Turning the Summer Heat Up on Junk Bonds

21st June is this year’s summer solstice, marking the turn of the seasons, as the heat is turned up for the Northern hemisphere. Markets around the world remained gripped in the Greek saga which still does not have a resolution in sight with time fast running out for the country to pay its loan to the IMF coming due by 30 June although Moody’s did say a default on the IMF does not constitute a formal default, it would only be a matter of time.

Source: Financial Times

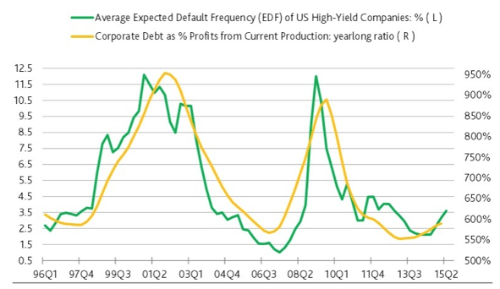

Moody’s, however, did caution that high yield bonds are in a dangerous zone at the moment with default risk highest since Dec 2012 as the ratio corporate debt to core profits climbs to levels not seen since late 2011 despite the easy monetary policies around the world.

Source: Moody’s

High yield bonds have become the staple for the private banking client, all hankering for the yields. They do lend an air of sophistication to conversations with friends and boasting that you dabble in junk. Not everybody invests in junk it is those who can afford to that win those admiring glances because junk, as its tag suggests, is high yield for a reason – that is it high risk!

When people ask me if I trade junk bonds, I find myself hard pressed for an answer, simply because I do not know if they are on the same page as me on the definition of junk. What constitutes junk these days ? The price? The yield? Or the rating? Or all of the above?What is the yield cut off for a bond to be speculative ? For my old and stubborn brain that still cling to days when Indonesia’s 5Y default swaps were >10%, I still find it hard to relate to my friends who are defining junk as the 6% cut off in yield. On hindsight, how could we ever have imagined that Indonesia would default ? Even though Greece is on the brink of it which we never imagined back then as well !After various discussions and mental re-calibrations, I decided to adopt the 6% threshold for USD yields to be junk, applying the same to SGD for the purpose of this post.

Why junk?

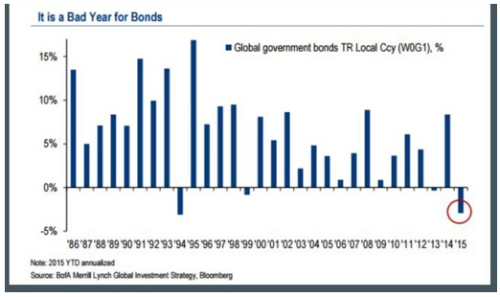

Because, SURPRISE, junk bonds have turned out to be the stars of the bond market this year as sovereign and investment grade bonds have floundered, giving negative returns so far.

Source: Otterwood Capital Management

What has actually performed worse than sovereigns has been the covered bonds with the Bloomberg Covered Bonds Index showing a -6.38% return year to date.

Bond Indices YTD Returns

Why is safety under appreciated even as US junk bond defaults rose to thehighest level since Oct 2009 giving us a total of 9 defaults in May? Because it has been isolated to commodity companies so far. And there are really not a lot of bonds to choose from if you are looking for that 6%. Of the 300 over thousand active bonds in the world, I could only find over a thousand hard currency bonds that are not in default or a defaulting government and liquid enough that pays a 6% or more yield. Narrowing them down, we have the same old names as far as Asian investors are concerned – the Chinese real estate names, O&G names, Indonesia and Indian corporates etc.

I prepared a table of SGD bonds that fall into the “junk” category. Just 47 names for the universe with prices just indicative, or potentially suspect, because of their illiquidity.

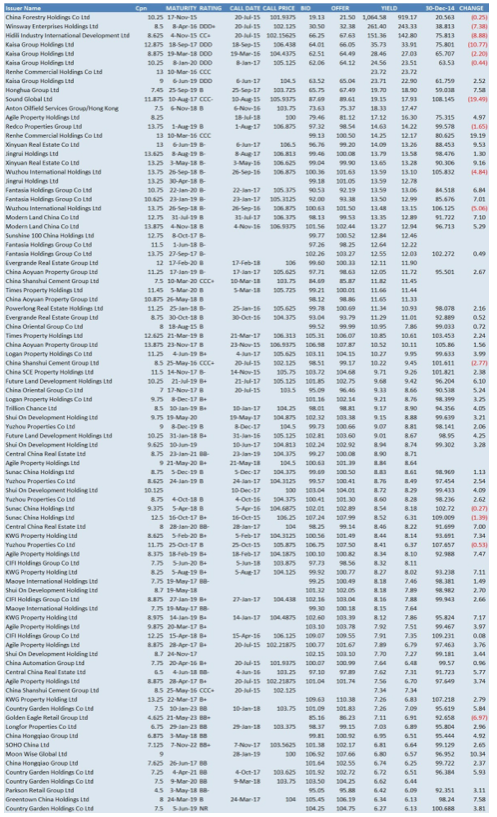

It is worthwhile noting that some of the bonds were not issued as junk (i.e. coupon <6%) but turned “junk” anyway and some junk got even “junkier” this year as prices fell further. I have a few favourites in the list and some friends, who had enjoyed the ride in Trikomsel, already know what we should be looking at next. Yet, so much for the small world of SGD bonds, the greater interest of the private investors lie in the big pool of Chinese issuers which have done better this year. I managed to extract a list for our review.

Other than the scandal riddled names, with new ones popping up every other week, we have rallies in most of the bonds for the year, until the next scandal strikes like the on we are witnessing unfold for China Shanshui Cement as I write.

The lesson in junk bonds is that we really do not need defaults to lose a bomb. I quote from my old Fabozzi bond bible “even though the actual default of an issuing corporation may be highly unlikely, the impact of a change in perceived credit risk or the spread demanded by the market for any given level of risk can have an immediate impact on the value of the security.”

Singaporean investors may recall the momentary madness we saw in markets back in 2012 when even investment grade perpetuals were dumped in panic which allowed the market to pick up bonds at big discounts. To quote Santayana, “Those who do not remember the past are condemned to repeat it”.

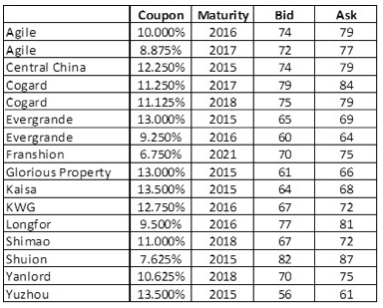

Here is a Chinese real estate bond run from 7 Oct 2011.

Whether the Greek problem is sorted or not, we still have China correcting 10% of their 120% (year to date) gains last week and we will have more commodity related defaults coming (it usually takes >12 months for companies to run into trouble). For those who do not remember the times when bond prices drop 10% overnight, I would share with them that during those moments, a 2% yield would never be more appealing.