Should I Chase The Rally: Greenspan Was Wrong Then Right On Animal Spirits

People are calling and chatrooms are buzzing with friends saying they were cashing out of their DBS stocks at SGD 18, after the steepest rally since 2009, which I would not attribute to boasting, on account of the nature of our friendship, although I cannot say the same for the rest who had to post their regret when DBS hit SGD 18.40 before closing the week at SGD 17.83. Others are celebrating renewing their rents at 10% discounts and it is certainly looking like a festive period for most investors so far, who are clearly ignoring the capital losses in their bond portfolios because it is only right to treat those bonds, as their category implies, as fixed income, to be held to maturity.

Graph: Steepest and Sharpest rally in DBS stock since 2009

It is also just too bad for celebrations if their favourite char kway teow seller passes off because char kway teow is unhealthy business, not just for the consumers, but the cooks as well, having to deal with the endless hours of grease, smoke and soot that will undoubtedly take a carcinogenic toll on their lives and who would want to sell char kway teow in the future when insurance companies start deeming it a hazardous profession?

Carrot cake at Commonwealth Crescent

As I devour my plate of fried carrot cake, I wonder about the rare stock rally we are witnessing and if I should chase it because I have been insufficiently invested, according to the standards of Greed, as many of us would be and I have about a dozen new emails in the past week on how the Dow would sustain towards 20,000 for a mother of all rallies that is here to stay! And to persist for a long time more. Who would not expect it especially when we had the Dow set 5 consecutive new historical highs every single day of this memorable December week, breaking 5 milestones in a month.

Source: wikipedia

Did I just really miss out on the biggest bull run of my life? Or did I miss something in the past 4 weeks since the US just elected a president with the lowest favourability rating in modern history? Who had managed to unleash “animal spirits”, on the 20th anniversary of Alan Greenspan’s “Irrational Exuberance” speech on 5th Dec, 1996. For the record, the Dow continued to make new highs 3 years following Greenspan’s comments.

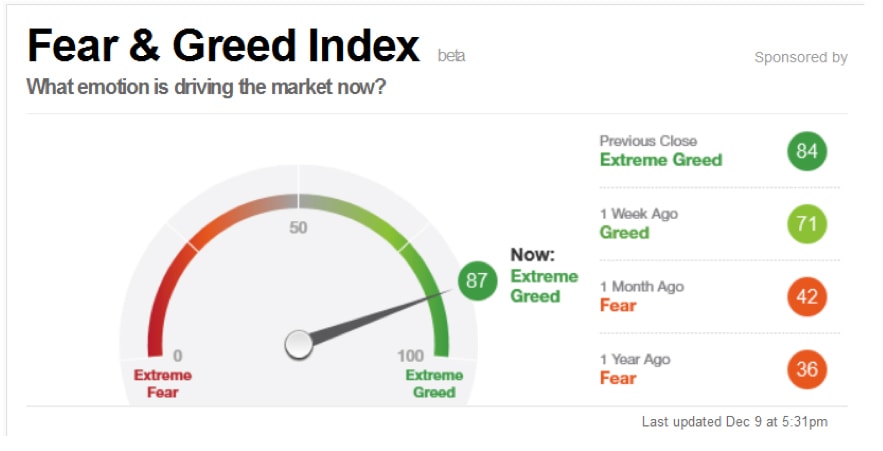

Well, analysts are probably doubling up as fantasy and sci-fiction writers right now—dreaming of their Trump future and writing to justify their jobs because having no clue is not in the job scope. Therefore, we are just 1 month into the new Trump fairytale reality and the CNN Fear and Greed Index is still not close to 100 yet.

Source: CNN Money

Perhaps its about the tax repatriation holiday that Donald Trump has promised? Analysts are expecting more stock buy-backs than jobs created or investments which is all speculative, of course, but good enough reason to buy shares. Alternatively, no reports have mentioned the possibility of buying bonds back at a big discount at the rate the markets are selling off.

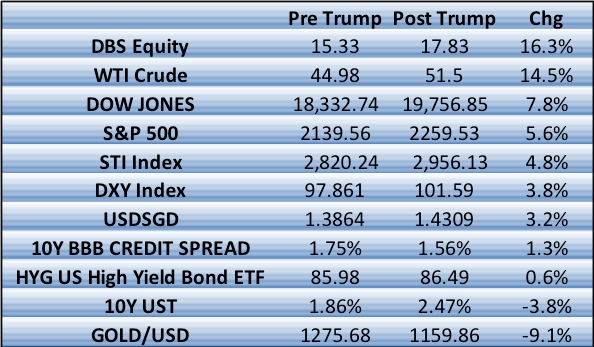

Nonetheless let’s do a quick tally of the month and the price action ranked.

Darn, it looks like we should have thrown it all into DBS and quickly sold it at $18 like my friends did right before the news of their HK branch scandal broke! Because the gains would have beat buying the USD and the Dow combined and it is not even as if they have announced a stock buyback programme.

Is It Trump Or Is It Oil Or Is It Just Sentiments?

Economic growth uncertainty has risen since the US elections with the sustained strength of the US dollar that will threaten the emerging markets reliant on USD funding. Global trade is threatened by the election promise to keep jobs in the US and more recently, to impose a 35% tax on companies that move their productions overseas and try to sell their products to Americans.

It got even better last Thursday with an apparent tough stance on China.

Notwithstanding the good news is that economic data from the developed markets have not looked stronger this whole year with PMI numbers and economic surprise indices all mostly beating expectations and inflation gauges turn to healthy as oil prices look set to heard higher especially with this weekend’s renewed production cut pledges, something that has not happened since 2001.

We may even want to thank Saudi Arabia over Trump for this month’s windfall because it is official now—higher oil prices are actually good for the economy as it spurs inflation and prices will rise, including asset prices such as stocks although we are not sure about Gold and real estate?

It is far easier to speculate in the pot of gold at the end of the Dow Transport Index which is up nearly 10% for the month, head and shoulders over the rest, for the promises that Trump has made, as Ken Rogoff suggests in Trump Boom? That the confidence will be boosted in an economy that is already growing at 3%, if the new administration gets it right although it can still end very badly, which is something we should not worry about at the moment.

What If We Cannot See The Reasons to Cheer?

Here in Singapore, most of the stressed out Singaporeans that we wrote about last week, could be struggling to find a reason to cheer or even be upbeat with the 5% return the STI has made in the past month as the SGD currency weakened 3.2% against the USD. Except for those who put all their money into DBS, OCBC, UOB, Genting, Sembcorp, Keppel Corp and gang, which have outperformed the STI.

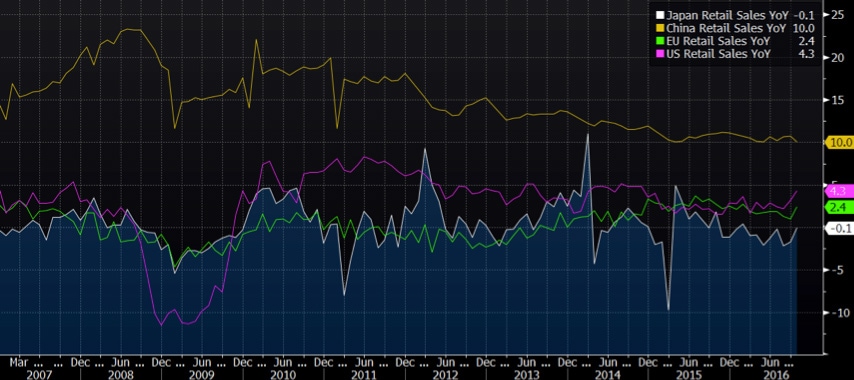

The Japanese have, on the other hand, been rejoicing with their currency weakness (-8.8% on the month)that is only bested by the Mexican Peso which has lost 10% against the greenback, giving the Nikkei stock index a massive 9.3% boost. That has managed to pull Japanese retail sales up to -0.1% YoY, less negative than before, while China slows to a 10Y low of 10% even as the US and EU give promising single digit growth.

Table of Retail Sales YoY Growth – US, China, EU and Japan

Table of Retail Sales YoY Growth – US, China, EU and Japan

We Are Not Alone

- Goldman prime: two-thirds of hedge funds have missed the past month’s move

- Regular investors don’t love this rally yet—here’s what that means for stocks

- “Since 1920, however, the eighth years of presidential terms have represented the worst of election years. While the Dow Jones Industrial Average has posted an average gain of 4.8% in election years since then, the last year of a two-term presidency has been down an average of almost 14% on the Dow and about 11% for the S&P 500 according to the Almanac, with losses in five of the last six times a two-term president was finishing up.”

- Valentin Dimitrov at Rutgers and Prem Jain at Georgetown University have concluded in their studies that only when the CAPE (cyclically-adjusted PE) is above 27.6 have stock markets proven to be really bad investments over 10 years. The last known CAPE is 27.9.

We Are Bond Traders

Trump’s promises, of course—Hope. The US economy is looking robust, with financial conditions at peak and the world looking towards Trump to close his doors on them or to sing to his tune for the most uncertain future we have faced since the crisis, that we can only embrace with Hope as our central bankers finally take the backstage.

The only problem is that only bond traders cannot feel the optimism.

As of 1 December, “November’s rout wiped a record $1.7 trillion from the global index’s value in a month that saw world equity markets’ capitalisation climb $635 billion”. This is referring to the global bond index. The global bond market (US$133 trillion) is about twice the size of the global stock market (US$67 trillion).

Greenspan is right to worry about the bond market in his recent 3rd December interview although he repeated his view that “bubbles are almost impossible to stop once they get going”.

And only the bond maestros are worried for “Bill Gross and Jeff Gundlach are among investors musing that the so-called Trump rally may have gone as far as rationality might allow.” Because we cannot ignore the cost of the interest expense as well as bond portfolio losses that will impact the pension funds, insurances companies, central banks, sovereign wealth funds, asset managers and banks.

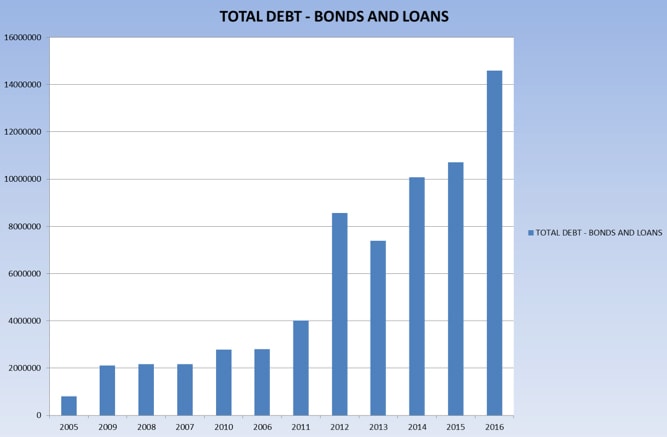

2016 saw a record US$14.6 trillion of debt (excluding govt but including municipals) priced, in the bonds and loans market, representing a 40% increase from 2015 and 2014 which saw about US$10 trillion priced which were record years as well.

Source: Bloomberg (10 year chart of bonds and loans issuance (excluding govt debt)

Market sensitivity to interest rates is higher than with the abrupt tanking of debt markets which has put trillions of dollars of loss into investors’ pockets even though Trump’s spending plans actually hinge on low financing rates to work and happy investors. And we have not even started on mortgage rates yet.

If we go by the fact that the post-election year has always delivered the weakest returns since 1900 which makes absolute sense because new presidents need time to set up shop and get things to work, 2017 has a risk of ending in a fizzle.

Bond traders are born pessimists. Nature or Nurture, un-excepted. But it is very hard to see earnings grow above interest expense, unless it is earnings per share. And DBS at $18 was a good sell, on hindsight and it does not make sense to chase this Trump or oil or sentiment rally even before Trump becomes president.

Just as Greenspan was wrong then right on animal spirits.