One Man’s CoCo is Another Man’s Junk

As we come to the end of the Chinese year of the Horse, markets are ending on optimism which is rightly placed with the European Central Bank readying to embark on their €60 bio bond purchases per month till Sept 2016.

2015 has been a year of many “first’s” with another central bank (Sweden) cutting rates to negative last week as Switzerland making a new world record for the lowest borrowing cost for 10 year money – 0.011%.

Investors have been driven back to the high yield debt markets as Nestle bonds trade at negative yields and Apple hurries to tap the Swiss franc bond market.

Indeed the past week has been the the best week for junk bonds, year to date, as issuance rose to $9 bio in the US and high yield bond funds saw inflows of $2.9 bio, according to Lipper, the highest since Sep 2014. This is led mostly by oil prices stabilising and Moody’s reporting that default rates are holding steady.

In Asia, markets are calmed as 1MDB, an affiliated company of the government, paying off a loan and Chinese company, Kaisa, sort of out of the woods at the moment.

The reassuring headlines have soothed investor unease and bond recommendations are returning to our mail boxes, along with structured credit options to enhance those yields. I believe I even saw some recommendations to buying Singapore O&G names sometime last week.

That brings me to my topic for today – Not About High Yield Credits. For I am not a financial advisor but a responsible citizen writing to a public audience and I will not take to task writing about fads that could fade away as quickly as they started or as oil prices fall again, if we remember the 2014 chase for yields that got us to where we are today.

In addition, the trader in me thinks, that it does not make good sense to buy junk bonds when the default rate is at a low? Counter intuitive perhaps, but the bargains come usually when there are defaults?

Instead, I would like to highlight a possible alternative that investors could consider, along with reasons why.

The CoCos market, which has not taken off in the Singapore dollar market, trading mostly in the hard currencies of USD, EUR, GBP and CNY.

Confusion remains over old Basel 3 compliant AT1 bonds and new CoCos, the different types of CoCos and recourse of action during defaults, the governing bodies and such which I admit was the main reason I hesitated to write about them, for I am not qualified to give an expert opinion.

The other reason I had shunned CoCos is also that their prospectuses are usually 3 times as thick as a normal one, heavily loaded with legal jargon that makes a non masochist shiver at the thought of even skimming through.

CoCos stand for contingent convertible bonds which are structured to absorb losses on a going concern basis by converting to equity or by being written down. This happens when a bank’s capital ratio falls below a contractually specified trigger level or when the authorities determine that the bank is not viable (source: Deutsche Bank)

Some facts:

CoCos can be Tier 1 or Tier 2 although the incentive is to go for Tier 1 CoCos

CoCos have different features but the main one to note would be the trigger, whether it is higher e.g. 7% (higher risk) or lower (lower chance of a trigger).

CoCos have different types of conversions – to equity, full or partial write downs which are temporary or permanent.

CoCos have different regulators depending on the jurisdiction of issue.

Risks:

- CoCos are unproven although we have seen in recent years, senior bondholders penalised/bailed-in with loss sharing too!

- There is still a debate raging as to whether CoCos should be considered equity although it has come to be accepted as a hybrid security which makes it hard for any self preserving bank to market as an alternative to bonds (for obvious legal reasons).

- Transparency issues as capital ratio numbers are published periodically.

- CoCos are seen as a boon for shareholders who can share their losses and yet not their profits with the holders.

- CoCos are hard to evaluate and compare across the board as each have different features.

My Take

CoCos are here to stay and to stay they will and the market will continue to grow as Basel 3 kicks in come Mar 2019.

We should be expecting the SGD dollar bond market to start launching those CoCos this year as their time runs short for Basel 3 which MAS is currently implementing. The eligibility of existing preference shares to count towards capital is reduced by 10% each year starting from 2013 which means that in this year, the capital recognition is cut to 70%.

CoCos vs high yields?

With the ECB coming in next month, it does look like banks will be the first destination for ECB cash. The Too-Large-To-Fail banks will be under heavy scrutiny which is an additional level of protection for investors, if you ask me.

Added Scrutiny = lower profits i.e. lower dividends.

Institutional investors are currently limited in their risk appetite for CoCos because the product does not fall into the fixed income category and banks are unable to buy because of the capital limitations imposed by Basel 3.

This means that liquidity can be poor.

Yet this also implies that perhaps the prices are reasonable?

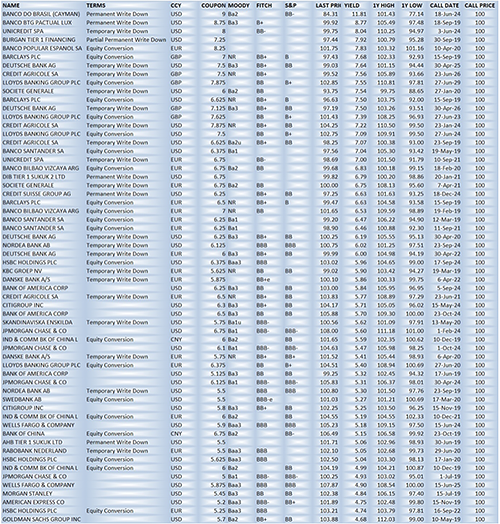

I compiled a list of major hard currency CoCos trading in the marketplace and ranked them by yield. I prefer hard currency this year as it saves the additional worry of forex swings.

Given that US high yield ETF, HYG US, is delivering a yield of about 5%, I suppose CoCos, at 5 to 7.5%, on average, should be comparable? Especially when the CoCos are issued by a bank that is in the Too Large To Fail category?

High yield bonds, senior or not, are as vulnerable, aren’t they?

Like I have always said, one man’s senior is another man’s junk.

Disclaimer: Note that CoCos are hybrid securities that bear significant risk and that countries like the UK have banned their distribution to the mass retail market, classifying them as “highly complex” instruments.