The First SGD Corporate Bond ETF Is Worth Musing Over

How can we expect others to spend more time and money on Facebook when our personal usage has declined sharply in the past year, with barely time to check on all our Whatsapp messages on a daily basis, reduced to replying some messages days later.

As we said last year, the next big trade could be in eye care because people will start going blind from over-usage of their phones to read Chinese literature besides being “expected to call for cabs and Ubers, do their shopping, book their holidays, order meals and groceries, buy insurance, do their banking and watch TV, play games and music too”.

This week’s big tech earnings have just proven, as Zerohedge summed on Twitter, “people are ditching social networks and watching less streaming movies so they have more time to purchase useless trinkets on Amazon”.

There is nothing much to gripe about that we have not written 2 months ago, when we were a little early in observing that the market is a “bit too long in the tooth for the FAANG club” because we have Facebook, Twitter, Netflix and Intel missing their earnings forecast, while Amazon missed on revenues.

Locally, we cannot be griping about the cybersecurity breaches since we have been unaffected by the 2 major data breaches onshore—Singhealth and SIAS, and we are pretty slow on the uptake on all things tech, no thanks to Pay-whatever or those banking apps and quite happy with our TV-and-Alexa-free lives.

What is worth musing over; the highlight of the week for us, would be the very first SGD corporate bond ETF.

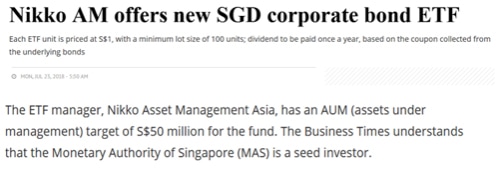

What We Think? Nikko AM offers new SGD corporate bond ETF

It has been a long wait for this and we suspect it is largely because the iBoxx SGD Non-Sovereigns Large Cap Investment Grade Index, took much longer to construct to show for the mouthful that it spells.

What on earth is the iBoxx SGD Non-Sovereign Large Cap Investment Grade Index?

We are not sure. But we will continue to be Not Sure because we can only guess at the constituents and it will definitely not be public information because Markit, the owner of the index is a for-profit organisation.

Why would Nikko AM only anticipate a target for S$ 50 million for the fund?

Source: BT

Source: BT

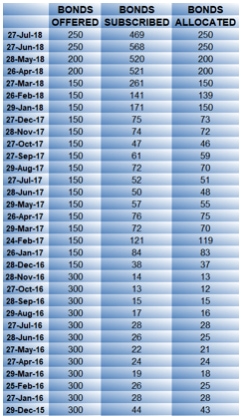

We are not sure, again. And we are definitely not sure because the Singapore Savings Bonds have been oversubscribed every single month, except for February, in 2018. We have had a healthy 4 monthly average of over S$ 500 mio in the past months.

Singapore Savings Bonds Monthly Stats (in SGD mio’s); Source: MAS

Singapore Savings Bonds Monthly Stats (in SGD mio’s); Source: MAS

If the statistics say anything, there is no stopping at S$1 billion dollars for this IPO.

Is This the Best Time to launch a SGD Corporate Bond ETF?

We are not sure too.

For one, Singapore government bond yields are starting on a divergence path with global rates.

Comparing the performance of the 10Y SGS yield against the 10Y US Treasury Note, we notice Singapore yields appear to be outperforming of late. Yet, we would not hold out for that extra 0.25% more we could be getting unless global rates continue on their upward trend which puts fixed rate instruments at risk.

Chart of US 10Y yields vs SGD 10Y yields; Source: Bloomberg

Chart of US 10Y yields vs SGD 10Y yields; Source: Bloomberg

Demand for corporate bonds has been on the wane as funding costs have increased and many a retail investor have been affected by the series of defaults we have seen since late 2015, with the latest coming out of CW Advanced Technologies and the fates of Hyflux retail bondholders still in limbo.

As such, issuance has faltered in 2018, running 23% behind this time in 2017 and maturities have not been matched by new offerings as we have summarised roughly in the table below.

Estimated SGD corporate bond maturities 2018 vs new issues

Estimated SGD corporate bond maturities 2018 vs new issues

Maturities exceed new issuance by over S$ 4 billion, probably due to the lack of demand, higher funding rates and capital losses.

A global trend perhaps, as central banks turn off the QE spigot and we cannot find a single bond index in the world that is in the money year to date, except for the US junk bond index.

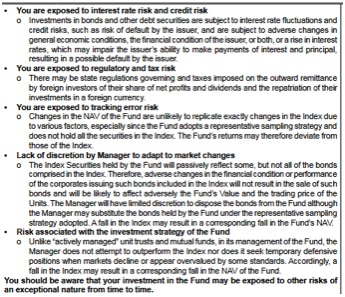

Yet, as the product highlight sheet stated, the fund is only suitable for investors who seek medium to long-term capital appreciation, so we should take off those trading hats on that matter.

Why the NikkoAM SGD IGBond ETF is Such a Good Thing?

It’s cheap! Expense ratio 0.3%!

It’s safe-ish, diversified and currency hedged, granting exposure to 102 bonds from 45 issuers, mainly HDB, LTA, SIA, DBS and Temasek (all government-linked!) and only 4.7 years average duration, delivering 3.2% which is nearly 1% higher than the Singapore Bond Index Fund’s (SBIF SP) 2.32% , notwithstanding the SBIF’s lower expense ratio of 0.25%.

This sort of return beats some of the unit trusts out there minus the fees!

The STI Index group of blue chips only managed a 3.08% average dividend yield last year, is suffering 2.29% capital loss for 2018 even if 2018 is expected to deliver 3.94% dividend returns.

Seeing that HDB bonds give an average 2.32% in yield and SIA just 3.07% with Temasek and DBS somewhere in between, we can expect the returns to come from the “20% of its total net asset value in such non-Index Securities” which is what we will not be able to access on our own and we know that there will be little heroics involved here because “unlike “actively managed” unit trusts and mutual funds, the Manager does not attempt to outperform the Index nor does it seek temporary defensive positives when markets decline or appear overvalued by some standards.”

With such fees which gives them no incentives to outperform, we can only expect good old-fashioned index investing and pretty predictable and straightforward returns, minus the bunch of risks highlighted, mainly interest rate and credit risk as well as the tracking error risk (when we see exodus inflows or outflows).

Source: NikkoAM

Source: NikkoAM

It is perhaps no wonder, to us, that the ETF is not included in the CPFIS scheme at the moment or folks will be ditching those unit trusts en masse and causing market gridlock?

Yet it does look like fund managers out there will have to work doubly hard for their money now that the “alternative” has arrived, especially those heavy-loaded investment-linked products tied to life policies etc.

What Will Keep Us Up At Night?

“Where are they going to get all the bonds in the index from?” a friend asked, given the lack of market depth which would pose a problem too eventually when funds get redeemed.

The market liquidity would be a major problem if this ETF really takes off and attracts global attention or makes its way into the CFD markets. Major redemptions and unit creation amounts will have the ability to roil the delicate balance of the local Singapore bond markets.

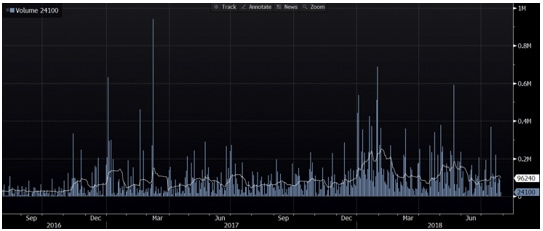

Yet, before we run ahead of ourselves, we should be reminded that the only other SGD ETF in Singapore, the SBIF Government bond ETF does not trade in a big way, with lackadaisical volumes over the past 13 years since its launch in 2005, e.g. last Friday’s volume of S$ 24.1k, for all of its S$ 750 mio in AUM.

Volume graph of the SBIF ETF over 2 years; Source: Bloomberg

Volume graph of the SBIF ETF over 2 years; Source: Bloomberg

That does not give a lot of hope for market liquidity, if we are to be honest to ourselves and we certainly would not want the market makers to give up, bid-offer spreads to widen to untouchable levels like the way individual government bonds quote on the exchange.

Good news too, for those in the know, because iBoxx is not known to be sharpest on market pricing which opens up the opportunity for potential arbitrage, that we will not delve into as it is a topic should not be discussed publicly.

Worth Musing About the NikkoAM SGD IGBond ETF?

Definitely.

Perhaps it took so long since SIA did their mega-sized issues last year and rumours of the ETF emerged, because the fund manager had to define its “representative sampling” strategy – investing in a representative sample of securities in the Index which have a similar investment profile as that of the Index.

How many Aaa HDB’s and Temasek’s are there out there in a world where there are only a handful of Aaa-rated names that give SGD 3.2%?

We are not sure, yet again.

There is no perfect timing but it is a good time as any to save investors from making other stupid investment mistakes, give the fund management industry a kick in the butt and run for their money and, revive the fledgling Singapore markets.

An ETF could spawn a CFD market that will give investors a chance to short or hedge themselves?

An ETF that puts 3% returns in the hands of the retail folk that will reshape the idea of blue chips, unit trusts and REITs?

We are not sure but we sure hope for success that made all this musing worthwhile.