic outlook and returns (i.e. dividend yield).

SReits score well with 33% gearing (debt/assets) and low price to book ratio of 1.02. We can probably assume that they would be able to weather a substantial asset price collapse of about 26%. (33/74 = approx 45% gearing limit that MAS has imposed)

Thus the main consideration would be the dividends against the trend in the risk free rate.

Some thoughts:

- SReits are hybrid securities, caught between equities and bonds, in terms of how investors view them.

- While some of the Sreits are rated by the agencies, the ratings apply to their debt and not their equity which has a subordination effect.

- The economic slowdown in Asia has just begun, led by China and business outlook is, at best, stagnant.

- SReits returns have not kept up with the up-move in the 10Y risk free rate so far.

- From their lows last year, junk bonds are paying some 1-1.5% more this year even as SReit returns have not changed.

Advantages of Reits Over Bonds

- Yes, we can assume that some reits are safer than many bonds out there issued by highly leveraged companies out there. leveraged to their hilts.

- Unlike Business Trusts and corporates, SReits have an obligation to pay out dividends (90% of taxable income) and keep their loans under 45% of their asset valuations.

- And finally, Reits is a universal investor asset class, traded in an exchange for all lot sizes, prices and not restricted to just “accredited investors” who are hostage to an OTC market.

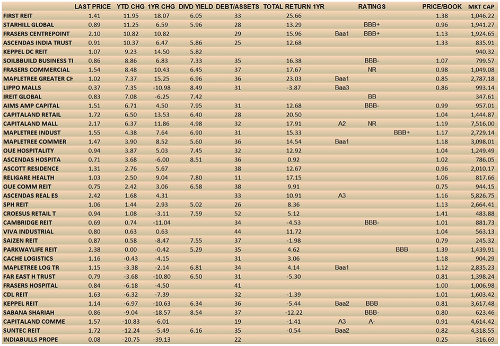

The best performing SReits and some business trusts this year.

We note that the heavyweights are nowhere near the top while it is understandable for small names like Sabana which reported difficulty in renewing some master leases and poor results. We can also understand the risk of buying Saizen Reit given the JPY currency weakness.

With such a mixed bag of results and performances, Morgan Stanley writes that the SReit market could be in for a spot of consolidation as Australia has seen in the past 2 years. This is as Temasek and JTC just completed the merger of Ascendas and Singbridge https://business.asiaone.com/news/ascendas-singbridge-merger-completed.

It would be hard to disagree with that assessment and tempting to take a punt or two based on Price/Book ratios although you could be hit with a rights issue if interest rates make re-financing difficult, noting that valuations have not caught up with 10Y yields.

Safer perhaps, is if someone would consider an SReit ETF or a Short SReit ETF just like the numerous ones we have out there?