No Arguing with the Liquidity Crisis

What happens when you get into a private hire vehicle only to be lambasted by a crotchety driver telling you not to tell him how to drive, spoiling for an argument? No, we are not arguing with you, you know best, time is money to you and you know the roads better. Yes, we totally agree that BMW drivers are assholes and everyone is out to get you on the roads. Just shrug it off like us when the old man who eyed us menacingly at the hawker queue earlier today to butt right in front of us for his carrot cake, only to, errr karmic-cally, drop his change into the food because his poor hands were unsteady.

Like, how do we argue with that? Just like the picture below which more or less sums up the new world order if Trump has his way, creating a new royal family?

Why do we argue about nasty China with anti-commie friends when we have really no idea between facts or fabrications? Just surrender and say, you win, because our opinions are not about to make a difference anyway? It is the same for Vietnam which cannot argue much as the U.S. Slaps Import Duties of More Than 400% on Vietnam Steel.

We cannot argue with the week we had in markets—S&P 500: All-Time High Dow Jones Industrial: All-Time High Nasdaq 100: All-Time High US Bonds: All-Time High US Jobs: 105 straight months of gains, longest run in history US Economy: longest expansion ever at month-end and we have the Fed: Cutting Rates on July 31st .

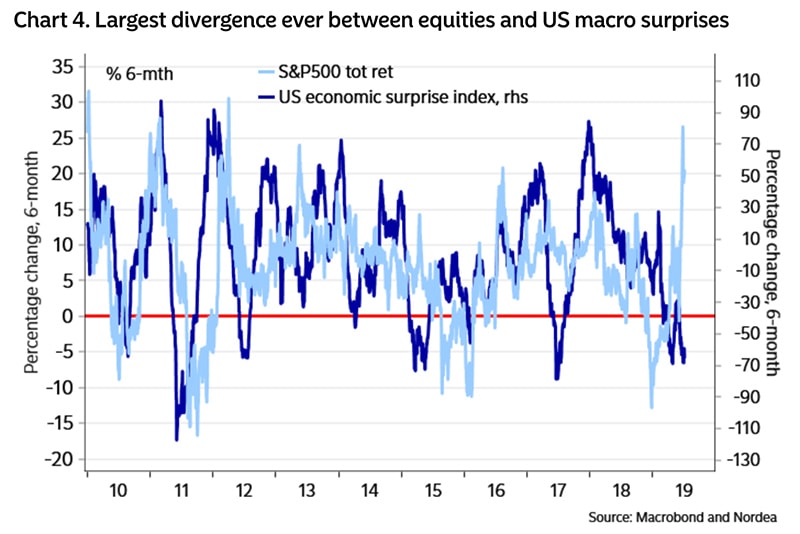

Nordea Bank notes, “comparing US equity market performance over the past six months with US macro surprises reveals the largest divergence ever”. Economic numbers and stock markets have simply decided to disagree even we cannot argue with that.

Source: Nordea Bank

Source: Nordea Bank

Yes, this is the longest period of expansion in the U.S. economy on record, at 120, tying the record for longest ever with 1991-01. On July 31st, it will be the longest in history. Meanwhile, negative yielding bonds now make up 40% of outstanding government debt, for a new record of US$13.4 trillion which includes US$608 billion of corporate bonds.

As all things negative is fashionable, we would also have the second highest number of S&P 500 companies issuing negative earnings (i.e. expected losses and not negative earnings growth) guidance for 2Q19 since 2006, just 87 out of 113 companies.

How can we argue with that when stocks are at record highs?

It is all perfectly timed to the election of Christian Lagarde, a lawyer and politician, to the head of the European Central Bank this week which has been viewed as “less independent” by markets and a good reason for investors to cheer given her well known view that “negative interest rates benefit the global economy”.

Source: WSJ

Source: WSJ

As Pimco says, “we see many of the supposed safe havens as offering a period of return-free risk rather than risk-free returns”, and “Heaven and Hell” are now perfectly priced in markets.

“We had a rally in both risk-free and risk assets,” said Geraldine Sundstrom, portfolio manager at Pacific Investment Management Co. “Both are priced to perfection. We have a fixed-income market priced in between heaven and hell.”

Thus it is perfectly acceptable for Friday’s headline that U.S. Stocks drop after STRONGER than expected jobs report.

Yet, we cannot argue that newly listed China Tobacco (6055 HK) is still up nearly 500% since its IPO last month even though WHO estimates around 3,000 people die every day in China due to tobacco use, as about 46,000 are born.

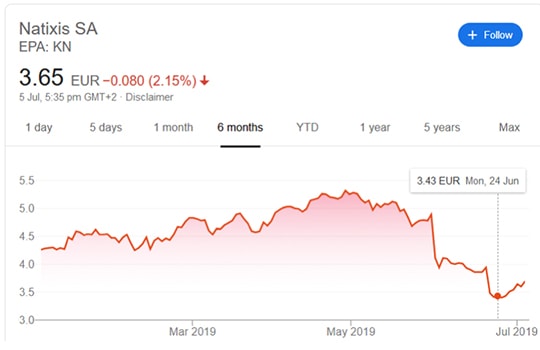

It is happening for a reason and we cannot argue with markets but what we are able to argue is that in the past weeks, 2 mutual funds, one backed by Natixis, have seen massive outflows or investor runs which led Woodford Investment Management run by equity star, Neil Woodford, to freeze client withdrawals due to “liquidity concerns” when the sales pitch was that investors would have daily access to their money. And client wealth is being eroded as the mutual fund remains shuttered as liquidation continues to progress and could take more than a year according to a Morningstar estimate.

Shortly after Woodford came H2O Asset Management which saw outflows after a FT report on some questionable debt dealings and Morningstar’s subsequent downgrade over “liquidity and appropriateness” of the fund’s holdings although the fund did not get around to freezing withdrawals, we are not sure how much investors got back after “losses were written off” and Natixis saw its shares take a fair beating for it.

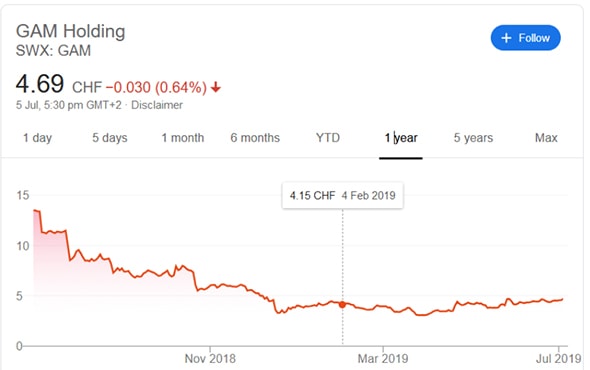

This follows the supposed “isolated” GAM scandal late last year when the Swiss-listed investment company froze client withdrawals after heavy outflows from its absolute-return unconstrained bond funds and dismissed star bond fund manager, Tim Haywood, in Feb 2019. Till now, fund liquidation is underway and there is little update as to how much investors have lost although GAM shares have taken a huge beating since October last year.

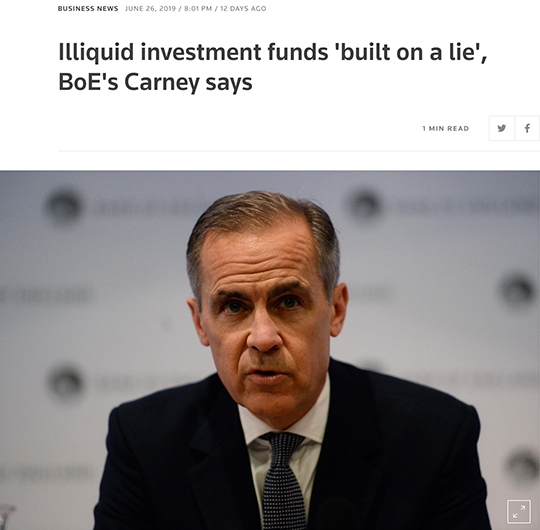

So far, the loudest regulator has been BoE Governor Carney who said “investment funds that include illiquid assets but allow investors to take out their money whenever they like were “built on a lie” and could pose a big risk to the financial sector”.

Source: Reuters

Source: Reuters

We definitely agree with Mr Carney, no argument about that. There is no arguing with the Federal Reserve’s warning in their May financial stability report stating, “the mismatch between these mutual funds’ promise of daily redemptions and the longer time required to sell bonds or loans may be heightened if liquidity in these markets diminishes in times of stress”, as if they knew of Woodford and H2O was coming along.

Liquidity is something we take for granted but experience since the financial crisis tells us that it can be a mirage, as none other than another Pimco alumnus, Mohd El Erian, opined as well.

Source: Bloomberg

Source: Bloomberg

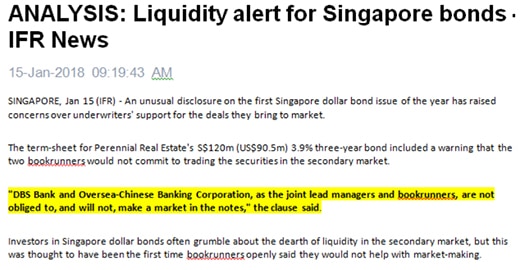

We can use Singapore as an example and wonder, in reality, how many million worth of, say, a perpetual bond you can sell at a single time in the market and you would be unpleasantly surprised—as we had pointed out in the past that local banks have taken to include in their offering circulars.

Taken from an email alert from IFR, 2018

Taken from an email alert from IFR, 2018

It is a global phenomenon now that is evidenced in the chart below which shows bank dealing positions of corporate securities shrinking in recent years against the total market capitalisation of bonds which are sitting in various investor pockets.

Source: Twitter feed of Sunchartist

Source: Twitter feed of Sunchartist

Does anyone ever wonder about how easy it would be to sell after they buy? For instance, the newly launched Credit Suisse leverage bond fund or the DBS Global Income-something, does anyone ever wonder what the liquidation price would be especially if there was a run, Heavens forbid.

It is the same for ETFs, with 80% of the market on autopilot and Index-Crazed Investors Turning S&P 500 Into One Gigantic Company.

Source: Bloomberg

Source: Bloomberg

It is as Jeff Gundlach describes, “herding behaviour”, with passive investments now in the driver’s seat which makes flash crashes (because there is no one on the receiving end) more commonplace in recent times.

Yet it is worse for China, as “herding” passive investing takes off even as the “number of listed companies with little or no analyst coverage has grown” and we also know it is hard to say bad stuff in China without getting into trouble too.

Source: Bloomberg

Source: Bloomberg

We will not argue with all that because inefficiencies can be profitable for savvy investors for instance in the illiquid bonds in the Singapore dollar market that trade at steep cash discounts to their European equivalents.

It is hard to argue against much these days—not against Trump because it looks like he will never go away, not against the central banks because there is nothing we can do and definitely not against NASA, which is headed to a giant golden-what? No arguments left.

Source: Fox News

Source: Fox News

Disclaimer: This is not a Trump-inspired attempt at gaslighting regarding the liquidity conditions of the market. We are just as bone-weary as anyone who has sat through markets in the past week, gaslit, moonstruck and mentally fried.