Reviewing Our Market Perspectives: We Are Human, After All

Enter September 2018, without one of the last Americans who would stand up to Donald Trump’s dystopic take on the future of world order, on the 10th anniversary of the collapse of Lehman Brothers which led to the Great Financial Crisis of 2008.

Lehman, for some of us, happened 10 years ago, on the 16th of September (15 Sept in NY), over wanton mee at Fullerton hotel by the river. Who could forget it 10 years later, for the difference it made to our lives but we will save that story for another time.

Would we have come to this dystopic future if not for the GFC?

It’s perspectives, really, if you ask us, 10 years on at record highs in S&P 500, Nasdaq, S&P MidCap 400 and Russell 2000 as we head into September, numbers growing bigger and bigger from billions to trillions and folks can aspire to be worth over 100 billion.

You see, “that cocky voice in your head is wrong.”

What do we know after 10 years?

We did not know that the Indonesia Rupiah can hit a 20 year low, the Argentine Peso can break record lows as the Turkish Lira continue to crap out in the same week Donald Trump-led American markets breaks new highs.

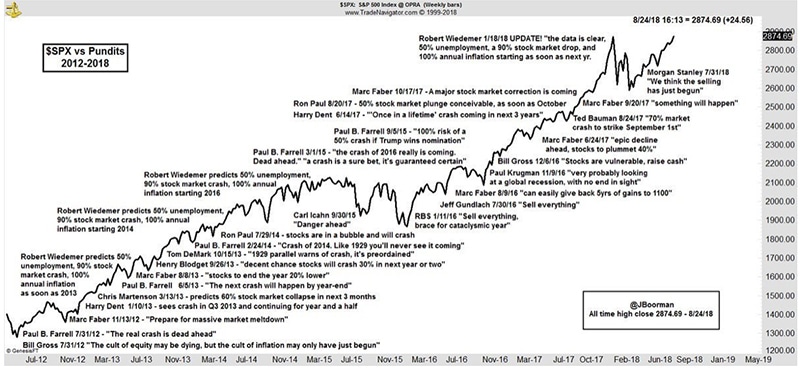

Check out the chart of shame of the S&P Index versus the renowned market pundits and naysayers over the past 6 years.

Source: Marketwatch

Source: Marketwatch

Verdict: We Are Guilty

We have been just as guilty, grasping at the “S&P 500 median Price to Free Cash Flow ratio is now 34.66”-straws that suggests that market over-valuation, or the “stock buybacks exceed capital spending in 2018”-straw to justify our pessimism while ignoring the good news like the S&P 500 profit margins rose to 11.6% in 2Q18, their highest level in history.

That is confirmation bias for us, seeking out evidence to support what we believe, just like the time when the endowment effect took hold of us to perpetuate the confirmation bias in our costly gold investment, years back.

As Ray Dalio tweeted this week—“Most people make bad decisions because they are so certain that they’re right. Radically open-minded people know that coming up with the right questions and asking other smart people what they think is as important as having all the answers.”

Source: Ray Dalio, from his coming book

Source: Ray Dalio, from his coming book

Perhaps we need fresh perspectives or we have been reading things differently from the other people out there. Perhaps all of us are mistaken and the market is one giant sum of what WSJ’s Jason Zweig summarised as common investor mistakes?

- Overconfidence (see Ray Dalio above)

- Confirmation Bias (see above)

- Myopic decision making

- Historic evidence versus gut feel

- Unconscious biases

- Unrealistic optimism

- Disposition effect – to sell winning positions too soon and hold on to loss-making trades

- Sunk-cost fallacy that leads many people to hold on to losses for years

- Home bias – to invest in their homeground

- Status-quo bias – passive investing?

- Bad at estimating probabilities

- Bias blind spot – to find fault in others and not ourselves

- Draw sweeping conclusions from small samples of data

- Overreaction

For details please read Dear Investor, That Cocky Voice in Your Head Is Wrong, WSJ.

Changing Our Perspectives

The entire Singapore appears to be caught in the 99-year leasehold debate, for all the government’s efforts to keep property prices affordable with the new borrowing limits and taxes but it does not seem to be dampening spirits from the following midweek headline.

Source: ST

Source: ST

It’s freehold!

A rick friend was telling us of rich people he knows from neighbouring countries who do not mind the extra taxes to buy real estate in Singapore for the peace of mind and comfort in currency and political stability.

And those folks from China and Hong Kong think 99 years is at least 29 years longer than the longest lease they have available in China (70 years) and freehold only exist to the state.

To make it affordable, they have made it smaller too, just as we thought that 441 sq ft for the tiniest apartment in that $3k per sq ft place was too small to live in… until we found the smallest apartment out there is 258 sq ft, somewhere off Balestier Road.

We have to change our perspectives here, as Singapore projects a 6.9 million population, and temper our biases towards real estate valuations because they are paying US$500k for 61.4 sq ft nano apartments (smaller than jail cells), about the size of a Singapore car park lot, in Hong Kong, of course.

The new perspective is that wealth is instantly created when the developer sells one of these, often dubbed, “coffin apartments”, to a buyer who possibly takes on a mortgage to pay it off. Who would live in them? Not us, of course, unbiasedly.

It is the same for stock markets – “America’s chronic current account deficit reflects a shift out of income-based saving into saving supported by asset inflation—leaving the US heavily dependent on frothy financial markets.” – The Current Account Counts, Stephen Roach

As long as wealth creation persists in asset prices, wealth begets more wealth because saving = buying assets (stocks, bonds, real estate), at times borrowing to do so, these days. The perspective has changed and new biases have been nurtured by the GFC, and is supported anecdotally by all the asset inflation happening, creating wealth in the process that we read about in the news, giving us “unrealistic optimism” (see list above), perhaps?

For the analysts, there is the bigger fallacy, an occupational hazard perhaps, that stock markets are a reflection of the economy when they are not, especially when it has been pointed out by M/I Investments that US$3.7 trillion in QE, US$ 15 trillion in global QE, zero and negative rates, US$70 trillion of new global debt and the 300% rise in stocks only got us a rough 2% gain in GDP growth.

Recognising Our Flaws

We are all but human and we could be wrong. For us, our mistakes in 2018, so far, has been to ignore the status-quo bias for complacency still lurks, global debt keeps ballooning, unchecked, but markets are none too worried.

Thus, while the eerie calm in markets has caused us considerable unease as we await for a capitulation of sorts, that is now looking increasingly like it will be something we cannot predict or expect.

We had thought that higher interest rate burdens would bite into spending and risk appetite but it has not happened as the prospects of capital gains is what the perspective has changed into – where savings = buying assets.

Now, we use the word “mistake”, in slight patronising fashion, as the year has been pretty decent, so far, and much better than it has been for most other folks mainly because we have forced to confront ourselves earlier this year when a star RM at a private bank told us not “to be too smart or think too hard”, which we wrote about in The Great Humbling: Markets Are Always Right, before we proceeded to catch the biggest correction of 2018 in the ensuing days.

Thinking without bias is and trumping behavioural economics is probably a feat that the great Warren Buffet or Ray Dalio are capable of doing, but being “radically open-minded” (in Dalio’s words) and admitting to mistakes, is perhaps a very good quality.

When Warren Buffet upped his Apple Inc stake again this month, saying that the “iPhone is enormously underpriced”, when folks are taking out loans to buy the phone (and not the AAPL:US stock), we decided that there is not much choice left for phone addicts because Google is always tracking you and selling that data without even talking about Chinese made phones that we would never be too phone-addicted to buy.

Donald Trump may be doing us a favour in his Google man-hunt.

It is September 2018, and status quo still prevails.

Biases aplenty, as we did a cheeky little poll without drawing sweeping conclusions (see listed above), of what would it be like if the government decided to subpoena all non-99 year leasehold land to be 99-year leasehold? Answers invariably veered towards home-bias, their positions, which looks like 85% of the population in HDB flats would be happy with such an outcome, minus those who own private non-99 year leasehold property.

We are human, after all.