A Short Story About Bonds and Strips

It is good to be back and writing—there’s a lot of crazy things going on in the world right now as we hold our breaths, wondering when the curtains will be drawn, so we can find ourselves in one galactic joke of a simulation.

But it is that time of year again. Our eyebrows rose as we witnessed an earnest young man asking the fishmonger at the market quite confidentially, after placing his CNY order, if there were more “impressive” offerings. To which the fishmonger gave an assuring reply that there would be more than enough exotic (and expensive) seafood to satisfy his palate (wallet).

Our “spidey senses” were activated. Could he be a private banker or RM of sorts? That sure fits the bill—unassuming, wholesome, and talks confidently about finance that we have been trying to save some friends’ parents from lately. Anyway, this is our comeback story.

A good part of 2024’s weekends have been spent going through the account statements of a good friend’s 86-year-old mother who had lost about half her savings to some mind-blowing investments recommended by her banker.

Who in their right mind would advise a then 82-year-old lady to take a punt on Alibaba (at 300 bucks) and Xiaomi at the same time for more than half her portfolio? Not only was the deed done, but the chap subsequently got a promotion for his zeal (or profits?) and remains her banker still. However, he has delegated his duties now to a junior who had the audacity, quite recently, to send her a redeeming trade to buy a “super safe” government bond, which will pay her 3.5 per cent in coupon semi-annually. Here’s the kicker: we flipped the page, we noticed the yield was closer to 2.5 per cent, after a hefty markup.

Asking around, we found some outraged folks who were willing to speak their minds under anonymity partly because they were underperforming compared to their peer bankers due to their sense of integrity. Or perhaps their superior product risk knowledge—there could be bankers who are genuinely unaware that the coupon is not the yield of the bond.

Comparing the situation to bond trader friends who have to scrimp for the 2 cents (0.02) on a bond trade, we were informed that the standard markup in priority banking (one notch below private banking) was three dollars (3.00) on the bond price (the standard notional price for bonds is 100.00) and that is a whopping 3 per cent or more if the bond price in under 100. Some places also claim to exercise compassion in cutting that standard margin if the markup reduces the ultimate bond yield by more than 50 per cent or something along those lines.

We were left speechless but nobody will be going to hell for the traumatised old auntie who was lately informed she had a month to close another private bank account for insufficient funds and needed another set of documents to go through with more legitimate investments (it was a foreign bank). She also had assumed those dividends she was getting quarterly, consisting of those funds she had her money in had the principal draw down clause (in that your principal would make up for the lack of returns) to pay for those dividends. Another loss conceived.

Now reduced to a priority bank client, we are happy to announce that auntie would have less to worry about now that we linked her with a reliable chap who would be an honest but fledging banker (for he has to work ten times harder than his peers to meet his targets).

Yet our interest was piqued in our various discussions that could be a damning expose, too incredulous to believe but entirely plausible for its ingenuity. This got us thinking that, true or untrue, if it exists or not, (because we are not PB clients and do not have an RM) would be the perfectly crafted margin-loaded trade.

Imagine a sales pitch where you were told that all you needed to invest now is 60 dollars to give you 100 dollars in, say 20 years.

It does sound good for some folks.

And to top it off, the investment would be in one of the safest financial instruments in the world—US government bonds. Welcome to the Strip Trade!

A strip, as its name implies, is a bond that has been stripped off its coupons to become a zero-coupon bond. A bond light in coupon would be light in price (to compensate for the lack of return) so it is not a product for someone looking for returns/payment along the way much like how a single premium insurance policy works. The price of a zero-coupon bond goes up in time as the missing coupons get imputed into the price on its way to maturity. Yet, a zero-coupon bond is not immune from capital losses if interest rates rise, unlike floating-rate bonds.

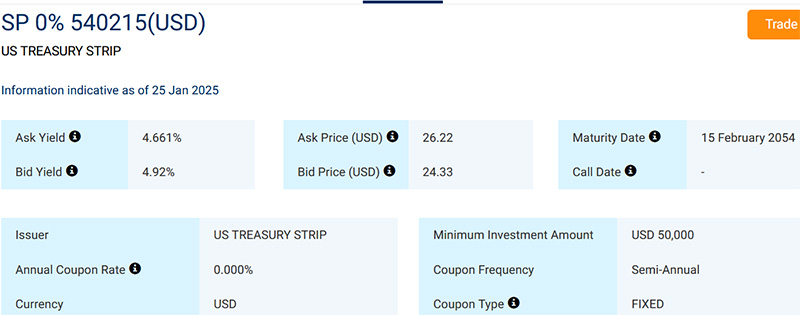

Screen clipping of a 2054 US Treasury Strip taken from the POEMS website showing offered cash price of 26.22.

Screen clipping of a 2054 US Treasury Strip taken from the POEMS website showing offered cash price of 26.22.

There you have the gist of it, and you can ask your favourite A.I. chatbot for more details although Investopedia is pretty good.

Back to the Strip Trade and if you are already sold on the idea of getting a dollar back for 60 cents you invest today, it would not be a concern if you paid 65 cents instead of 60 cents.

Indeed, folks like dear auntie would not notice the difference it would make to the chaps who sell it to you because he is looking at a 9 per cent margin (9 per cent profit for him vs 3 pe for regular bond trades as we mentioned above). Hence, a superstar banker is born!

Now we know 2024 was a volatile year for bonds, including US treasuries and rates rose a fair bit—some clients may find themselves sitting on a 20 per cent (which includes the 9 per cent margin above). But it can all be conveniently blamed on the market fluctuation; regular people do not carry a bond calculator around, much less than have access to market prices.

Enter the lifeline by the banker, in the form of a bond recovery note/fund where the strip is transferred to a structured note and pooled with others to create a diversified basket to limit your losses to, say 50 per cent, at a much cheaper and compassionate margin (profit) of say, 2 per cent. Plus, they may get a promotion next year for their zealous efforts.

Unfortunately, we hear that commission models are being phased out without much detail and we are not sure if this playbook would work in the future, but we are mighty impressed to present this to folks who might be keen to have a go at it. Imagine all the delectable seafood they can be ordering for the upcoming lunar new year.

Disclaimer: The above story is not intended to be a trade recommendation and does not purport to be investment advice or misadvice. We will not take any responsibility for how the information is used nor bear any earthly or heavenly repercussions for the abuse or misuse of the information.