Wrapping Our Heads Around Negative Yields

What a week and Bloomberg was not exaggerating last weekend when we were told to Get Ready for the World Economy’s Biggest Week of 2019 (sans Trump who had to steal the show on Thursday on Twitter and new tariffs).

Source: Bloomberg

Source: Bloomberg

A friend saw a blue tent covering a corpse fished from the Singapore river and saw the GBP break under 1.22 against the US dollar and wondered if it could be a forex suicide just like the time when gold plunged back in 2013 and there was a suicide at the Sail given that the local suicide rate is up 10% in 2018.

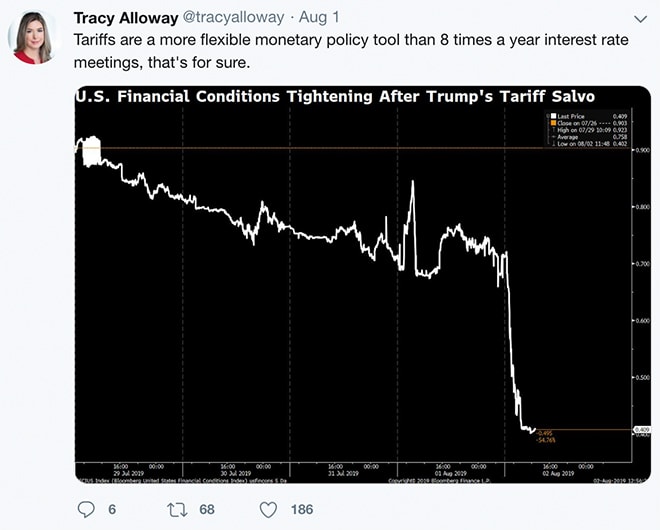

We can correlate anything these days, spicy foods have been linked to dementia and research shows fruit juice could lead to cancer and we really do not know what to believe in these days because on Wednesday the Federal Reserve did not cut interest rates enough, causing the first market decline on the day of a rate cut since Oct 1987. Yet Donald Trump managed to initiate a “rate cut” of 0.2% in a single tweet less than 24 hours later causing one of the biggest U-turns in market sentiments this year. The panic that ensued resulted in further yield curve inversion and odds of a rate cut in September jumped to 100% as gamma hedges propelled a ton of involuntary hedges against volatility (instead of prices) and we wonder if dementia is a bad thing for the mental damage all this is causing folks out there.

Source: Twitter Feed of Tracy Alloway

Source: Twitter Feed of Tracy Alloway

There are harder things to do we can suppose. We could try to win US$ 3 mio playing Fortnite, qualifying out of 40 million people or we could groom the 6 year-olds at home to YouTube stardom and buy a £6.4 million skyscraper in Seoul with less than 3 months worth of income after harnassing 30 million fans/followers. Both options too difficult even if billionaires Eduardo Saverin, Jack Ma and James Dyson make millions look cheap the way they are spending on Singapore’s ultra-prime real estate.

Yet is the billionaire rush for real estate a sign? A sign that a decade of low interest rates is changing everything? Is it “paradigm shift of epic proportion for investors”, as put by the CIO of fixed income at Guggenheim Partners?

Source: Bloomberg

Source: Bloomberg

We have stood by the idea that anything negative yield should not be worth anything, and we suspect we are echoing the views of the silent majority because paying someone to borrow money is a moral hazard, although it is something Indian Coffee tycoon could have done before his apparent suicide this week.

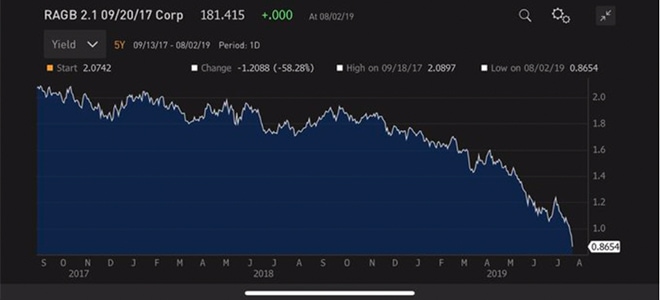

And we stand wrong on our stance on the negative yields because German 10 year yields hit a new low of -0.466% and German 30 year bond yields fell below 0% for the first time ever, meaning that German debt profits the government and pays for itself which is a feat until we consider the profits of buying Austria’s 100 year bond 2 years ago, roughly risk-free 82%! And we scratch our heads as to how we can survive on a portfolio yielding just 0.87% per year till 2117? And we slap ourselves because we said the same thing 2 years ago when the bond was issued at 100 with just 2.1% coupon vs 181.415 now.

Source: Bloomberg

Source: Bloomberg

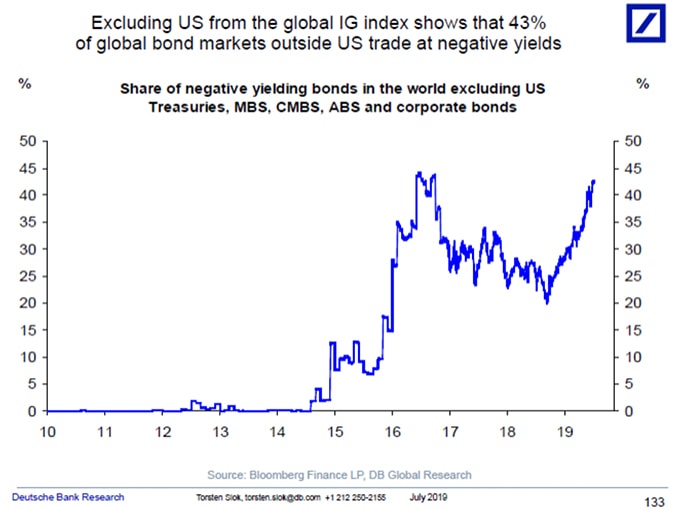

With 43% of global bonds ex-US trading at negative yields, it is high time to figure out how it all works because as it turns out, Japanese negative bonds are the cheapest in the world and Singapore is not far behind even though 1 month SIBOR is higher than every yield 10 years and below.

Source: Deutsche

Source: Deutsche

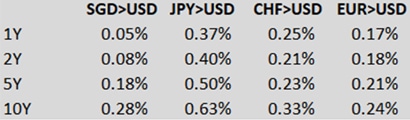

The secret is really more to do with the swaps and the demand for US dollars. We compiled the rough cost of USD against the 3 most negative currencies and added the SG dollar in for comparison. The roughly estimated results are tabulated below showing the percentage yield gains when buying those bonds/assets hedged for US dollars.

We can roughly assume that the numbers represent the equivalent yield lost if one were to buy US dollar bonds/assets hedged in the respective currencies.

This means that Japanese investors have the most to lose if they buy US dollar assets and that makes Japanese bonds look good for investors with US dollars to spare and it is true because a dollar funding squeeze is spreading across global markets.

Source: Bloomberg

Source: Bloomberg

While it may matter less to retail investors who have less access to the swap product, it is still important to realise that interest rate parity still drives the markets even if Japanese 10-year bonds are -0.2% because it is much higher in US dollar terms.

The reason why it got so good or bad for the Japanese was to do with the news this week that the Japanese Government Pension Investment Fund (GPIF), the largest pension fund in the world, revealed that it was hedging its bond purchases against currency fluctuations which meant paying all those numbers in the table above every time it bought something in USD or even EUR (take USD minus EUR). It does look a tad expensive then.

Source: Bloomberg

Source: Bloomberg

For the retail investor, the best way to visualise the concept is to observe the difference between the local Singapore SIBOR and SOR. Why is 1M and 3M SIBOR at 1.88% when the 1M and 3M SOR at 1.73%? It simply means if one buys a SG dollar asset financed in US dollar LIBOR, the rate would be 1.73% as opposed to financing in SIBOR before all the spreads they throw in. Capeesh?

Yet, how negative are the yields we are talking about? The picture below summarises the government bond yields and is not very pretty. It just feels wrong to be buying something at minus and will take a while to wrap the head around the fact that it is higher if it was in US dollars.

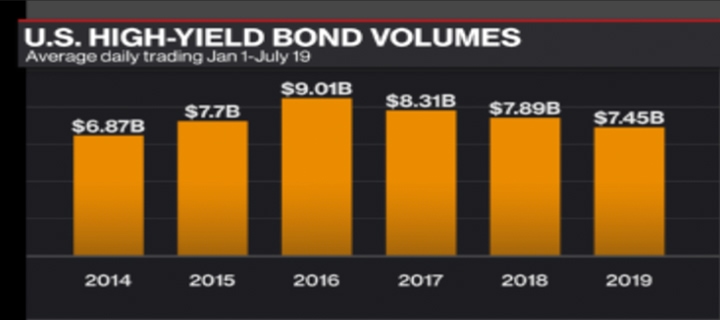

Looking at the table above, Singapore stands out when it comes to as cheap and as good as it can get. But does it make it more attractive than High Yield bonds which, according to Finra, have the lowest average daily trading volumes since 2014?

Source: Bloomberg

Source: Bloomberg

There is no intelligent answer to that question. But we do feel foolish for dissing the Austrian 100-year paper when it was launched in 2017 and we eat our words now reminded that is why we will never be Jack Ma or Eduardo Savarin or James Dyson in this lifetime.

We will conclude that we are starting to embrace the idea of negative interest rates and that we now know that Japanese yen bonds are relatively cheap and we urge people not to get too upset about the negative rate situation and seek help although the Samaritan hotline may not work. Good luck, folks.